Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Euro Zone ZEW Economic Sentiment Index (Jan)

Euro Zone ZEW Economic Sentiment Index (Jan)A:--

F: --

P: --

Euro Zone Construction Output YoY (Nov)A:--

F: --

P: --

Euro Zone Construction Output MoM (SA) (Nov)A:--

F: --

Argentina Trade Balance (Dec)

Argentina Trade Balance (Dec)A:--

F: --

P: --

U.K. CPI MoM (Dec)

U.K. CPI MoM (Dec)A:--

F: --

P: --

U.K. Input PPI MoM (Not SA) (Dec)A:--

F: --

U.K. Core CPI MoM (Dec)A:--

F: --

P: --

U.K. Retail Prices Index MoM (Dec)A:--

F: --

P: --

U.K. Input PPI YoY (Not SA) (Dec)A:--

F: --

P: --

U.K. CPI YoY (Dec)A:--

F: --

P: --

U.K. Output PPI MoM (Not SA) (Dec)A:--

F: --

P: --

U.K. Output PPI YoY (Not SA) (Dec)A:--

F: --

P: --

U.K. Core Retail Prices Index YoY (Dec)A:--

F: --

P: --

U.K. Core CPI YoY (Dec)A:--

F: --

P: --

U.K. Retail Prices Index YoY (Dec)A:--

F: --

P: --

Indonesia 7-Day Reverse Repo Rate

Indonesia 7-Day Reverse Repo RateA:--

F: --

P: --

Indonesia Loan Growth YoY (Dec)A:--

F: --

P: --

Indonesia Deposit Facility Rate (Jan)A:--

F: --

P: --

Indonesia Lending Facility Rate (Jan)A:--

F: --

P: --

South Africa Core CPI YoY (Dec)

South Africa Core CPI YoY (Dec)A:--

F: --

P: --

South Africa CPI YoY (Dec)A:--

F: --

P: --

IEA Oil Market Report U.K. CBI Industrial Output Expectations (Jan)

IEA Oil Market Report U.K. CBI Industrial Output Expectations (Jan)A:--

F: --

U.K. CBI Industrial Prices Expectations (Jan)A:--

F: --

P: --

South Africa Retail Sales YoY (Nov)A:--

F: --

P: --

U.K. CBI Industrial Trends - Orders (Jan)A:--

F: --

P: --

Mexico Retail Sales MoM (Nov)

Mexico Retail Sales MoM (Nov)A:--

F: --

P: --

U.S. MBA Mortgage Application Activity Index WoW

U.S. MBA Mortgage Application Activity Index WoWA:--

F: --

P: --

Canada Industrial Product Price Index YoY (Dec)

Canada Industrial Product Price Index YoY (Dec)A:--

F: --

Canada Industrial Product Price Index MoM (Dec)A:--

F: --

U.S. Weekly Redbook Index YoY--

F: --

P: --

U.S. Pending Home Sales Index YoY (Dec)--

F: --

P: --

U.S. Pending Home Sales Index MoM (SA) (Dec)--

F: --

P: --

U.S. Construction Spending MoM (Oct)--

F: --

P: --

U.S. Pending Home Sales Index (Dec)--

F: --

P: --

Japan Imports YoY (Dec)

Japan Imports YoY (Dec)--

F: --

P: --

Japan Exports YoY (Dec)--

F: --

P: --

Japan Goods Trade Balance (SA) (Dec)--

F: --

P: --

Japan Trade Balance (Not SA) (Dec)--

F: --

Australia Employment (Dec)

Australia Employment (Dec)--

F: --

P: --

Australia Labor Force Participation Rate (SA) (Dec)--

F: --

P: --

Australia Unemployment Rate (SA) (Dec)--

F: --

P: --

Australia Full-time Employment (SA) (Dec)--

F: --

P: --

Turkey Capacity Utilization (Jan)

