Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.K. 3-Month RICS House Price Balance (Nov)

U.K. 3-Month RICS House Price Balance (Nov)A:--

F: --

P: --

Australia Employment (Nov)

Australia Employment (Nov)A:--

F: --

Australia Full-time Employment (SA) (Nov)A:--

F: --

P: --

Australia Unemployment Rate (SA) (Nov)A:--

F: --

P: --

Australia Labor Force Participation Rate (SA) (Nov)A:--

F: --

P: --

Turkey Retail Sales YoY (Oct)

Turkey Retail Sales YoY (Oct)A:--

F: --

P: --

South Africa Mining Output YoY (Oct)

South Africa Mining Output YoY (Oct)A:--

F: --

P: --

South Africa Gold Production YoY (Oct)A:--

F: --

P: --

Italy Quarterly Unemployment Rate (SA) (Q3)

Italy Quarterly Unemployment Rate (SA) (Q3)A:--

F: --

P: --

IEA Oil Market Report Turkey 1-Week Repo Rate

IEA Oil Market Report Turkey 1-Week Repo RateA:--

F: --

P: --

South Africa Refinitiv/Ipsos Primary Consumer Sentiment Index (PCSI) (Dec)A:--

F: --

P: --

Turkey Overnight Lending Rate (O/N) (Dec)A:--

F: --

P: --

Turkey Late Liquidity Window Rate (LON) (Dec)A:--

F: --

P: --

U.K. Refinitiv/Ipsos Primary Consumer Sentiment Index (PCSI) (Dec)A:--

F: --

P: --

Brazil Retail Sales MoM (Oct)

Brazil Retail Sales MoM (Oct)A:--

F: --

P: --

U.S. Weekly Continued Jobless Claims (SA)

U.S. Weekly Continued Jobless Claims (SA)A:--

F: --

U.S. Exports (Sept)A:--

F: --

P: --

U.S. Trade Balance (Sept)A:--

F: --

U.S. Weekly Initial Jobless Claims (SA)A:--

F: --

Canada Imports (SA) (Sept)

Canada Imports (SA) (Sept)A:--

F: --

U.S. Initial Jobless Claims 4-Week Avg. (SA)A:--

F: --

P: --

Canada Trade Balance (SA) (Sept)A:--

F: --

Canada Exports (SA) (Sept)A:--

F: --

U.S. Wholesale Sales MoM (SA) (Sept)A:--

F: --

U.S. EIA Weekly Natural Gas Stocks ChangeA:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)

China, Mainland M1 Money Supply YoY (Nov)--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)--

F: --

P: --

U.S. 30-Year Bond Auction Avg. YieldA:--

F: --

P: --

Argentina CPI MoM (Nov)

Argentina CPI MoM (Nov)--

F: --

P: --

Argentina National CPI YoY (Nov)--

F: --

P: --

Argentina 12-Month CPI (Nov)--

F: --

P: --

U.S. Weekly Treasuries Held by Foreign Central Banks--

F: --

P: --

Japan Industrial Output Final MoM (Oct)

Japan Industrial Output Final MoM (Oct)--

F: --

P: --

Japan Industrial Output Final YoY (Oct)--

F: --

P: --

U.K. Services Index MoM (SA) (Oct)--

F: --

P: --

U.K. Services Index YoY (Oct)--

F: --

P: --

Germany HICP Final YoY (Nov)

