Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Turkey Trade Balance

Turkey Trade BalanceA:--

F: --

P: --

Germany Construction PMI (SA) (Nov)

Germany Construction PMI (SA) (Nov)A:--

F: --

P: --

Euro Zone IHS Markit Construction PMI (Nov)

Euro Zone IHS Markit Construction PMI (Nov)A:--

F: --

P: --

Italy IHS Markit Construction PMI (Nov)

Italy IHS Markit Construction PMI (Nov)A:--

F: --

P: --

U.K. Markit/CIPS Construction PMI (Nov)

U.K. Markit/CIPS Construction PMI (Nov)A:--

F: --

P: --

France 10-Year OAT Auction Avg. Yield

France 10-Year OAT Auction Avg. YieldA:--

F: --

P: --

Euro Zone Retail Sales MoM (Oct)A:--

F: --

P: --

Euro Zone Retail Sales YoY (Oct)A:--

F: --

P: --

Brazil GDP YoY (Q3)

Brazil GDP YoY (Q3)A:--

F: --

P: --

U.S. Challenger Job Cuts (Nov)

U.S. Challenger Job Cuts (Nov)A:--

F: --

P: --

U.S. Challenger Job Cuts MoM (Nov)A:--

F: --

P: --

U.S. Challenger Job Cuts YoY (Nov)A:--

F: --

P: --

U.S. Initial Jobless Claims 4-Week Avg. (SA)A:--

F: --

P: --

U.S. Weekly Initial Jobless Claims (SA)A:--

F: --

P: --

U.S. Weekly Continued Jobless Claims (SA)A:--

F: --

P: --

Canada Ivey PMI (SA) (Nov)

Canada Ivey PMI (SA) (Nov)A:--

F: --

P: --

Canada Ivey PMI (Not SA) (Nov)A:--

F: --

P: --

U.S. Non-Defense Capital Durable Goods Orders Revised MoM (Excl. Aircraft) (SA) (Sept)A:--

F: --

U.S. Factory Orders MoM (Excl. Transport) (Sept)A:--

F: --

P: --

U.S. Factory Orders MoM (Sept)A:--

F: --

P: --

U.S. Factory Orders MoM (Excl. Defense) (Sept)A:--

F: --

P: --

U.S. EIA Weekly Natural Gas Stocks ChangeA:--

F: --

P: --

Saudi Arabia Crude Oil ProductionA:--

F: --

P: --

U.S. Weekly Treasuries Held by Foreign Central BanksA:--

F: --

P: --

Japan Foreign Exchange Reserves (Nov)

Japan Foreign Exchange Reserves (Nov)A:--

F: --

P: --

India Repo Rate

India Repo RateA:--

F: --

P: --

India Benchmark Interest RateA:--

F: --

P: --

India Reverse Repo RateA:--

F: --

P: --

India Cash Reserve RatioA:--

F: --

P: --

Japan Leading Indicators Prelim (Oct)A:--

F: --

P: --

U.K. Halifax House Price Index YoY (SA) (Nov)--

F: --

P: --

U.K. Halifax House Price Index MoM (SA) (Nov)--

F: --

P: --

France Current Account (Not SA) (Oct)--

F: --

P: --

France Trade Balance (SA) (Oct)--

F: --

P: --

France Industrial Output MoM (SA) (Oct)--

F: --

P: --

Italy Retail Sales MoM (SA) (Oct)--

F: --

P: --

Euro Zone Employment YoY (SA) (Q3)--

F: --

P: --

Euro Zone GDP Final YoY (Q3)--

F: --

P: --

Euro Zone GDP Final QoQ (Q3)--

F: --

P: --

Euro Zone Employment Final QoQ (SA) (Q3)--

F: --

P: --

Euro Zone Employment Final (SA) (Q3)--

F: --

Brazil PPI MoM (Oct)--

F: --

P: --

Mexico Consumer Confidence Index (Nov)

