Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

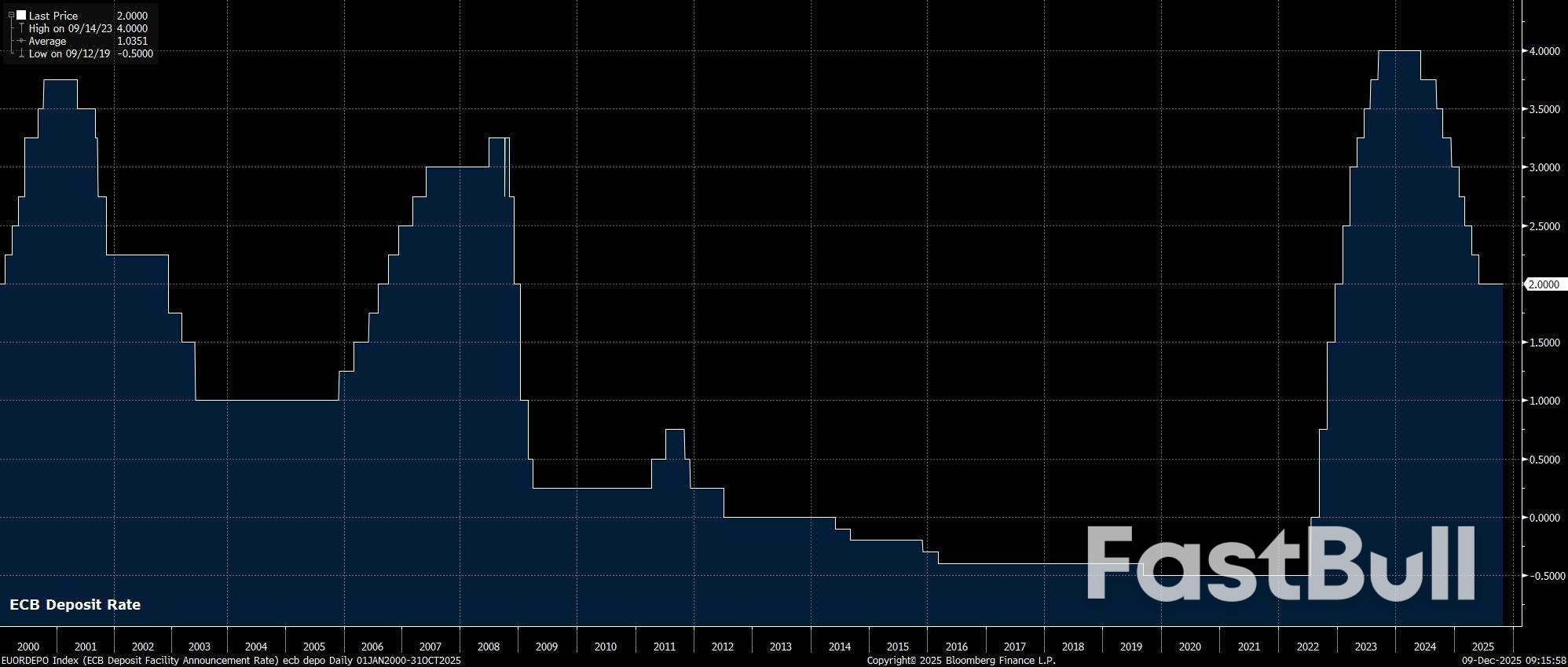

Rates On Hold: The ECB should maintain all policy settings at the December meeting, holding the deposit rate steady at 2.00%; Forecasts In Focus: December's staff macroeconomic projections will be they key area of focus, particularly whether an inflation undershoot is foreseen for 2028; Easing Cycle Over: The upcoming meet should do nothing to dispel the idea that the easing cycle is done & dusted, though policy tightening remains some considerable way off.

After what most market participants would describe as an incredibly dull October confab, the ECB's Governing Council aren't especially likely to deliver much more by way of excitement this time around, with policymakers still in a 'good place', and being set to round out the year by standing pat on all policy instruments.

As alluded to above, the ECB's Governing Council are set to stand pat at the conclusion of the December policy meeting, maintaining the deposit rate at 2.00%. Such a decision to stand pat comes not only as the EUR OIS curve discounts next-to-no chance of any further easing, but also amid little indication from any GC members that they presently see a desire to reduce rates further. All signs point to the easing cycle having now come to an end, and 2.00% being this cycle's terminal rate.

