Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Turkey Trade Balance

Turkey Trade BalanceA:--

F: --

P: --

Germany Construction PMI (SA) (Nov)

Germany Construction PMI (SA) (Nov)A:--

F: --

P: --

Euro Zone IHS Markit Construction PMI (Nov)

Euro Zone IHS Markit Construction PMI (Nov)A:--

F: --

P: --

Italy IHS Markit Construction PMI (Nov)

Italy IHS Markit Construction PMI (Nov)A:--

F: --

P: --

U.K. Markit/CIPS Construction PMI (Nov)

U.K. Markit/CIPS Construction PMI (Nov)A:--

F: --

P: --

France 10-Year OAT Auction Avg. Yield

France 10-Year OAT Auction Avg. YieldA:--

F: --

P: --

Euro Zone Retail Sales MoM (Oct)A:--

F: --

P: --

Euro Zone Retail Sales YoY (Oct)A:--

F: --

P: --

Brazil GDP YoY (Q3)

Brazil GDP YoY (Q3)A:--

F: --

P: --

U.S. Challenger Job Cuts (Nov)

U.S. Challenger Job Cuts (Nov)A:--

F: --

P: --

U.S. Challenger Job Cuts MoM (Nov)A:--

F: --

P: --

U.S. Challenger Job Cuts YoY (Nov)A:--

F: --

P: --

U.S. Initial Jobless Claims 4-Week Avg. (SA)A:--

F: --

P: --

U.S. Weekly Initial Jobless Claims (SA)A:--

F: --

P: --

U.S. Weekly Continued Jobless Claims (SA)A:--

F: --

P: --

Canada Ivey PMI (SA) (Nov)

Canada Ivey PMI (SA) (Nov)A:--

F: --

P: --

Canada Ivey PMI (Not SA) (Nov)A:--

F: --

P: --

U.S. Non-Defense Capital Durable Goods Orders Revised MoM (Excl. Aircraft) (SA) (Sept)A:--

F: --

U.S. Factory Orders MoM (Excl. Transport) (Sept)A:--

F: --

P: --

U.S. Factory Orders MoM (Sept)A:--

F: --

P: --

U.S. Factory Orders MoM (Excl. Defense) (Sept)A:--

F: --

P: --

U.S. EIA Weekly Natural Gas Stocks ChangeA:--

F: --

P: --

Saudi Arabia Crude Oil ProductionA:--

F: --

P: --

U.S. Weekly Treasuries Held by Foreign Central BanksA:--

F: --

P: --

Japan Foreign Exchange Reserves (Nov)

Japan Foreign Exchange Reserves (Nov)A:--

F: --

P: --

India Repo Rate

India Repo RateA:--

F: --

P: --

India Benchmark Interest RateA:--

F: --

P: --

India Reverse Repo RateA:--

F: --

P: --

India Cash Reserve RatioA:--

F: --

P: --

Japan Leading Indicators Prelim (Oct)A:--

F: --

P: --

U.K. Halifax House Price Index YoY (SA) (Nov)--

F: --

P: --

U.K. Halifax House Price Index MoM (SA) (Nov)--

F: --

P: --

France Current Account (Not SA) (Oct)--

F: --

P: --

France Trade Balance (SA) (Oct)--

F: --

P: --

France Industrial Output MoM (SA) (Oct)--

F: --

P: --

Italy Retail Sales MoM (SA) (Oct)--

F: --

P: --

Euro Zone Employment YoY (SA) (Q3)--

F: --

P: --

Euro Zone GDP Final YoY (Q3)--

F: --

P: --

Euro Zone GDP Final QoQ (Q3)--

F: --

P: --

Euro Zone Employment Final QoQ (SA) (Q3)--

F: --

P: --

Euro Zone Employment Final (SA) (Q3)--

F: --

Brazil PPI MoM (Oct)--

F: --

P: --

Mexico Consumer Confidence Index (Nov)