Germany HICP Final YoY (Nov)--

F: --

P: --

Germany HICP Final MoM (Nov)--

F: --

P: --

U.K. Trade Balance Non-EU (SA) (Oct)--

F: --

P: --

U.K. Trade Balance (Oct)--

F: --

P: --

U.K. Services Index MoM--

F: --

P: --

U.K. Construction Output MoM (SA) (Oct)--

F: --

P: --

U.K. Industrial Output YoY (Oct)--

F: --

P: --

U.K. Trade Balance (SA) (Oct)--

F: --

P: --

U.K. Trade Balance EU (SA) (Oct)--

F: --

P: --

U.K. Manufacturing Output YoY (Oct)--

F: --

P: --

U.K. GDP MoM (Oct)--

F: --

P: --

U.K. GDP YoY (SA) (Oct)--

F: --

P: --

U.K. Industrial Output MoM (Oct)--

F: --

P: --

U.K. Manufacturing Output MoM (Oct)--

F: --

P: --

U.K. Monthly GDP 3M/3M Change (Oct)--

F: --

P: --

Germany CPI Final MoM (Nov)--

F: --

P: --

Germany CPI Final YoY (Nov)--

F: --

P: --

U.K. Construction Output YoY (Oct)--

F: --

P: --

France HICP Final MoM (Nov)--

F: --

P: --

China, Mainland Outstanding Loans Growth YoY (Nov)--

F: --

P: --

U.K. Inflation Rate Expectations--

F: --

P: --

India CPI YoY (Nov)

India CPI YoY (Nov)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

The Fed cut rates and launched $40B in bill purchases to ease liquidity strain, though the move seems late and insufficient. Powell nears exit, funding pressures persist, and Oracle’s weak cloud results hit AI sentiment.