Mexico Consumer Confidence Index (Nov)--

F: --

P: --

Canada Unemployment Rate (SA) (Nov)--

F: --

P: --

Canada Labor Force Participation Rate (SA) (Nov)--

F: --

P: --

Canada Employment (SA) (Nov)--

F: --

P: --

Canada Part-Time Employment (SA) (Nov)--

F: --

P: --

Canada Full-time Employment (SA) (Nov)--

F: --

P: --

U.S. Dallas Fed PCE Price Index YoY (Sept)--

F: --

P: --

U.S. PCE Price Index YoY (SA) (Sept)--

F: --

P: --

U.S. PCE Price Index MoM (Sept)--

F: --

P: --

U.S. Personal Outlays MoM (SA) (Sept)--

F: --

P: --

U.S. Core PCE Price Index MoM (Sept)--

F: --

P: --

U.S. UMich 5-Year-Ahead Inflation Expectations Prelim YoY (Dec)--

F: --

P: --

U.S. Core PCE Price Index YoY (Sept)--

F: --

P: --

U.S. 5-10 Year-Ahead Inflation Expectations (Dec)--

F: --

P: --

U.S. UMich Current Economic Conditions Index Prelim (Dec)--

F: --

P: --

U.S. UMich Consumer Sentiment Index Prelim (Dec)--

F: --

P: --

U.S. UMich 1-Year-Ahead Inflation Expectations Prelim (Dec)--

F: --

P: --

U.S. UMich Consumer Expectations Index Prelim (Dec)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

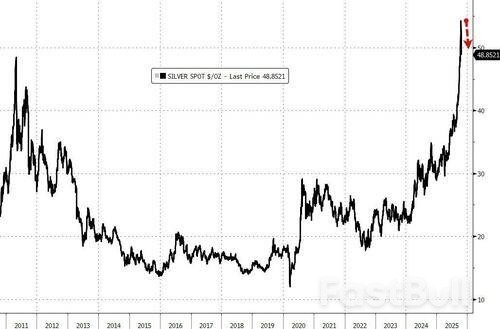

...don't panic!

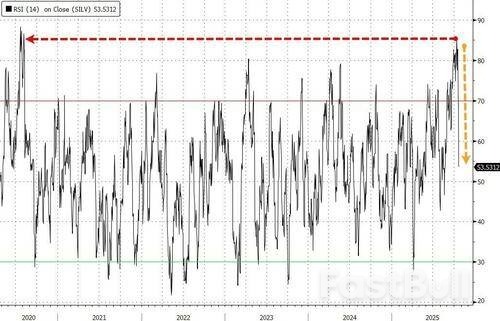

Precious metals have been clubbed like a bay seal this morning with Gold down 4%...

Silver is doing even worse, down almost7%...

A little context is useful...

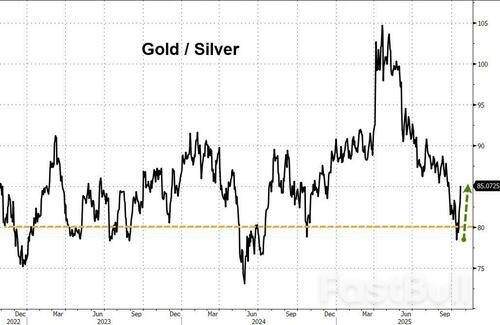

Meanwhile, we note that silver's dramatic underperformance came at critical support levels against gold (at the 80x ratio that has been significant for years)...

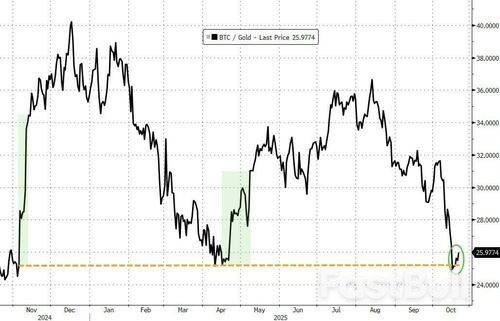

Additionally, relative to crypto, gold had got back to a key resistance level (that acted as serious support for the BTC/Gold ratio twice before - the election and liberation day)...

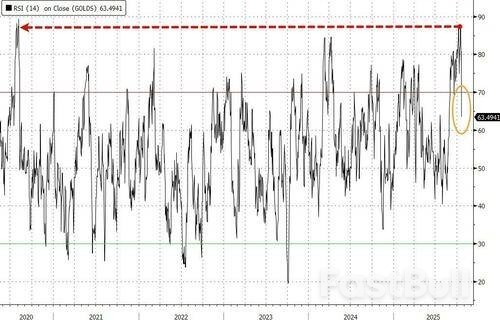

On the 'bright' side, this decline has dragged gold and silver back from perilously overbought levels...

UBS traders say that the next level to watch is the Oct. 15 low at 4165, before 4095/4100 which held on dips on Oct. 14; then it is the 4060 level which briefly capped the advance on Oct. 8/9.

It is no longer clear that Turkey provides a counterweight to Iran in the Middle East. Ankara has ambitions of its own.