Turkey Capacity Utilization (Jan)--

F: --

P: --

Turkey Late Liquidity Window Rate (LON) (Jan)--

F: --

P: --

Turkey Overnight Lending Rate (O/N) (Jan)--

F: --

P: --

Turkey 1-Week Repo Rate--

F: --

P: --

U.S. Weekly Continued Jobless Claims (SA)--

F: --

P: --

U.S. Initial Jobless Claims 4-Week Avg. (SA)--

F: --

P: --

U.S. Real Personal Consumption Expenditures Final QoQ (Q3)--

F: --

P: --

U.S. Real Personal Consumption Expenditures Prelim QoQ (Q3)--

F: --

P: --

U.S. Weekly Initial Jobless Claims (SA)--

F: --

P: --

U.S. Real GDP Annualized QoQ Final (Q3)--

F: --

P: --

U.S. PCE Price Index Final QoQ (AR) (Q3)--

F: --

P: --

U.S. EIA Weekly Natural Gas Stocks Change--

F: --

P: --

U.S. Kansas Fed Manufacturing Composite Index (Jan)--

F: --

P: --

U.S. Kansas Fed Manufacturing Production Index (Jan)--

F: --

P: --

U.S. EIA Weekly Crude Stocks Change--

F: --

P: --

U.S. EIA Weekly Crude Demand Projected by Production--

F: --

P: --

U.S. EIA Weekly Cushing, Oklahoma Crude Oil Stocks Change--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Germany's 2026 growth outlook is fragile, per BDI, contingent on avoiding US tariffs and industrial reforms.

Germany's economy could see 1% growth in 2026, but only if it can avoid a new round of U.S. tariffs, the BDI industry association warned on Wednesday. The group stressed that despite the potential for growth, the outlook for the country's crucial industrial sector remains fragile.

Amid rising global uncertainty, the BDI urged the German government to center its policy agenda on improving competitiveness, stimulating growth, and creating jobs. The looming threat of fresh U.S. tariffs adds significant pressure to export-driven European economies like Germany's.

BDI President Peter Leibinger stated that Europe must meet these tariff threats with a united and confident response. He argued that only a competitive and resilient European Union can negotiate from a position of strength.

The BDI projects that Germany's industrial sector will likely expand at a slower pace than the overall economy this year, highlighting a key vulnerability.

"Only if we now give top priority to strengthening competitiveness and growth can we stop the downward trend in industrial production," Leibinger said.

To reverse this trend, the BDI outlined a series of reforms designed to invigorate the industrial base.

The association is advocating for measurable policy changes to unlock economic potential. Key proposals include:

• Cutting Bureaucracy: The BDI has already submitted 253 specific proposals to reduce red tape for businesses.

• Accelerating Permits: Speeding up the approval process for major industrial projects is seen as critical.

• Flexible Labor: The group called for allowing more flexible working-time models to adapt to modern economic demands.

Additionally, Leibinger suggested that bringing forward a planned cut in corporate tax could provide a direct growth impulse as early as 2026.

Ukraine has appointed a new defence minister with a clear mandate: overhaul Europe's largest military with a data-driven strategy designed to give its forces a decisive edge against Russia's larger army. Mykhailo Fedorov, formerly the country's digitalisation minister, was appointed last week by President Volodymyr Zelenskiy to drive innovation and fortify Ukraine's defenses.

Fedorov's plan centers on rewarding battlefield results and implementing advanced technology to counter Russia's superior equipment.

In his first remarks to reporters, Fedorov promised a sweeping reform of the defence ministry's management, emphasizing that performance will be the sole criterion for success. "If people don't demonstrate measurable results, they can't remain in the system," he stated.

His team has already compiled "high-quality data" to analyze ministry spending, identify potential savings, and address a significant budget gap. Fedorov stressed the importance of what he calls "the mathematics of war," underscoring that his approach will be built on systematic calculation and efficiency.

To translate this vision into action, the ministry will soon launch a mission control system for its drone operations. This platform will provide detailed data on the performance and effectiveness of drone crews, enabling better strategic decisions. A similar system is planned for artillery units.

"We need to see the full picture to simplify and speed up management decision-making," Fedorov explained. The ultimate goal is to increase Russian losses to an unsustainable level.

Ukraine plans to establish a system that allows its allies to use its vast repository of combat data to train their military artificial intelligence models. Since Russia's full-scale invasion in February 2022, Ukraine has accumulated an invaluable trove of battlefield information, including:

• Systematically logged combat statistics

• Millions of hours of drone footage

This real-world data is critical for training AI to recognize patterns and predict outcomes. Fedorov has previously described this data collection as one of Ukraine's key negotiating assets. Ukraine is already using AI technology from the U.S. data analytics firm Palantir.

Fedorov also noted that his team is receiving strategic advice from prominent think tanks, including the Center for Strategic and International Studies (CSIS) and RAND in the United States, as well as the Royal United Services Institute (RUSI) in the UK, as he seeks to more actively integrate allies into defense projects.

