Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The Bank of England's committee decided to keep their main interest rate (Bank Rate) at 4%, which is what most people expected. However, the vote was close (5 members for keeping it, 4 members wanted to cut it by a small amount), showing that more people on the committee are leaning towards lowering rates.

The Bank of England's committee decided to keep their main interest rate (Bank Rate) at 4%, which is what most people expected. However, the vote was close (5 members for keeping it, 4 members wanted to cut it by a small amount), showing that more people on the committee are leaning towards lowering rates.

They believe that the worst of inflation is over and prices are starting to slow down. This slowdown is due to their current high rates, slower wage increases, and weaker price growth in services. They also noted that a slow economy and a less tight job market are helping to push inflation down.

The committee now thinks the risks of missing their 2% inflation target are more balanced; they are less worried about high inflation sticking around and more worried about the economy being too weak. Still, they emphasized they need to see more proof that this trend will continue.

Future rate cuts will happen gradually and will depend entirely on the new economic data that comes in.

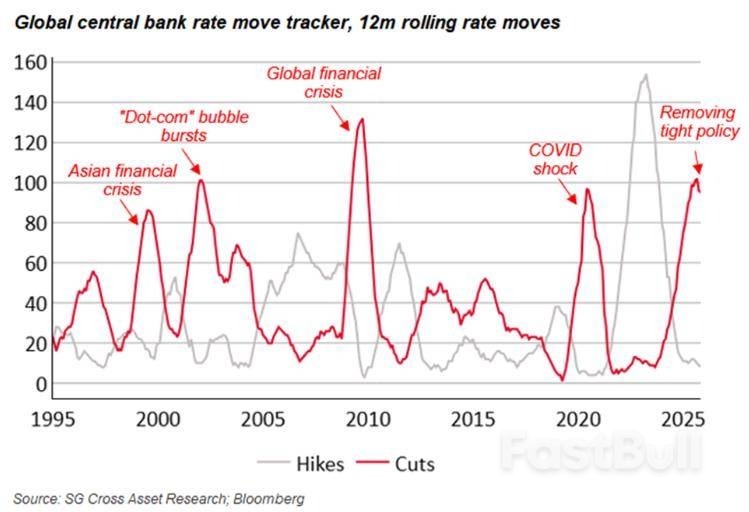

Optimism that the Bank of England (BoE) might cut interest rates this year is rising, causing UK 10-year bond yields to drop significantly since mid-October. Just a month ago, the market doubted the BoE would cut rates again soon. Now, the view is changing because inflation, currently at 3.8%, appears to have peaked.

Even though the full drop won't happen until next year, encouraging signs are appearing: food price inflation is easing more quickly than expected, and service sector inflation is slowing down. This is being helped by private sector wage growth also falling, which is on track to end the year below 4% after starting much higher.

This confidence is also boosted by expectations that the upcoming Autumn Budget will be viewed positively by the financial markets.

UK Chancellor Rachel Reeves welcomed today's BoE cut to inflation forecast.

According to the BoE "Progress on disinflation indicates bank rate likely to continue a gradual downward path: "gradual and careful approach" to further withdrawal of monetary policy restraint".

On the subject of inflation, Governor Bailey stated "It is encouraging that the inflation peak in September was 0.2 percentage points below our August forecast". All in all signs appear positive on the Inflation front.

There is another inflation print due out on November 19, which could have a major impact on pricing of a BoE rate cut in December, before attention turns to Chancellor Rachel Reeves' budget.

The UK budget will become the main area of focus as the month progresses. Fiscal sustainability remains key and will likely determine the impact the budget speech has on the GBP.

If Chancellor Reeves adopts more fiscal tightening the implications could lead to further weakness for the GBP. A budget which delivers tax hikes but pushes up 2026 inflation could potentially boost the GBP while a budget that under-delivers on fiscal sustainability could prompt a severe sell-off in the GBP.

Chancellor Reeves really has an unenviable task ahead of her with markets paying close attention.

Markets saw the GBP weaken in the aftermath of today's rate decision with a 30-40 pip selloff in GBP/USD.

However, cable has since reversed this and pushed higher to trade around the 1.3100 handle at the time of writing.

A break above the 1.3100 handle and four-hour candle close could embolden bulls and push GBPUSD toward the 1.3250 handle and the 100-day MA which rests around the 1.3270.

If cable fails to find acceptance above 1.3100 handle, a retest of the crucial 1.3000 level may be in the offing.

GBP/USD Four-Hour Chart, November 6, 2025

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up