Mexico Consumer Confidence Index (Nov)--

F: --

P: --

Canada Unemployment Rate (SA) (Nov)--

F: --

P: --

Canada Labor Force Participation Rate (SA) (Nov)--

F: --

P: --

Canada Employment (SA) (Nov)--

F: --

P: --

Canada Part-Time Employment (SA) (Nov)--

F: --

P: --

Canada Full-time Employment (SA) (Nov)--

F: --

P: --

U.S. Dallas Fed PCE Price Index YoY (Sept)--

F: --

P: --

U.S. PCE Price Index YoY (SA) (Sept)--

F: --

P: --

U.S. PCE Price Index MoM (Sept)--

F: --

P: --

U.S. Personal Outlays MoM (SA) (Sept)--

F: --

P: --

U.S. Core PCE Price Index MoM (Sept)--

F: --

P: --

U.S. UMich 5-Year-Ahead Inflation Expectations Prelim YoY (Dec)--

F: --

P: --

U.S. Core PCE Price Index YoY (Sept)--

F: --

P: --

U.S. 5-10 Year-Ahead Inflation Expectations (Dec)--

F: --

P: --

U.S. UMich Current Economic Conditions Index Prelim (Dec)--

F: --

P: --

U.S. UMich Consumer Sentiment Index Prelim (Dec)--

F: --

P: --

U.S. UMich 1-Year-Ahead Inflation Expectations Prelim (Dec)--

F: --

P: --

U.S. UMich Consumer Expectations Index Prelim (Dec)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Most emerging Asian equities traded in positive territory on Thursday, following the release of cooler US inflation data for February, although an escalating global trade war continues to loom.

Most emerging Asian equities traded in positive territory on Thursday, following the release of cooler US inflation data for February, although an escalating global trade war continues to loom.

The MSCI's gauge for emerging Asian equities rose as much as 0.6%, rebounding from a 0.4% drop at close on Wednesday.

Data from the US showed that consumer prices increased less than expected in February, but investors fret that the improvement is likely temporary against the backdrop of aggressive tariffs on imports that are expected to raise the costs of most goods in the months ahead.

However, the upbeat sentiment from cooling US inflation supported a rebound in emerging Asia stocks and currencies, according to Poon Panichpibool, market strategist at Krung Thai Bank.

Stocks in Kuala Lumpur rose the most, advancing around 1.5% and snapping a five-session losing streak, while Thai equities climbed nearly 0.3%.

On the other side, as April approaches, concerns over reciprocal tariffs have surfaced, with US President Donald Trump continuing to impose tariffs on neighbouring countries. This could potentially have a negative impact on assets in emerging Asia, Poon warned.

"Countries such as India, Thailand, Philippines ... collect higher tariffs from the US when we compare to what the US collects from them ... we could definitely face reciprocal tariffs for sure, which could be quite negative for EM Asia," he said.

Stocks in Indonesia slipped, falling as much as 0.7% in early trade as a few large banks, including Bank Mandiri (Persero) and Bank Rakyat Indonesia (Persero), pulled the benchmark lower.

A nearly 30% drop in Indonesian government revenues in January, which comes as President Prabowo Subianto implements big spending plans, has raised concerns about fiscal sustainability and a potential jump in borrowing.

Meanwhile, equities in Taiwan fell the most, dropping around 1.4%, dragged by TSMC.

In currencies, the Indian rupee and the Philippine peso rose about 0.2% each.

On the other hand, the South Korean won and the Taiwan dollar slipped around 0.1% each.

A rise in global trade tensions and worries over US recession risks have rattled global markets and sparked huge volatility in the foreign exchange market, as traders see-saw between relief and angst over Trump's whipsawing policy changes.

A majority of Americans believe President Donald Trump is being too “erratic” in his moves to shake up the US economy, as his imposition of tariffs against some of the nation's top trading partners hammers stock markets, a new Reuters/Ipsos poll found.

Some 57% of respondents, including one in three Republicans, said the president’s policies have been unsteady as his efforts to tax imports have set off a global trade war, according to the two-day poll that closed on Wednesday.

Americans instead want Trump to continue to focus on combating high prices even as there are growing concerns his policies will drive costs up, not down, the poll found.

Trump’s imposition of tariffs on allies such as Canada and Mexico and his refusal to rule out a recession has spooked US markets. The S&P 500 has lost more than US$3 trillion (RM13.3 trillion) in value since its all-time peak last month.

In response, the White House has said that some short-term economic pain might be necessary for Trump to implement his trade agenda, which is intended to drive manufacturing back to the US.