That said, the swaps curve has got rather excitable of late, now discounting around a 1-in-5 chance that the ECB will deliver a 25bp hike by the end of next year, spurred on by hawkish comments from Exec. Board member Schnabel in recent days. That pricing does appear rather over-ambitious at this juncture, given the likelihood of a relatively sustained inflation undershoot, hence participants will be watching for any explicit pushback on the idea that policy will be tightened within the next 12 months.

With the GC set to hold all policy settings steady, focus will naturally fall on whether policymakers decide to make any guidance tweaks.

The chances of said tweaks, however, range between 'incredibly slim' and 'none at all', with the accompanying policy statement set to simply reiterate the commentary that has been used for many months, and is now incredibly familiar to all participants. Consequently, the statement will repeat that policymakers will continue to adopt a 'data-dependent' and 'meeting-by-meeting' approach to upcoming decisions, while also making no 'pre-commitment' to a particular policy path.

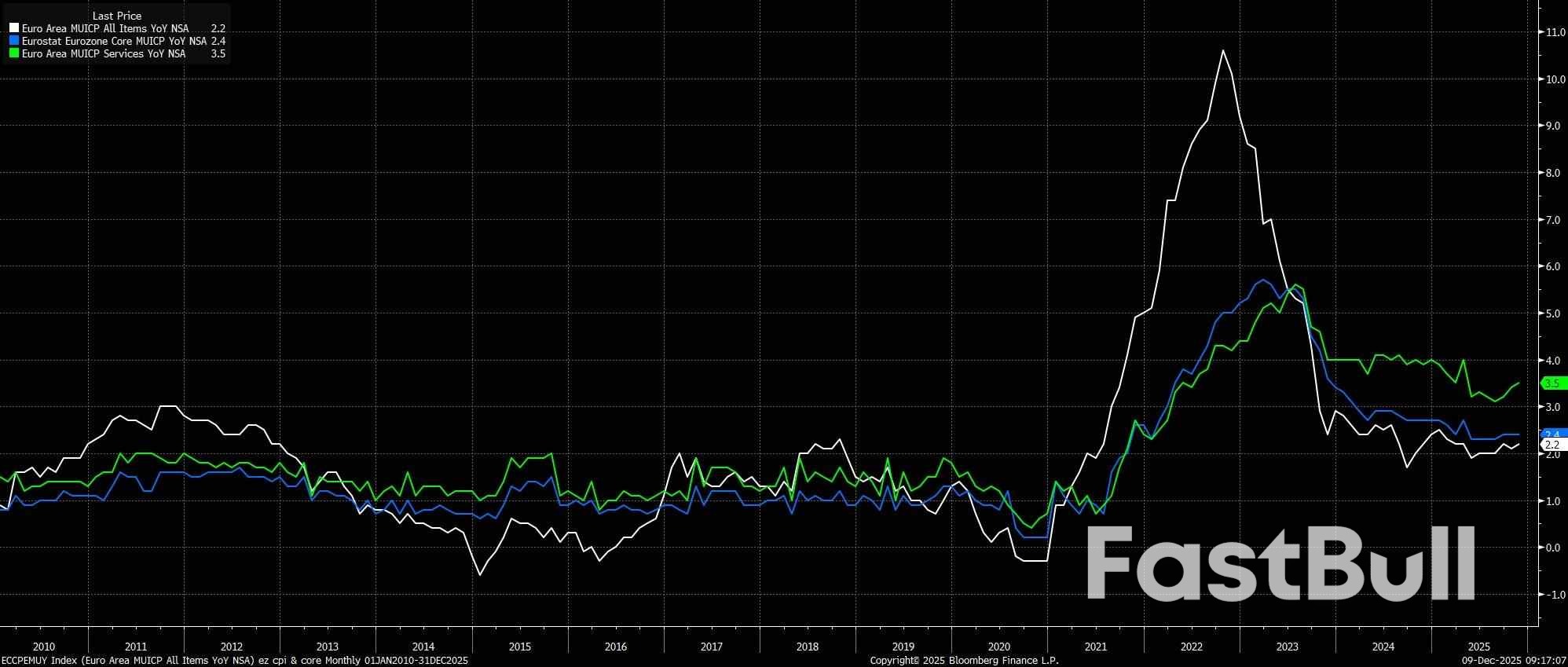

Perhaps the most interesting area of the December confab will be the updated round of staff macroeconomic projections, particularly the first read on how the projections see the eurozone economy evolving into 2028.