Under the guise of leading a moderate Sunni axis and assisting the West against Iran’s radical Shia bloc, President Recep Tayyip Erdoğan’s Turkey is advancing a far more ambitious vision: the restoration of Turkey’s regional hegemony.Ankara’s economic and diplomatic ties with the West, including its NATO membership, are tactical tools to attain regional hegemony rather than genuine commitments to shared interests with the United States. Turkey’s ultimate objective is to reclaim the influence once enjoyed by the Ottoman Empire, which ruled vast swaths of Asia, Europe, and Africa for over six centuries. It follows that these ambitions threaten US, Western, and Israeli interests alike.

The close relationship between Turkey and Syria’s new president, Ahmed al-Shara, signals a dangerous realignment. Despite Western hopes that the collapse of the Iran-led axis in Syria would stabilize the region, the “Erdoğan-Shara axis” risks replacing one radical bloc with another.

Analysts such as Dr. Hay Eytan Cohen Yanarocak warn that Turkey is now the de facto powerbroker in Syria, directing events via its proxies. Turkish-led “joint operations commands” now reportedly coordinate activity across Syria, Jordan, Iraq, and Lebanon. While this may weaken Iran’s footprint, it empowers Ankara’s Islamist ambitions rather than promoting peacebuilding in Syria.Israel and Syria are now publicly admitting to pushing forward a peace agreement under the auspices of the United States. Yet given Erdoğan’s strong influence in Syria, these ambitions may face hardships—or worse, come to fruition under an innocent guise that would later entail heavy costs.

Even as Turkey seeks to curb Iranian and Russian influence, its hardly an ally for either Israel or the West. At an Organization of Islamic Cooperation (OIC) summit in June, Erdoğan openly backed Iran, a country recognized by the US as a State Sponsor of Terrorism, declaring, “We are optimistic that victory will be Iran’s,” while accusing Israel of igniting the region. His statements reveal both solidarity with sanctioned adversaries and claims to regional leadership over the Islamic world.

Meanwhile, Erdoğan continues to whitewash Hamas, recently describing it as a “resistance movement,” not a terrorist group, in an interview with Fox News. The Turkish president significantly escalated his rhetoric since the beginning of the Gaza war, accusing Israeli prime minister Benjamin Netanyahu of committing “genocide” in Gaza, “no less than what Hitler did.” He proudly leads massive rallies around the country, even going as far as threatening to “invade” Israel last year, “just as we entered Karabakh, just as we entered Libya.”

Indeed, Turkey has been hosting and harboring Hamas leaders on its soil for years, providing them with financial networks in defiance of US sanctions. Turkey’s ties with Hamas are longstanding and deep—politically, financially, and operationally. Hamas has established real estate companies, investment funds, and sham NGOs in Turkey, an enterprise whose scale has turned Turkey into a major Hamas financial hub, overseeing assets worth more than half a billion dollars.Hamas operatives have also received training in Turkey, returning with funds and directives to escalate attacks against Israel. Inter alia, this was proven in documents seized by the IDF in the Gaza Strip, exposing Hamas’ “Shadow Unit”—an undercover squad that left Gaza to Iran via Turkey for guidance and sponsorship in 2019. Ankara justifies its support through euphemisms that attempt to distinguish Hamas as a political, rather than a terrorist entity.

Meanwhile, Ankara has been building the largest military around the Mediterranean, expanding defense exports to $7.1 billion in 2024, and gaining combat experience in Syria, Libya, and the Caucasus. Though lacking stealth aircraft and a long-range ballistic missile arsenal, Turkey seeks to fill these gaps through US arms purchases.

Erdoğan’s threats go beyond Israel. In 2022, he threatened to launch ballistic missiles at Greece. Turkey still illegally occupies Northern Cyprus, a move firmly condemned by the European Union, of which Cyprus is part. During a July 2024 visit to the territory, Erdoğan declared his intention to establish a military base there.

The West’s hope that Turkey will counterbalance Iran’s Shia axis misreads Ankara’s intentions. As recent Iran-Turkey defense dialogues demonstrate, the two share growing military and intelligence cooperation despite sectarian differences. In 2025, Tehran’s defense minister hailed Turkey as a partner in facing “the challenges before the Islamic world.”Finally, Turkey’s nuclear ambitions should keep the West alert. Though Turkey lacks an independent nuclear arsenal, it hosts 50 US-controlled warheads and is now signaling a civilian nuclear drive that could evolve militarily. In September 2025, Ankara announced plans for domestic reactor development and nationwide bunker construction, including nuclear shelters.

