Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The Federal Reserve’s (Fed) annual gathering in the Rocky Mountains is usually a time for central bankers and their wonky friends to kick back, discuss a few complicated economic topics and then go for a hike in the shadow of Grand Teton.

The Federal Reserve’s (Fed) annual gathering in the Rocky Mountains is usually a time for central bankers and their wonky friends to kick back, discuss a few complicated economic topics and then go for a hike in the shadow of Grand Teton.This year, the Fed’s Jackson Hole symposium, which wrapped up Saturday, was at times a tense affair and drove home how difficult the path ahead is for the US central bank.

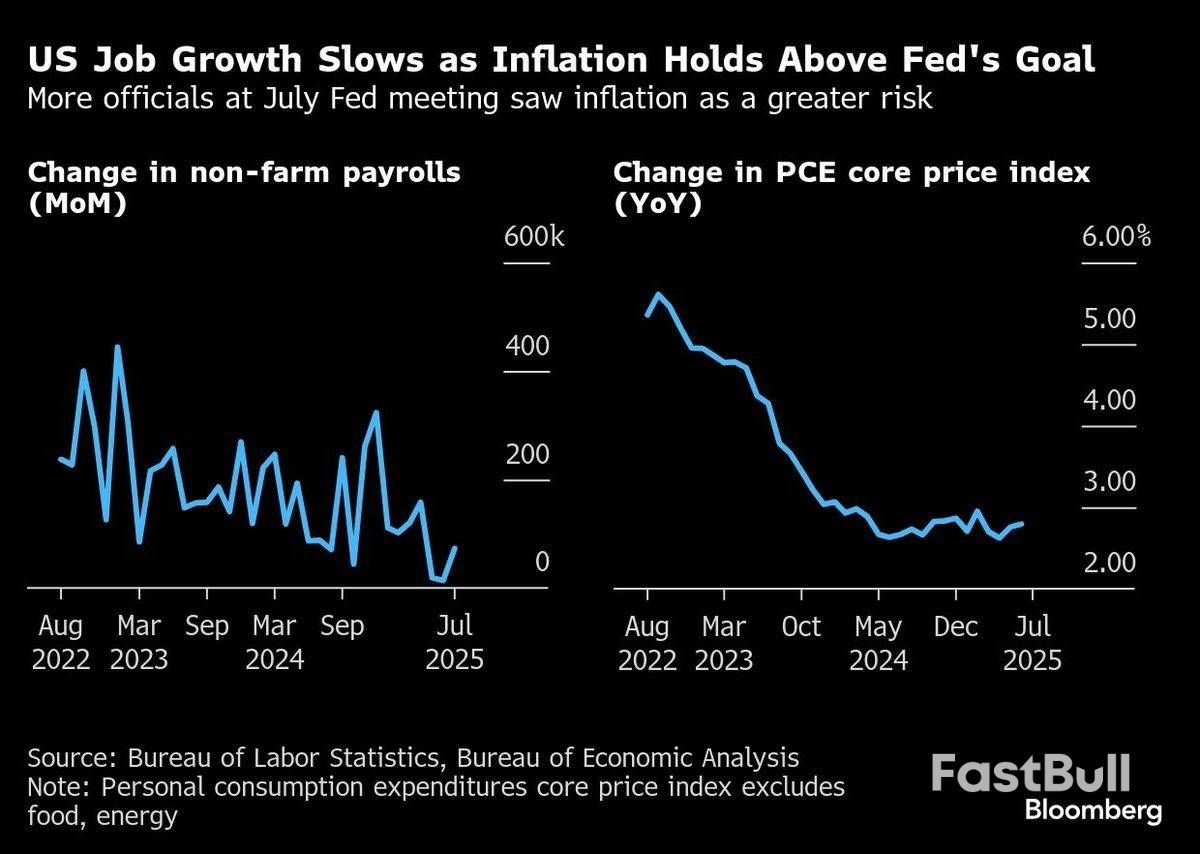

On Friday, Chair Jerome Powell used his keynote speech to signal the Fed is headed for an interest-rate cut as soon as its next policy meeting in September. Yet there are clear divisions among policymakers over whether that’s the right call. Powell, himself, noted the economy has handed Fed officials a “challenging situation”.Policymakers are grappling with inflation that’s still above their 2% goal — and rising — and a labour market that’s showing signs of weakness. That unnerving reality, which pulls policy in opposite directions, is made worse by a high degree of uncertainty about how each of those factors will evolve over the coming months.