On inflation, the projections are again likely to point to headline CPI undershooting the 2% target both next year, and in 2027. While services inflation has started to bubble away once more in recent months, the beginning of 2026 will see a significant energy-induced base effect impact the data, dragging headline price metrics (much) lower in the first half of the year.

The two key areas of focus for the upcoming inflation projections will be, firstly, whether headline inflation is set to have risen back to 2% by the end of the horizon, in 2028. Secondly, if another undershoot is pencilled in for that year, the question becomes one of whether the Governing Council's doves view that as reason enough to begin pushing for further policy easing, in the early months of next year.

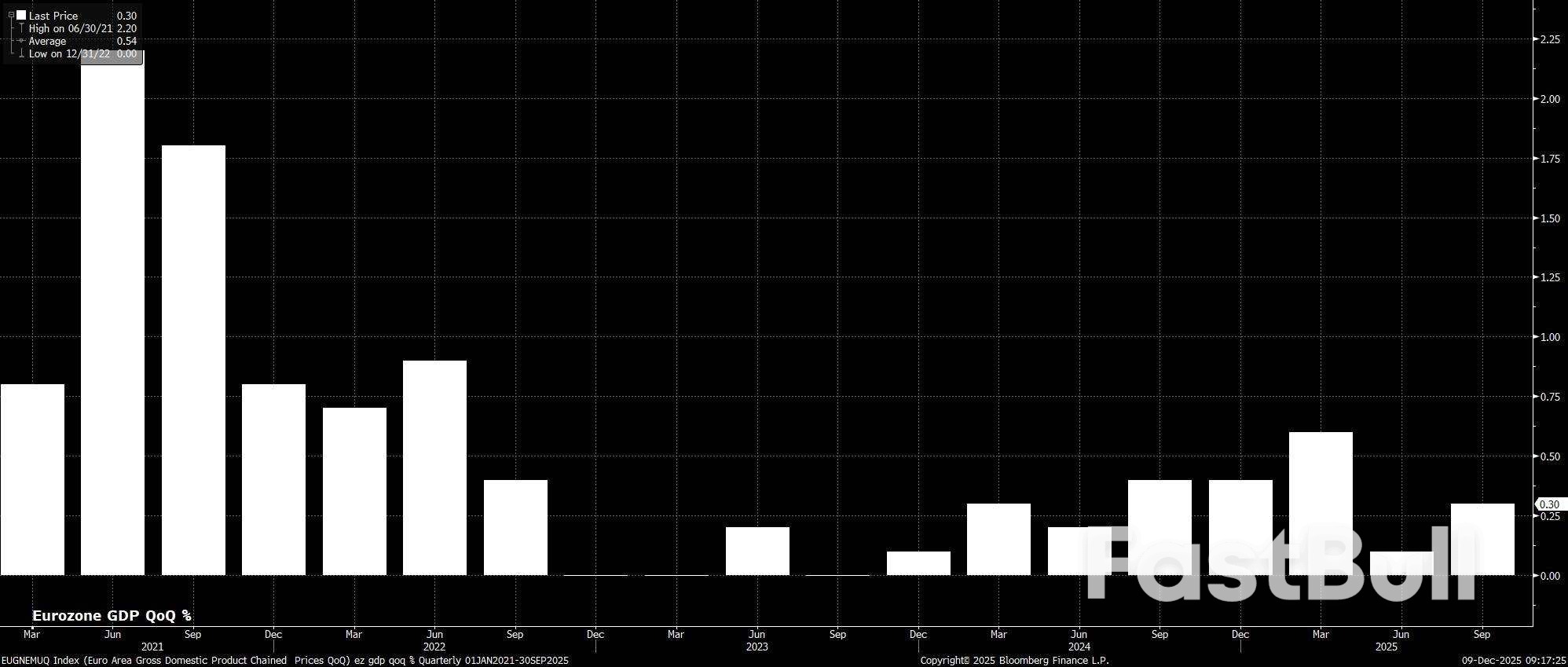

Meanwhile, on growth, there are likely to be relatively little by way of significant changes to the forecast GDP growth path, not least considering that many of the headwinds which have buffeted the eurozone economy in 2025 will increasingly turn to tailwinds as we move into the new year. Said tailwinds are relatively numerous, including increased certainty in terms of global trading relationships (especially with the US), as well as the lagged effects of ECB policy easing, plus a broadly looser fiscal stance next year.