Wall Street has been shaken by some of Trump's whipsaw policy reversals. On Tuesday, Trump announced more severe tariffs on Canadian metals — causing stocks to fall — and then dropped the threat later that day after Canada made a concession.

Overall, 44% of respondents said they approved of the job Trump was doing as president, unchanged from a Reuters/Ipsos poll conducted March 3-4. He got particularly weak marks on the issue of the cost of living, where just 32% of respondents approved of his performance.

And most of them — 70% including nine in 10 Democrats and six in 10 Republicans — said they expected higher tariffs will make groceries and other regular purchases more expensive.

For most of his political career, Trump — a real estate developer turned reality TV star — has pointed to the strength of the stock market as an indication of economic health. But since returning to office, he has downplayed it.

“Markets are going to go up and they’re going to go down. We have to rebuild our country,” Trump said at the White House on Monday.

That’s a sharp change in tune from his first term, when, in March 2017, Trump celebrated the Dow Jones industrial average blasting through the 21,000 mark for the first time.

"Since November 8th, Election Day, the Stock Market has posted $3.2 trillion in GAINS and consumer confidence is at a 15 year high. Jobs!" Trump at the time posted on the site now called X.

A White House spokeswoman on Wednesday urged patience, calling the market’s performance “a snapshot of a moment in time, and we expect there will be good days and there will be bad days, but ultimately, Wall Street and Main Street are going to benefit from this president's policies, as they did in his first term.”

Inflation was far and away the top concern of respondents to the poll. Six in ten respondents said that was the issue they thought Trump should prioritize, far more than those who cited other presidential priorities including reducing the size of government, addressing immigration and fighting crime.

Recession warnings

Some analysts have painted a gloomier picture. Investment bank JPMorgan sees the risk of a US recession this year at around 40%, and considers an economic downturn even more likely if Trump follows through with another planned wave of tariffs in April.

Already, the White House has steepened levies on Chinese-made goods and on Wednesday hiked taxes on a wide range of imported automotive and tractor parts, construction materials and machinery parts — much of which are purchased from Canada and Mexico. Canada and the European Union on Wednesday pledged to retaliate with their own trade barriers on US products.

Inflation, which surged under Trump's predecessor in office, Democrat Joe Biden, remains high and is expected to increase due to tariffs, analysts say.

Despite the volatility, Republicans on Capitol Hill and Trump’s supporters still support his economic vision.

Senator Roger Marshall told Reuters he believes the market was “overvalued.”

“The market is one piece of the puzzle,” Marshall, of Kansas, told Reuters. “There’s other things going on: How do we get interest rates down, bringing manufacturing jobs here. I think it’s all a pretty complicated picture.”

Others acknowledged that the declines were a worry for Americans, particularly retirees and those approaching retirement age sensitive to their retirement savings accounts.

"We all know that people who are relying on retirement accounts watch them daily. And so, I think maybe he needs to be a little more sensitive to that," said Republican Senator Shelley Moore Capito of West Virginia.

Democratic Senator Richard Blumenthal of Connecticut viewed the sell-off differently. “It may not make any difference to him, because he's a billionaire. But to the everyday investor, it's a really big deal to lose this amount of money,” he said.

Nearly 80% of Republicans in the two-day poll said they agreed with a statement that Trump's actions on the economy "will pay off in the long run," a sign that some people in Trump's party have faith in his policies even if they are nervous about the short-term effects.

Forty-one percent of respondents overall — and just 5% if Democrats — said Trump's policies would pay off eventually.

Americans for Responsible Growth, an advocacy group representing Democratic state treasurers, called Trump’s approach “chaotic” and said it was harming investors across the nation.

“What may have seemed like a quick fix in Trump’s mind has become a big mess that will not only take a long time to clean up, but has also left consumers and businesses with higher prices, fewer choices, and more uncertainty,” said Dave Wallack, the group’s executive director.

The poll surveyed 1,422 US adults nationwide and had a margin of error for all respondents of three percentage points.