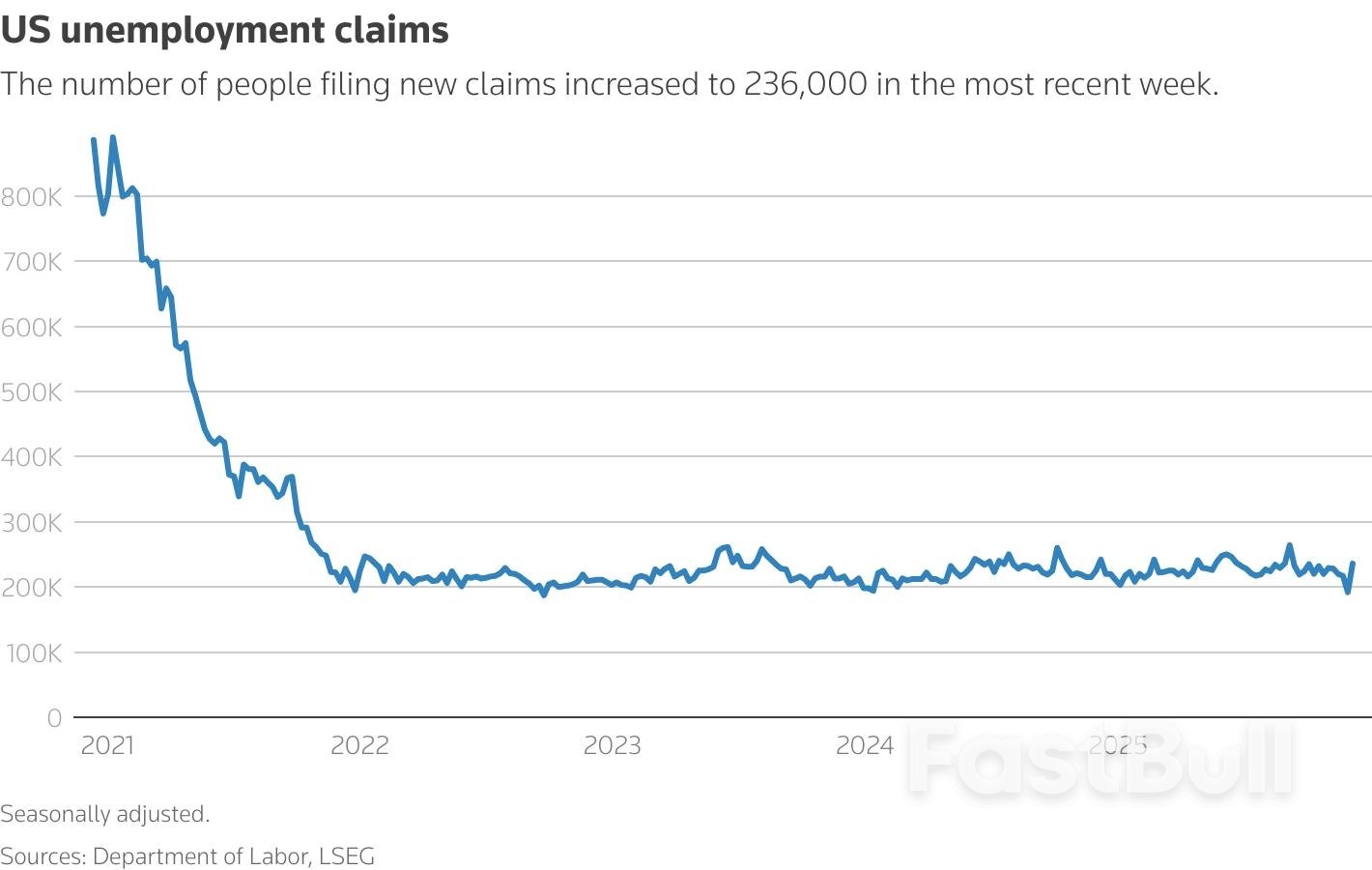

The number of Americans filing new applications for unemployment benefits increased by the most in nearly 4-1/2 years last week, but the surge likely does not suggest a material weakening in labor market conditions, as the claims data are volatile around this time of year.

The larger-than-expected rise in initial weekly jobless claims reported by the Labor Department on Thursday reversed the sharp drop in the prior week, which had pushed filings to a three-year low.

Economists said adjusting the data for seasonal fluctuations is always a challenge during the start of the holiday season, and recommended focusing on the four-week moving average to get a better read of the labor market. The four-week average of claims suggested labor market conditions remained stable.

"The bulk of this week-to-week volatility is seasonal noise," said Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets. "On an underlying basis, nothing has changed, but if anything, we would have to say that initial claims are running slightly below the long-established trend, one of several data points that refutes (Federal Reserve) Chairman (Jerome) Powell's characterization of a shaky labor market."

Initial claims for state unemployment benefits jumped 44,000, the biggest increase since mid-July of 2021, to a seasonally adjusted 236,000 for the week ended December 6, the Labor Department said. Economists polled by Reuters had forecast 220,000 claims for the latest week.

Claims had dropped to a three-year low in the prior week, which was partly attributed to difficulties adjusting the data around the Thanksgiving holiday. The four-week moving average of claims, which irons out seasonal fluctuations, rose 2,000 to 216,750 last week. Economists continue to describe the labor market as being in a "no-fire, no-hire" state despite a raft of layoff announcements by large corporations, including Amazon.

"It's a little surprising that recent layoff announcements haven't translated into a shift higher in initial claims," said Nancy Vanden Houten, lead U.S. economist at Oxford Economics.

"It may be that some workers who have lost their jobs have received generous severance packages or have found other employment, although that is more difficult in the current labor market with a depressed rate of hiring."