This month, Ukraine will begin testing a domestically produced replacement for China's widely used DJI Mavic drone, which serves as a primary reconnaissance tool for both sides of the conflict. The manufacturer's name was not disclosed.

This move addresses concerns about over-reliance on Chinese technology, especially given Beijing's close ties with Moscow. "We will have our own Mavic analogue: the same camera, but with a longer flight range," Fedorov confirmed.

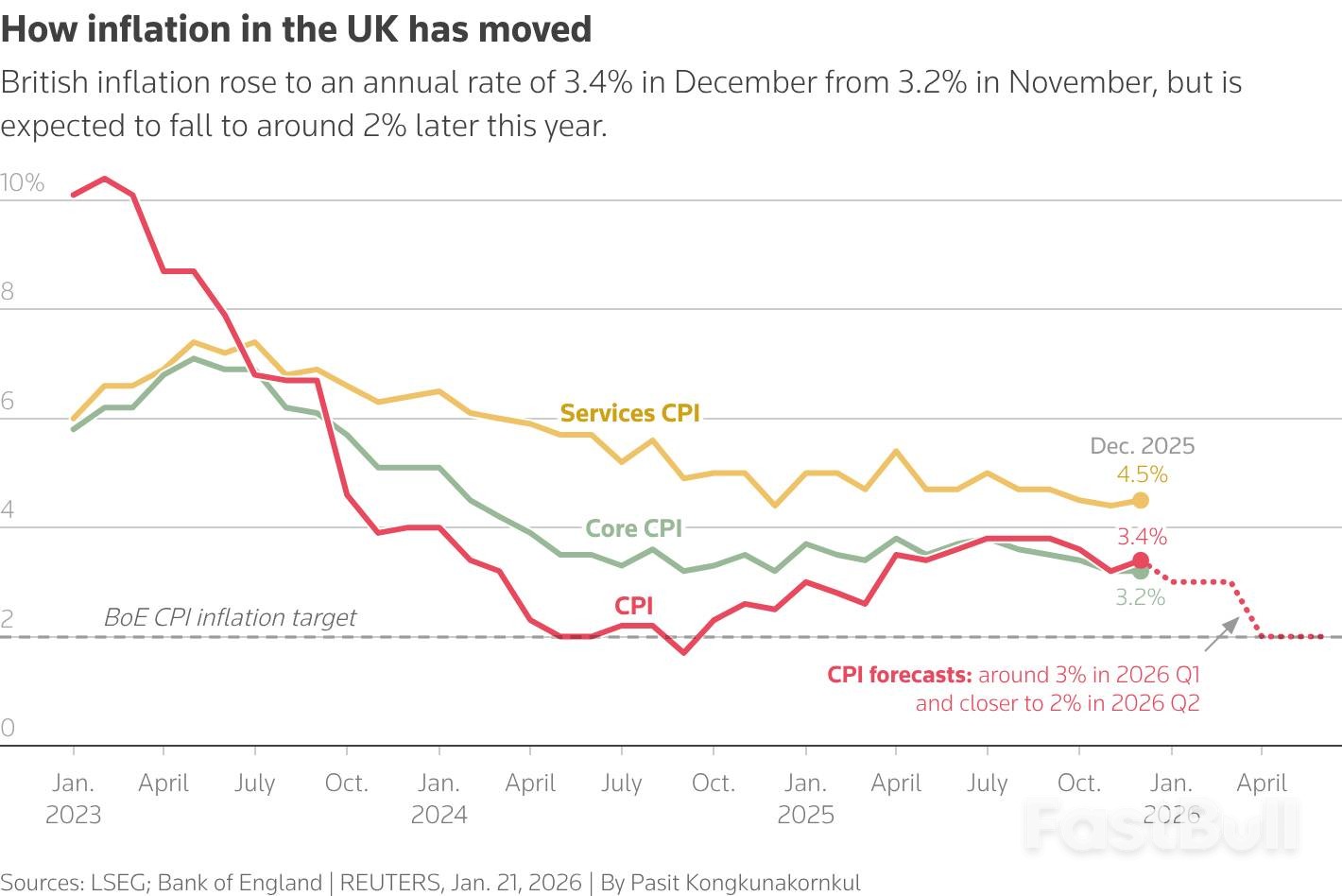

UK inflation unexpectedly climbed for the first time since July, hitting 3.4% in December and complicating the path toward price stability. Despite the increase, investors and economists largely believe the upward blip won't derail the Bank of England's plan to cut interest rates later this year.