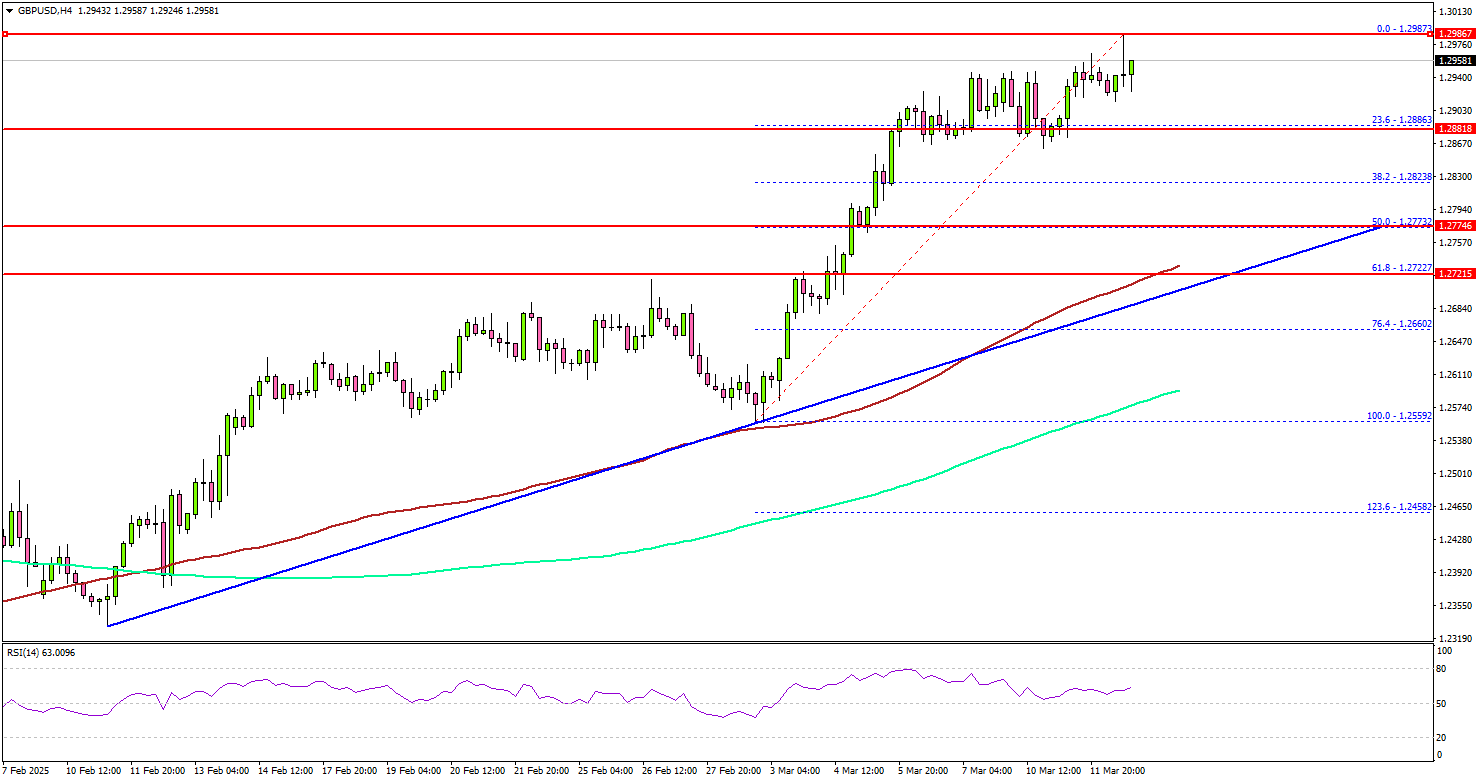

GBP/USD Technical Analysis

The British Pound formed a base and started a fresh increase above 1.2800 against the US Dollar. GBP/USD broke the 1.2850 resistance to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 1.2850 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even cleared the 1.2920 resistance zone.

It seems to be aiming for a move above the 1.3000 resistance zone, which is a major hurdle for the bulls. The next major resistance is near the 1.3050 level.

The main resistance is now forming near the 1.3120 zone. A close above the 1.3120 level could set the tone for another increase. In the stated case, the pair could even clear the 1.3200 resistance.

On the downside, immediate support sits near the 1.2880 level. The next key support sits near the 1.2850 level. Any more losses could send the pair toward the 1.2800 level. The main support could be 1.2740. There is also a key bullish trend line forming with support at 1.2720 on the same chart.

Looking at EUR/USD, the pair also started a decent increase and the pair could now aim for a move toward the 1.1000 resistance.

Upcoming Economic Events:

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up