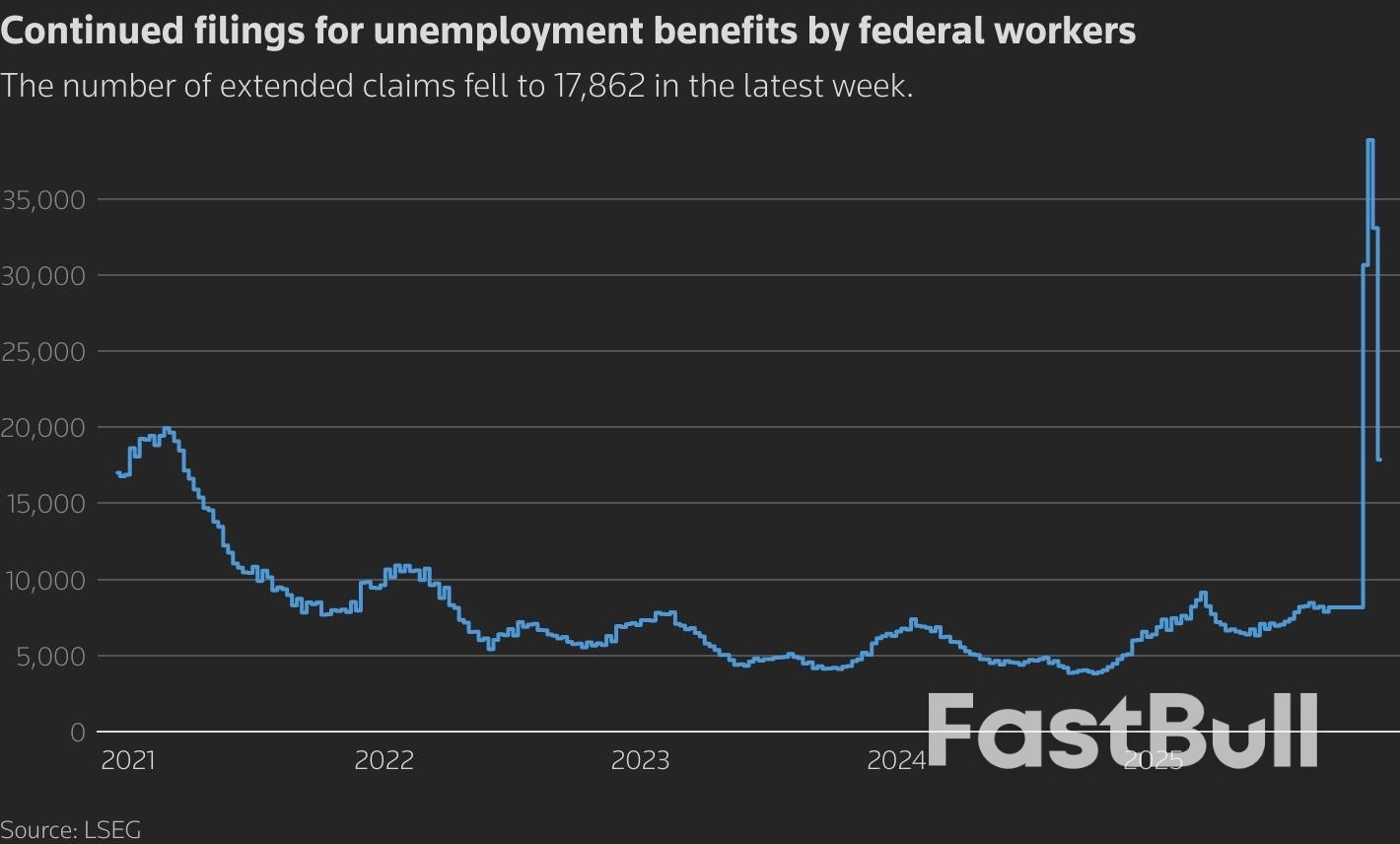

A line chart with the title 'Continued filings for unemployment benefits by federal workers'

A line chart with the title 'Continued filings for unemployment benefits by federal workers'The Fed on Wednesday cut its benchmark overnight interest rate by another 25 basis points to the 3.50%-3.75% range. The U.S. central bank has cut rates three times this year. Powell told reporters the labor market "seems to have significant downside risks," noting there was an overcounting of nonfarm payrolls, which policymakers believed was still persisting.

U.S. stocks were trading mostly lower. The dollar weakened against a basket of currencies. U.S. Treasury yields also fell.

In September, the Bureau of Labor Statistics estimated 911,000 fewer jobs were created in the 12 months through March than previously estimated, the equivalent of 76,000 fewer jobs per month. The BLS will publish the final payrolls benchmark revision in February along with January's employment report.

The employment report for November, delayed by the 43-day government shutdown, will be released next Tuesday. It will incorporate October's nonfarm payrolls data. The unemployment rate for October, however, will not be available because the shutdown prevented the collection of data for the household survey, from which the jobless rate is calculated.

