Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Freddy94_

ID: 1815108

Despite incremental dovish shifts in the makeup of the FOMC voters, early 2026 is still likely to bring a pause to the Fed's easing cycle.

Despite incremental dovish shifts in the makeup of the FOMC voters, early 2026 is still likely to bring a pause to the Fed's easing cycle.

"New Year, New You" the saying goes, but for traders, the more salient phrase may be more along the lines of "New Fed, New Markets."

The FOMC will enter 2026 with a fresh slate of regional bank presidents and a leadership transition on the horizon, developments that could shift the markets current expectations for interest rate cuts at the world's most important central bank.

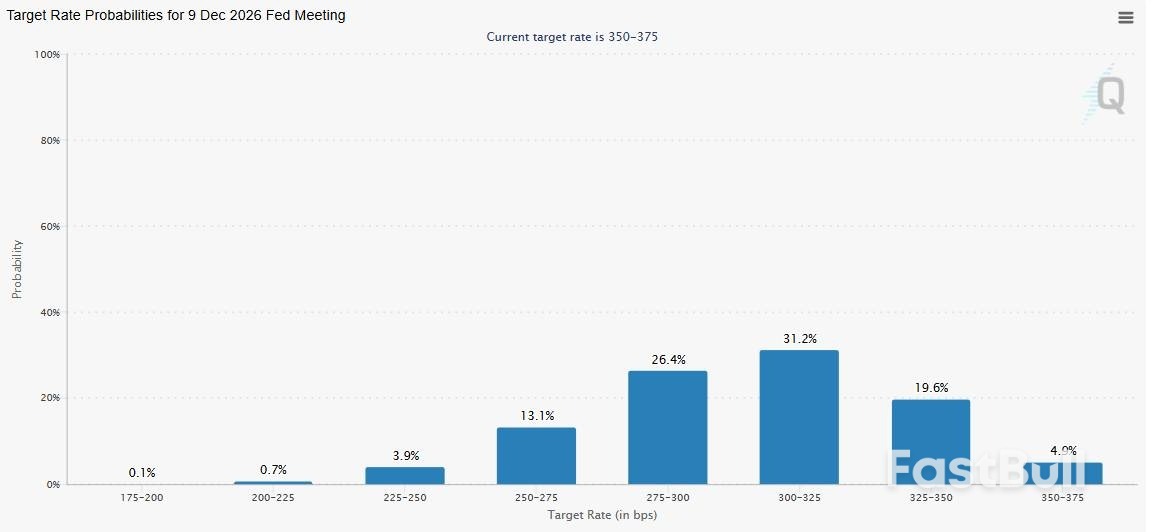

As the chart below shows, traders are currently pricing in a wide range between one and four 25bps interest rate cuts by the Fed in 2026, presenting clear trading opportunities for traders who are able to successfully handicap the outcome:

When it comes to the usual rotating voters, four Reserve Bank presidents will rotate off the FOMC in the new year: Susan Collins (Boston), Austan Goolsbee (Chicago), Alberto Musalem (St. Louis), and Jeff Schmid (Kansas City).

Their replacements are Anna Paulson (Philadelphia), Beth Hammack (Cleveland), Lorie Logan (Dallas), and Neel Kashkari (Minneapolis).

On balance, the outgoing voters lean hawkish (less inclined to cut interest rates overall. Recent quotes from the outgoing presidents follow:

Meanwhile, the new voters are more balanced, with two leaning hawkish and two more dovish:

Overall, the regular voter rotation could shift the Fed to a slightly more dovish or centrist outlook heading into the new year, though the move is likely to be marginal and economic data will still take precedence over broad ideological leans.

As you've no doubt heard, the bigger shift could be at the top: Chairman Powell's second four-year term ends in May, leaving an opening at the top for President Trump to nominate a(n almost certainly more dovish) successor early next year.

Names floated include Kevin Hassett, Kevin Warsh, and Chris Waller. Hassett and Warsh are widely viewed as favoring a more aggressive easing stance, citing growth risks and political priorities. Waller, meanwhile, has leaned hawkish historically but could pivot under a Trump mandate for faster cuts.

Beyond the appointment of a new Chairman in January, readers should also be aware that Trump-appointed Governor Stephen Miran exits January 31, 2026. In his so-far short tenure at the Fed, Miran has repeatedly dissented in favor of large 50bps rate cuts, making him the most dovish voice on the Board. In all likelihood, his replacement will reinforce a pro-easing tilt. Combined with a new Chair, this could shift the seven-member Board toward a majority favoring quicker normalization, even if regional presidents urge caution.

Despite these dovish shifts, early 2026 is still likely to bring a pause to the central bank's easing cycle, with the potential for interest rate cuts to accelerate through the middle of the year on the back of a new, more dovish Chairman, especially if employment data continues to deteriorate.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Daily Light Crude Oil Futures

Daily Light Crude Oil Futures