Official data shows the Consumer Price Index (CPI) rose from 3.2% in November, surpassing the 3.3% that economists had forecasted.

Key takeaways from the latest report include:

• Headline Inflation: Reached 3.4% in December.

• Primary Drivers: Price hikes were mainly caused by increased tobacco duties and seasonal airfare costs.

• Market Reaction: Financial markets remained steady, with expectations for 2026 rate cuts unchanged.

• Services Inflation: A crucial metric for the central bank, services price inflation edged up to 4.5% from 4.4%, aligning perfectly with forecasts.

The primary forces behind the December inflation increase were higher prices for tobacco products, following a rise in duties, and the typical surge in airfares around the Christmas holiday period.

While the headline number was higher than expected, Adam Deasy, an economist at PwC, described the event as a "speed-bump, rather than an indication we are veering off course on the road to price stability."

This sentiment is shared across the market, as the underlying drivers are seen as temporary rather than a sign of persistent inflationary pressure.

Despite the uptick, the Bank of England (BoE) is widely expected to proceed with interest rate cuts in 2026. The central bank is focused on the broader trend, which still points toward a significant slowdown in price growth over the coming months.

BoE Governor Andrew Bailey has previously stated that he expects inflation to fall close to the bank's 2% target by April or May. Consequently, the latest data did little to move the pound or alter market bets on future monetary policy.

"The Bank of England will... not be worried by these numbers," noted Nicholas Crittenden, an economist from the National Institute of Economic and Social Research. He added, "We still predict one cut in Bank Rate in the first half of this year."

Financial markets are currently pricing in one or possibly two quarter-point rate cuts by the BoE in 2026. This reflects confidence that the disinflationary trend will overcome short-term volatility.

While the domestic inflation picture appears manageable, external factors pose a significant risk. Governor Bailey recently highlighted that the BoE is worried about how markets are reacting to geopolitical developments.

These concerns are materializing in energy markets. British natural gas futures have surged by approximately 25% in the last two weeks, partly due to deteriorating relations with the United States, a key supplier of liquefied natural gas. The tensions stem from President Donald Trump's threats of tariffs on European allies who oppose his Greenland takeover plan. An escalation could disrupt supply chains and push energy costs higher, complicating the BoE's inflation fight.

Even with the December surprise, Britain's consumer price and services inflation rates are running slightly below the BoE's own projections from its November forecasts. However, the UK continues to have the highest inflation rate in the Group of Seven, paired with sluggish economic growth.

Data on producer prices, which can be a leading indicator for consumer inflation, showed a sharp increase in the services sector during the fourth quarter, rising to 2.9% from 2.0%. Meanwhile, output price inflation for manufacturers remained stable.

The BoE's Monetary Policy Committee last cut the Bank Rate to 3.75% in December, but the decision was not unanimous. Nearly half of its members voted to hold rates steady, citing concerns about persistent inflation, a signal that the debate over policy easing is far from over.

Global markets appeared to stabilize somewhat today after the sharp U.S. selloff overnight, which saw the DOW suffer its worst one-day loss since October. That said, the underlying source of stress has not faded. Greenland-related tensions remain unresolved, with no visible path toward de-escalation. The current stabilization looks more like position-squaring, rather than renewed confidence.

For now, markets are simply catching their breath, awaiting the next catalyst. Attention has shifted to World Economic Forum, where US President Donald Trump is due to deliver a closely watched address later today. Trump's speech comes amid soaring tensions between the U.S. and Europe over Danish territory Greenland, which Trump wants the U.S. to acquire. Markets are watching closely for any signal of escalation, moderation, or strategic ambiguity.

On Tuesday, Trump declined to specify how far he is prepared to go to achieve that objective, telling reporters bluntly, "You'll find out." He has previously refused to rule out military action and has threatened new tariffs on multiple European countries if they block the takeover bid.

Those threats have already left their mark on markets this week. The renewed risk of a transatlantic trade war pushed U.S. Treasuries sharply lower, while Gold surged to new record highs.

U.S. 10-year yield briefly breached 4.3% overnight, before settling around 4.295%. Speaking in Davos, Scott Bessent sought to play down concerns about the bond selloff. He said he was not worried about Treasuries, dismissing speculation that European investors were pulling back.

Asked specifically about Denmark, Bessent said its holdings were "irrelevant," noting they amounted to less than USD 100 million, and added that Denmark has been selling Treasuries for years. He emphasized that the U.S. has seen record foreign investment in Treasuries overall.