The labor market has stagnated amid low supply and demand for workers, which economists blamed on reduced immigration and on import tariffs. The adoption of artificial intelligence for some job roles is also eroding demand for labor.

The number of people receiving unemployment benefits after an initial week of aid, a proxy for hiring, dropped 99,000 to a seasonally adjusted 1.838 million during the week ending November 29, the claims report showed.

Some of the decline in the so-called continuing claims could be the result of people exhausting their eligibility for benefits, limited to 26 weeks in most states. Continuing claims are consistent with a gradual rise in the unemployment rate.

A line chart with the title 'US unemployment claims'

A line chart with the title 'US unemployment claims'The unemployment rate increased to 4.4% in September from 4.3% in August. The Fed's new Summary of Economic Projections estimated the jobless rate would end this year at 4.5% and ease slightly to 4.4% in 2026, unchanged from the projections in September.

A separate report from the Commerce Department's Bureau of Economic Analysis and Census Bureau showed the trade deficit contracted 10.9% to $52.8 billion in September, the lowest level since June 2020, as goods exports soared and imports rose marginally. The smaller trade gap suggested trade likely contributed to gross domestic product in the third quarter.

Exports climbed 3.0% to $289.3 billion in September. Goods exports surged 4.9% to $187.6 billion, with shipments of consumer goods increasing to a record high. Imports rose 0.6% to $342.1 billion. Goods imports advanced 0.6% to $266.6 billion. But imports of automotive vehicles, parts and engines were the lowest since November 2022.

The goods trade deficit compressed 8.2% to $79.0 billion, the lowest level since September 2020.

The Atlanta Fed estimated GDP increased at a 3.5% annualized rate in the third quarter. The government will release its first estimate of third-quarter GDP on December 23, a delay prompted by the shutdown. The economy grew at a 3.8% pace in the April-June quarter.

In the latest wave of fearmongering surrounding President Trump's efforts to overhaul the U.S. Department of Education, a coalition of states that sued to stop mass layoffs at the department in March is now challenging recent decisions to transfer many of the DOE's core functions to the U.S. Department of Labor and other federal agencies.

The attorneys general from 20 blue states and the District of Columbia, along with several teachers' unions, argue in an amended complaint filed on Nov. 25 that federal laws require the U.S. Department of Education to implement its own programs. The lawsuits focus on the fact that the department signed seven agreements with four other federal agencies, allowing those agencies to handle the day-to-day management of key grant programs. Under these arrangements, the Labor Department now heads up most K-12 grant programs, distributing over $20 billion annually to schools.

The National Education Association issued a ridiculous statement alleging that the moves are "illegal, cruel, and shameful." NEA president Becky Pringle bizarrely declared, "Not only do they want to starve and steal from our students—they want to rob them of their futures. Nothing is more important than the success of our students, and America's educators and parents will not be silent as Trump and Linda McMahon turn their backs on our students, families, and communities to pay for billionaire tax cuts."

American Federation of Teachers President Randi Weingarten also claims that the move is not legal. "There are lots of things about the Department of Education that are in statute," she declares, referring to funds that the department distributes to low-income families, students with disabilities, English as a Second Language learners, and work-study programs.

Let's take a deep breath, step back, and look at the facts.

While the federal government has spent money on education and developed education policies since the 19th century, the DOE didn't become a standalone agency until 1980, when it split off from the U.S. Department of Health, Education, and Welfare. Its creation came about when, as a sop to the National Education Association, Jimmy Carter established it while running for reelection. Clearly, it was politically motivated, and in response, the NEA subsequently issued its first-ever endorsement in a presidential contest.

As Jay Greene, a senior research fellow at The Heritage Foundation, points out, most of the programs that the DOE now administers were created before the department was established. He writes that it is "just a bureaucratic restructuring. It doesn't get rid of programs; it doesn't cut funding; it doesn't close any schools. It's just a change in the administration, not a change in the programs and services and funding delivered to America's schools."

Neal McCluskey, director of the Cato Institute's Center for Educational Freedom, further explains that under the restructuring, states may get money back, but with strings attached.