Under Erdoğan, Turkish society has undergone systematic Islamization, a reverse of Atatürk’s secular legacy. The government cultivates a conservative Sunni extremist ideology, mirroring Iran’s revolutionary model.

Turkey courts Western engagement through trade, defense procurement, joint military exercises with the United States, and a rhetoric of partnership—as illustrated in Erdoğan’s latest visit to Washington to meet President Trump. Yet this dual-track strategy—appearing as a NATO ally while empowering jihadist actors—mirrors Iran’s former guise as a stabilizer against ISIS.Turkey’s assertive foreign policy, Islamist orientation, and cooperation with US-designated terror groups have increasingly rendered it an unreliable ally and emerging revisionist power. Its neo-Ottoman aspirations pose a strategic challenge that Washington, NATO, and Jerusalem can no longer afford to ignore.

It is now unavoidable to ramp up demands on Erdoğan before any further strengthening of the Turkish-Western alliance—if not reevaluate Turkey’s role in the West’s security architecture altogether. The West currently underestimates Turkey’s ambitions, focuses on short-sighted moves while ignoring its destabilizing and aggressive military moves and ties with radical terrorist groups.The logic of “the lesser evil”—choosing Turkey over Iran—has run its course. It is of the essence to shift from accommodation to vigilance with Turkey, scrutinizing its role in keeping regional stability and participation in the global security burden sharing, and its status as a legitimate Western partner. Until it changes its course, Ankara has now established itself as a strategic competitor, rather than a partner, to the US international security interests.

Gold prices fell over 3% on Tuesday, as the dollar firmed and investors booked profits after expectations of U.S. interest rate cuts and sustained safe-haven demand drove the yellow metal to a fresh record high in the previous session.

Spot goldwas down 3.5% at $4,203.89 per ounce, as of 09:05 a.m. ET (1305 GMT), its steepest fall since November 2020.

U.S. gold futuresfor December delivery fell 3.3% to $4,217.80 per ounce.

Prices scaled an all-time peak of $4,381.21 on Monday and have gained over 60% this year, bolstered by geopolitical and economic uncertainty, rate cut bets and sustained central bank buying.

"Gold dips were being bought as recently as yesterday, but the sharp jump in volatility at the highs over the past week is flashing caution and may encourage at least short-term profit-taking," said Tai Wong, an independent metals trader.

The dollar indexrose 0.4%, making bullion more expensive for holders of other currencies.

Wall Street looked poised for a calm start, with futures trimming earlier losses as investors assess a wave of largely positive earnings from corporate giants.

"Better risk appetite in the general marketplace early this week is bearish for the safe-haven metals," said Jim Wyckoff, senior analyst at Kitco Metals, in a note.

Traders now await the U.S. consumer price index (CPI) data, delayed due to the ongoing U.S. shutdown, due on Friday. September's figures are expected to show a 3.1% year-on-year rise. Markets expect that the Federal Reserve will cut interest rates by 25 basis points at its meeting next week.

Gold, a non-yielding asset, tends to benefit in a low-interest rate environment.

Investors are also awaiting U.S. President Donald Trump's upcoming meeting with Chinese President Xi Jinping next week.

Spot silverdropped 5.2% to $49.68 per ounce.

"Silver is stumbling badly today and has dragged the entire complex lower," said Wong.

"It appears we have a short-term top at $54 and while sentiment wobbles under $50, silver is likely to trade sideways with substantial volatility as long as gold remains relatively firm."

Elsewhere, platinumshed 4.3% to $1,568.25 and palladiumlost 5.8% to $1,410.

Canadian Dollar climbed across the board as markets enter into U.S. session, leading major currencies higher after domestic inflation data came in hotter than expected. Combined with this month’s firm employment figures, the data have made the case for a rate cut at the October 29 meeting a close call.

While the BoC maintain an easing bias and markets still expect more cuts ahead, the latest figures may prompt the BoC to pause this month and reserve ammunition for December, especially with signs that the domestic economy remains more resilient than feared.

Meanwhile, Yen stayed under sustained selling pressure. In a landmark parliamentary vote, Sanae Takaichi, leader of the ruling Liberal Democratic Party, was formally elected as Japan’s first female prime minister. The LDP’s new coalition partner, the Japan Innovation Party, helped deliver a comfortable win as opposition parties failed to field a unified challenger.

Takaichi swiftly unveiled her new Cabinet, naming Ryosei Akazawa, Japan’s chief tariff negotiator with the U.S., as trade minister to maintain momentum in bilateral talks. The new administration faces an immediate diplomatic challenge — the upcoming visit by U.S. President Donald Trump, which will test Japan’s approach to the ongoing tariff discussions and its broader defense cooperation with Washington.