Of course, said fiscal stance will not be entirely equal across the bloc. The vast majority of any fiscal boost next year will come from Germany, where not only is a significant increase on defence and infrastructure spending on the cards, but also a considerable number of tax changes which should provide a boost to personal consumption. That, in turn, at an aggregate level, is likely to offset the impact of further fiscal consolidation in both France, and Italy, which should result in the overall GDP growth forecast remaining broadly unchanged, seeing the eurozone work its way back towards potential growth in 2027 and 2028.

Turning to the post-meeting press conference, it seems highly unlikely that President Lagarde will seek to 'rock the boat' to any significant degree, thus raising the prospect of another turgid and dull affair, in keeping with the remarks delivered last time out, in October.

As a result, it is highly likely that Lagarde will simply reiterate the remarks that she made last time out, namely that policy is still in a 'good place', and that the ECB will ensure policy remains in such a place, while likely also confirming that the December decision to stand pat was a unanimous one.

As always, in addition to the presser, any post-meeting 'sources' stories will also be closely watched, particularly in determining how much weight, if any, policymakers are placing on the 2028 inflation forecasts.

On the whole, the December ECB confab is unlikely to be one that goes down as a game-changer in terms of the broader policy outlook.

While the GC's doves may seek to argue for another rate reduction early next-year, it remains likely that an overwhelming majority of policymakers see little-to-no need to shift to a more accommodative policy stance. Barring a material deterioration in economic growth, policymakers are likely to be relatively comfortable tolerating a modest inflation under-shoot, continuing to place more weight on 'hard' data, as opposed to staff projections.

As such, the base case remains that the ECB's easing cycle has now come to an end, and that the next rate move will indeed be a hike. Such a hike, however, is near-certain not to come next year, with the deposit rate set to remain at 2.00% through the end of 2026, and the matter of policy tightening one that will, eventually, be addressed in 2027.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

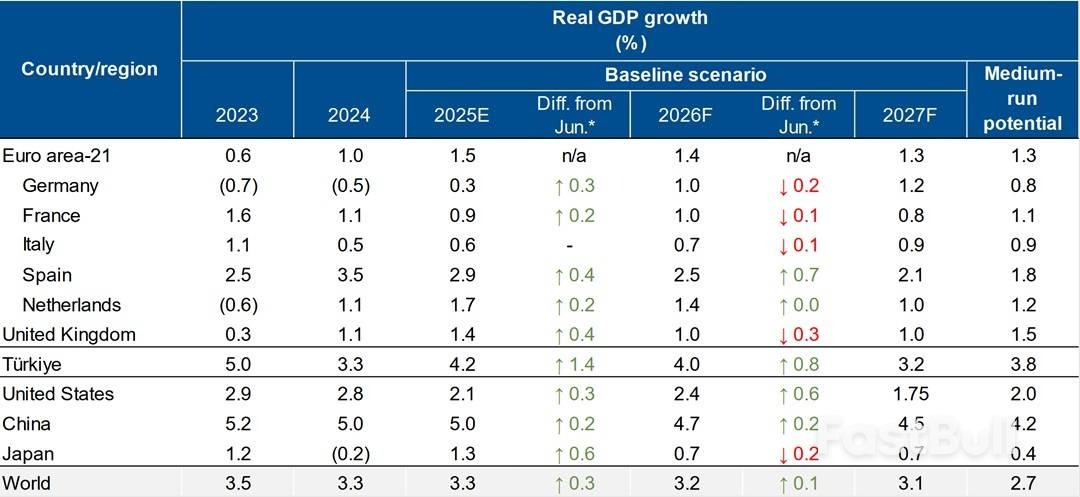

*Changes compared with June 2025's Global Economic Outlook. Negative growth rates presented in parentheses. Source: Scope Ratings forecasts, regional and national statistical offices, IMF.

*Changes compared with June 2025's Global Economic Outlook. Negative growth rates presented in parentheses. Source: Scope Ratings forecasts, regional and national statistical offices, IMF.

EURUSD 2026-2027 forecast: key market trends and future predictions

EURUSD 2026-2027 forecast: key market trends and future predictions Gold (XAUUSD) forecast 2026 and beyond: expert insights, price predictions, and analysis

Gold (XAUUSD) forecast 2026 and beyond: expert insights, price predictions, and analysis