Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Investors face a monumentally busy week ahead that includes rates decisions by the big G7 central banks, as well as a packed earnings calendar will see reports from five of the Mag-7. The Trump-Xi summit rounds off the week.

As noted earlier, investors face a monumentally important and extremely busy week ahead that includes rates decisions by four of the G7 central banks, with the Fed and BoC on Wednesday followed by the BoJ and ECB on Thursday. A packed earnings calendar will see reports from five of the Mag-7 (Microsoft, Alphabet, Meta, Apple and Amazon), together representing a quarter of the S&P 500 market cap. But ahead of all that, markets are in a buoyant mood this morning as US and China officials indicated that they have largely aligned a deal to ease trade tensions ahead of the Trump-Xi meeting this Thursday.

Starting with the US-China news, China's Ministry of Commerce said that the sides reached an initial consensus on a range of issues including an extension of the tariff truce, fentanyl, agricultural trade, export controls and shipping levies. In turn, US Treasury Secretary Bessent suggested that China would defer its new rare-earth export controls for one year and make "substantial" purchases of US soybeans, while the US threat of 100% tariffs on China was "effectively off the table". Bessent signaled that the agreed "framework" should allow Presidents Trump and Xi to have "a very productive meeting" when they meet on Thursday on the sidelines of the APEC summit. The details from that meeting should give a clearer sense whether this represents a genuine stabilisation in US-China trade relations or only a return to the uneasy trade truce in place before the rhetoric escalated earlier this month. Any reduction of the 20% fentanyl tariffs by the US will be one key barometer to watch.

In other weekend trade news, Trump signed trade framework pacts with Malaysia, Thailand, Vietnam and Cambodia. The countries will allow preferential access for US goods in return for tariff exemptions on some of their exports to the US, though many of exact details are still to be finalised. By contrast, Trump announced a 10% additional tariff on Canada amid a spat over an anti-tariff ad released by the government of Ontario. It's not clear whether USMCA-compliant goods would remain exempt from the extra 10% levy, which would mitigate much of its impact, but it's a reminder that tariffs remain a go-to policy tool for the US administration even if peak trade uncertainty is behind us.

Looking to the week ahead, a second consecutive 25bps Fed cut looks locked in for Wednesday's FOMC meeting, with markets pricing 49bps of cuts across the next two meetings. With a dearth of data and a still-divided FOMC, economists think Chair Powell is unlikely to provide clear signals on the policy path ahead, focusing more on topics including balance sheet policy and financial stability. Meanwhile, as we first discussed here first, the emerging baseline is that the Fed will this week announce an end to QT in response to the recent tightening in funding markets.

In Europe, the ECB is widely expected to keep the deposit rate steady at 2% for a third consecutive meeting. DB economists think ECB President Lagarde will again describe policy as "in a good place" and will be watching whether she maintains the net hawkish tone that she struck in July and September (see their preview here). The Bank of Japan (Thursday) is expected to maintain its current policy stance (see preview here), while the Bank of Canada is likely to deliver its own 25bp rate cut on Wednesday.

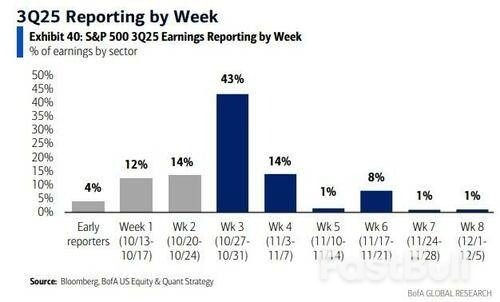

The Q3 earnings season will reach its apex this week with key reports due from Microsoft, Alphabet and Meta on Wednesday as well as Apple and Amazon on Thursday. The five biggest companies in the world after Nvidia now make up $15tn in total market capitalization or 25% of the S&P 500. The full list of key reports is in the week ahead calendar at the end as usual.

Overall, some 43% of the S&P500 by market will report this week.

On the data front, in the US the Conference Board's October consumer confidence readings (Tuesday) are likely to be the main indicator of note amid the government shutdown. In the euro area, Germany's ifo survey today will receive extra attention after last Friday's jump in the PMIs, the ECB's quarterly Bank Lending Survey (Tuesday) will precede its rates decision, and we'll get the October inflation readings for Germany and Spain on Thursday, followed by France, Italy and the Eurozone on Friday. In Asia, we have the October PMIs in China (Friday) as well as September retail sales, industrial production and the Tokyo CPI for October in Japan (Thursday).

Monday October 27

Tuesday October 28

Wednesday October 29

Thursday October 30

Friday October 31

Finally, looking at just the US, several key data releases will almost certainly be postponed this week because of the government shutdown, including the durable goods report scheduled for release on Monday, the advance goods trade balance scheduled on Wednesday, the Q3 advance GDP report scheduled on Thursday, and the core PCE inflation scheduled on Friday. The Department of Labor will also postpone the official release of the jobless claims report if the government shutdown continues through Thursday, but preliminary state-level claims data will likely be available. There are no speaking engagements by Fed officials this week, reflecting the FOMC's blackout period.

Monday, October 27

Tuesday, October 28

Wednesday, October 29

Thursday, October 30

Friday, October 31

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up