Instead, Bessent pointed to Japan, arguing that the recent Japanese bond selloff following a snap election announcement had spilled over into global markets. He dismissed talk of European liquidation as originating from a single analyst at Deutsche Bank. Bessent added that Deutsche Bank's CEO had personally contacted him to say the bank did not stand by the analyst report, accusing "fake news media" of amplifying unfounded fears.

Meanwhile, Gold climbed above 4,800, extending a powerful rally driven by tariff threats, geopolitical instability, falling real rates, and ongoing diversification away from the dollar. After a record 2025, Gold has entered 2026 with momentum firmly intact. According to analysts surveyed by the London Bullion Market Association, prices are increasingly expected to rise above 5,000 this year, citing lower U.S. real yields, continued Fed easing, and sustained central-bank diversification.

In FX performance terms this week so far, Dollar sits at the bottom, followed by Yen and Sterling, while Kiwi leads, followed by Swiss Franc and Aussie, with Euro and Loonie in the middle.

In Asia, Nikkei fell -0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.08%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield stabilized and fell -0.056 to 2.288. Overnight, DOW fell -1.76%. S&P 500 fell -2.06%. NADSAQ fell -2.39%. 10-year yield rose 0.064 to 4.295.

ECB President Christine Lagarde said she expects only a "minimal" inflationary impact from additional U.S. tariffs, arguing that Eurozone price pressures remain firmly under control. Speaking to RTL, Lagarde noted that inflation is currently around 1.9%, leaving little scope for tariffs to materially disrupt the ECB's inflation outlook.

Though, she acknowledged that the impact would not be evenly distributed, with Germany likely more exposed than France given its export-heavy manufacturing base. However, Lagarde argued that Europe would be far more resilient if it focused on removing non-tariff trade barriers within the EU, strengthening internal trade and competitiveness rather than reacting defensively to external shocks.

Lagarde's sharper warning was reserved for uncertainty, not tariffs themselves. Referring to renewed threats from US President Donald Trump, who has vowed to impose escalating tariffs on several European countries over Greenland, she said the "constant reversals" and unpredictability pose a more serious risk. Trump, she added, often takes a transactional approach, setting demands at "sometimes completely unrealistic" levels.

UK inflation firmed at the end of 2025, with headline pressure coming in slightly hotter than expected. CPI rose to 3.4% yoy in December, up from 3.2% and above expectations of 3.3%, while prices increased 0.4% mom, pointing to ongoing near-term inflation momentum.

The upside in headline inflation, however, masked relative stability in underlying pressures. Core CPI—excluding energy, food, alcohol and tobacco—was unchanged at 3.2% yoy, undershooting expectations of 3.3%, and marking the joint-lowest reading since December 2024. Core inflation was last lower in September 2021, reinforcing the view that underlying disinflation progress, while slow, remains intact.

By component, services inflation edged up to 4.5% yoy from 4.4%, keeping the sector firmly in focus for the BoE, while goods inflation rose to 2.2% from 2.1%.

NZD/USD has surged sharply this week and is now pressing key near-term resistance at 0.5852, as shifting global risk dynamics unexpectedly favor the Kiwi. With Dollar and Euro under pressure from Greenland-related geopolitical tensions, both New Zealand dollar and Australian Dollar have surprisingly emerged as relative safe havens, benefiting from stable domestic backdrops and distance from the dispute.

At the same, Yen remains under pressure, weighed down by an aggressive selloff in Japanese government bonds as markets price in post-election fiscal expansion. That divergence has left antipodean currencies unusually well-bid, along with Swiss Franc.

For Kiwi, attention now turns to New Zealand Q4 CPI, due Friday in Asia. The annual rate is expected to hold at 3.0%, right at the top of the RBNZ's 2–3% target band. With the Official Cash Rate at 2.25%, markets broadly agree the RBNZ has completed its easing cycle. The open question is timing of the next hike, not whether one eventually comes. CPI overshoot would sharply pull forward expectations and offer fresh support to NZD.

That focus will intensify at the February 18 OCR review, the first major policy decision under new Governor Anna Breman. Markets will be listening closely to the tone of the post-meeting press conference for clues on whether Breman leans hawkish, dovish, or neither.

Technically, NZD/USD's dip to 0.5710 earlier this month was a little deeper than expected. But that didn't alter the overall structure. The corrective down trend from 0.6119 (2025 high) should have completed with three waves down to 0.5580.