Trade tensions between the U.S. and China remain another focal point. Chinese customs data showed rare earth magnet exports to the U.S. fell -28.7% mom in September to 420.5 tonnes — nearly 30% below last year’s levels. Reports suggest China tightened licensing procedures for rare earth exports in September, ahead of a broader regulatory expansion implemented in October. The move underscores Beijing’s intention to use resource controls as leverage in trade disputes, while Washington continues to forge strategic mineral alliances with partners such as Australia.

In currency markets, Loonie stands out as the day’s top performer, followed by Dollar and Sterling. Yen remains the weakest, trailed by the Swiss franc and Kiwi. Aussie and Euro trade in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.31%. DAX is up 0.17%. CAC is up 0.44%. UK 10-year yield is down -0.022 at 4.492. Germany 10-year yield is down -0.007 at 2.573. Earlier in Asia, Nikkei rose 0.27%. Hong Kong HSI rose 0.65%. China Shanghai SSE rose 1.36%. Singapore Strait Times rose 1.20%. Japan 10-year JGB yield fell -0.006 to 1.663.

Canada’s consumer prices accelerated more than expected in September. Headline CPI rose 2.4% yoy, up sharply from 1.9% in August and above consensus of 2.3%. The rebound was largely driven by a smaller year-ago decline in gasoline prices — down -4.1% compared with -12.7% in August — which created a notable base effect in the annual calculation.

Even so, underlying inflation momentum also firmed. Excluding gasoline, CPI rose 2.6% yoy, up from 2.4% in the previous month, signaling broader price pressures beyond energy. All three core inflation measures came in hotter than anticipated. CPI median held steady at 3.2%, beating expectations of 3.0%. CPI trimmed ticked up from 3.0% to 3.1%. CPI common accelerated from 2.5% yoy to 2.7%.

New Zealand recorded another sizeable trade deficit in September 2025, as import growth outstripped exports despite solid overseas demand. Statistics NZ data showed goods exports rose 19% yoy to NZD 5.8B. Imports increased 1.6% yoy to NZD 7.2B. The result was a monthly deficit of NZD -1.4B, versus expectation of NZD -6B and prior month’s NZD -1.2B.

Export strength was broad-based, led by double-digit gains to all major partners. Shipments to China jumped 24% yoy, Australia 28%, and Japan 23%, while sales to the U.S. and EU rose 10% and 15%, respectively.

On the import side, purchases from China climbed 16% yoy, while inflows from the EU and Australia rose 7.3% and 6.4%. Offsetting that, imports from the U.S. slumped -30%, and South Korea fell -4.8%.

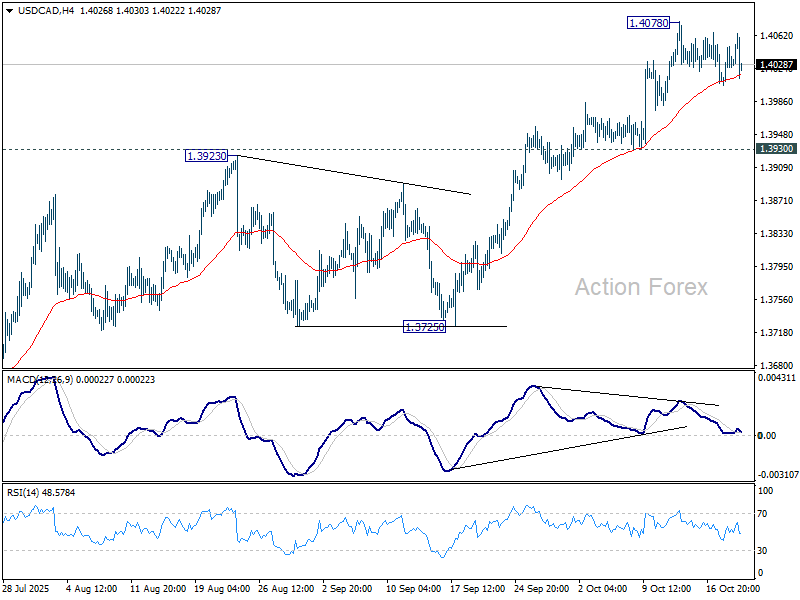

Daily Pivots: (S1) 1.4014; (P) 1.4032; (R1) 1.4059;

USD/CAD dips mildly in early US session, but stays well above 1.3930. Intraday bias remains neutral for more consolidations below 1.4078. But further rally is still expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up