“We’re getting some cross-currents and it’s in a difficult environment,” Chicago Fed President Austan Goolsbee said in an interview on the sidelines of the conference. “I always say the hardest job the central bank has is to get the timing right at moments of transition.”The conference also highlighted the political pressures weighing on the Fed. Those are likely to intensify in coming months as President Donald Trump looks to put his stamp on what may be the most prominent federal institution to have so far escaped his overhaul attempts.

As Powell delivered his speech Friday morning, Trump said he would fire Fed Governor Lisa Cook if she didn’t resign over recent allegations that she committed mortgage fraud. It’s the latest attempt by the administration to pressure the Fed from multiple angles as Trump relentlessly pushes for lower interest rates.Security for the event was noticeably heightened compared to recent years, adding to the tension at the gathering. Officers from the Fed Police, US Park Police and Teton County Sheriff’s Office, some in military-style fatigues and carrying weapons, were a constant presence.

Earlier Friday morning, officers had to remove one person, the Trump-backer and Fed gadfly James Fishback, after he confronted Cook in the lobby of the lodge and shouted questions about the mortgage controversy.

Powell, in what was likely his final Jackson Hole speech at the helm of the Fed, detailed the cloudy signals coming from the economy.While the effect of tariffs on prices is now visible, there are still questions about whether that will reignite inflation in a more persistent way, he said. He called the labour market’s current status — with both falling demand for, and declining supply of workers — “curious”.

Even with those uncertainties, Powell opened the door to a rate cut at the Fed’s Sept 16-17 meeting, though it wasn’t as clear a signal as at last year’s conference. Then, the labour market was deteriorating but inflation worries had receded, and many policymakers shared a desire to cut soon. The backing is not nearly as strong this year.

Recent data have shown inflation has stalled above the Fed’s 2% goal, with some measures indicating that price pressures may be spilling over to products and services not directly impacted by tariffs. Meantime, while hiring has slowed significantly over the summer, other labour market indicators, like the low level of unemployment, paint a more stable picture.Without much clarity on how the economy will unfold, disagreements over how to proceed are festering among policymakers. Already, two governors dissented at the Fed’s July meeting, when officials didn’t cut rates. If they do cut in September, others may dissent in the opposite direction.

Policy disagreements could grow in the coming months as Trump names new officials to vacancies at the Fed and Powell’s term as chair ends in May. The president has already tapped Stephen Miran, who chairs his Council of Economic Advisers, to fill an open slot on the Fed board that expires in January.

The discord among Fed officials comes at a time when the central bank is facing intense scrutiny from the White House. The topic seeped into conversations over coffee, during meals and in between sessions, even if there wasn’t much outright discussion of it during official conference proceedings.

Karen Dynan, an economics professor at Harvard University and frequent attendee of the conference, said she wasn’t surprised that central bankers didn’t want to wade into conversations about politics. Still, she said the conference set an example of how big-picture economic issues should be approached.

“This year it feels particularly meaningful that we have a bunch of papers that are grounded in good economics done by people who are prominent experts,” Dynan said. “These are not problems that can be solved by thinking about one’s intuition or talking to just a circle of people around you — you really need this sort of expertise.”

One issue that received less attention was the new framework Powell unveiled in his speech.The document, which will guide policymakers as they pursue their inflation and employment goals, is the culmination of a months-long review of the previous one, implemented in 2020. The new strategy removes some of the language that more narrowly focused on the pre-pandemic challenge of persistently low inflation.

It’s a return to basics and sets the Fed up to more clearly focus on its mandates of maximum employment and stable prices, said Carolin Pflueger, associate professor at the University of Chicago Harris School of Public Policy.In his remarks, Powell “emphasised that his job is inflation and unemployment, and that can only be achieved within an independent Fed,” Pflueger said. “I think people appreciate that.”

That appreciation became apparent when Powell was greeted Friday morning with a standing ovation from economists and policymakers from around the world — and not for the first time this year.For them Fed independence is not only a matter of principle but also practicality, since decisions taken in Washington inevitably come with consequences that spread far beyond.

The euro strengthened by 1% against the dollar following Powell’s remarks, adding downside risks to euro-area inflation that’s already seen falling to 1.6% next year.“If a cut does come and reflects slower US growth, that probably means slower growth for them given the size of the US,” Maurice Obstfeld, a senior fellow at the Peterson Institute for International Economics and the former chief economist at the International Monetary Fund, said of the euro area and other economies.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up