Firm break of 0.5852 will resume the whole rally from 0.5580 and target 100% projection of 0.5580 to 0.5852 from 0.5710 at 0.6015. Decisive break of 0.6015 will solidify that NZD/USD is in an impulsive move that should be resuming whole rise from 0.5484 (2025 low) through 0.6119. In any case, outlook will now stay bullish as long as 0.5710 support holds.

Daily Pivots: (S1) 184.33; (P) 184.90; (R1) 186.02;

EUR/JPY retreated ahead of 185.55 resistance as range trading continues. Intraday bias remains neutral for the moment. With 182.60 support intact, further rally is expected. On the upside, break of 185.55 will resume larger up trend to 186.31 projection level. Firm break there will target 138.2% projection of 151.06 to 173.87 from 172.24 at 189.94. However, sustained break of 182.60 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 181.83) and below.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.58) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

| GMT | CCY | EVENTS | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 07:00 | GBP | CPI M/M Dec | 0.40% | 0.40% | -0.20% | |

| 07:00 | GBP | CPI Y/Y Dec | 3.40% | 3.30% | 3.20% | |

| 07:00 | GBP | Core CPI Y/Y Dec | 3.20% | 3.30% | 3.20% | |

| 07:00 | GBP | RPI M/M Dec | 0.70% | 0.50% | -0.40% | |

| 07:00 | GBP | RPI Y/Y Dec | 4.20% | 4.10% | 3.80% | |

| 07:00 | GBP | PPI Input M/M Dec | -0.20% | -0.10% | 0.30% | 0.50% |

| 07:00 | GBP | PPI Input Y/Y Dec | 0.80% | 1.10% | ||

| 07:00 | GBP | PPI Output M/M Dec | 0.00% | 0.10% | 0.10% | |

| 07:00 | GBP | PPI Output Y/Y Dec | 3.40% | 3.40% | ||

| 07:00 | GBP | PPI Core Output M/M Dec | -0.10% | 0.00% | 0.10% | |

| 07:00 | GBP | PPI Core Output Y/Y Dec | 3.20% | 3.50% | 3.60% | |

| 13:30 | CAD | Raw Material Price Index Dec | 0.30% | |||

| 13:30 | CAD | Industrial Product Price M/M Dec | 0.90% | |||

| 15:00 | USD | Pending Homeles M/M Dec | 3.30% |

The conflict over the U.S. Federal Reserve's independence has intensified, with Treasury Secretary Scott Bessent openly criticizing Fed Chair Jerome Powell's decision to attend a high-stakes Supreme Court hearing. The case centers on President Donald Trump's attempt to fire a sitting central bank governor, a move that could reshape the Fed's political autonomy.

Bessent argued that Powell's presence at the court proceedings would be a "real mistake" that could further politicize the central bank. The controversy is escalating just as the Trump administration prepares to announce its nominee to lead the Fed, with a decision expected as early as next week.

In an interview with CNBC, Bessent was direct in his assessment of Powell's plan to attend the Supreme Court's oral arguments.

"If you're trying not to politicize the Fed, for the Fed chair to be sitting there, trying to put his thumb on the scale, is a real mistake," Bessent said.

Powell’s planned attendance is widely seen as a symbolic gesture amid an ongoing clash with the administration. The U.S. Department of Justice has previously threatened a criminal investigation against him, which Powell labeled a "pretext" to influence monetary policy.

The Supreme Court is set to hear arguments on Wednesday regarding the legality of President Trump's effort to remove Federal Reserve Governor Lisa Cook. While the case proceeds, lower courts have allowed Cook to remain in her position.

The attempt to fire Cook, based on alleged misstatements on mortgage documents from before her time at the Fed, has been criticized as a thinly veiled effort to pressure the central bank into lowering interest rates or to open up board seats for Trump to fill. Cook has not been charged with any violations related to the mortgages.

This case tests the legal standard for removing a Fed governor, who serves a 14-year term and can only be dismissed "for cause." This protection is designed to shield the central bank from short-term political influence, and the "for cause" standard has never been tested in court.

The situation has also drawn scrutiny from Congress. Democratic senators Elizabeth Warren and Dick Durbin have called on the Trump administration to release all records related to the probe into the Fed. Their request includes any communications between the Justice Department, the Treasury, and the White House concerning Powell, Cook, and the Fed's interest-rate decisions.

Critics of the president worry that the administration's actions and rhetoric are a direct threat to the U.S. central bank's long-held independence. The ongoing tension is particularly significant as President Trump's choice to succeed Powell, whose term ends in May, is imminent.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up