Additionally, President Trump says his goal is to transfer the department's primary responsibilities—such as Pell Grants, Title I funding, and resources for students with disabilities—to other parts of the federal government.

There is little reason to believe that moving various programs to different agencies will have any impact on schools whatsoever. Running the same programs under a different department is unlikely to affect students.

"If that's all they're doing, they're not going to save any money, they're not going to change any policy," says Shep Melnick, a political scientist at Boston College.

Melnick is correct. Essentially, what the feds are trying to do at this time is tantamount to rearranging the deck chairs on the Titanic.

What the left and the teachers' unions truly fear is that the restructuring will eventually result in the federal government completely withdrawing all educational control.

The reasons for shutting it down are numerous.

First, spending is more efficient when it is closer to the source. Jim Blew, assistant secretary of education during the first Trump administration and co-founder of the Defense of Freedom Institute for Policy Studies, correctly notes, "This 'local control' message is often met by naysayers with the concern that some local districts may do worse without federal 'guardrails'—as if every school and district needs the same guardrails or that maintaining them comes with no cost. Perhaps some local districts will use their freedom to create worse outcomes (although that would be hard to do when roughly a third of our nation's 4th and 8th graders already cannot demonstrate even basic, grade-level reading or math skills), but I find it more likely that we will see committed, innovative educators improve student outcomes when freed to use federal funding as they think best."

Perhaps no one fully comprehends the DOE's uselessness and waste more than former Secretary of Education Betsy DeVos. She contends that it shuffles money around, imposes unnecessary requirements and political agendas through its grants, and then shirks responsibility for evaluating whether any of what it does actually adds value. "Here's how it works: Congress appropriates funding for education; last year, it totaled nearly $80 billion. The department's bureaucrats take in those billions, add strings and red tape, peel off a percentage to pay for themselves, and then send it down to state education agencies."

In summary, the DOE is ineffective, incompetent, unnecessary, and costly, and does nothing to support education. Its creation was a mistake, and it should be abolished. There is no strong policy reason or constitutional basis for the federal government to be involved in K-12 education. Ultimately, America's schools would be better off without it.

But big-government leftists and teachers' unions rely on centralized authority. It's easier for them to influence a single federal agency where they already hold sway than to compete for control across 50 states and thousands of local districts. And, sadly, they will get their way, as 60 U.S. Senators would have to authorize the abolition of the DOE, which will not happen.

President Donald Trump spoke with Prime Minister Narendra Modi as negotiators from the US and India work to resolve differences over an elusive trade agreement.

Modi on Thursday described the conversation as "warm and engaging" and said they "reviewed the progress in our bilateral relations and discussed regional and international developments."

"India and the U.S. will continue to work together for global peace, stability and prosperity," Modi posted on X.

An Indian official added that the two leaders underlined the importance of sustaining momentum in bilateral trade talks, and also discussed cooperation in critical technologies, defense, and security.

The White House did not immediately respond to a request for comment.

A pair of American delegations traveled to New Delhi this week in an effort to repair ties between the two countries that were damaged amid Trump's tariff push.

State Department official Allison Hooker was scheduled to meet with Indian diplomats including Foreign Secretary Vikram Misri. Separately, Deputy US Trade Representative Rick Switzer has been discussing a tariff framework with Indian negotiators.

The engagement has raised hopes of a rapprochement, especially around trade. Trump's punitive 50% tariffs have battered Indian industries and New Delhi is eager to secure relief and negotiations over the rate have dragged on for months. Indian officials have recently expressed optimism that an initial agreement to lower import taxes could be clinched by year's end, after the two sides failed to reach an understanding in the fall.

India's top economic adviser, V. Anantha Nageswaran, said in a Bloomberg Television interview that he would be surprised if a trade deal wasn't signed by March, saying most trade-related issues have been resolved.

"I was hoping something would be done by the end of November, but it has turned out to be elusive," Nageswaran said. "That's why it is difficult to give a timeline on this. However, I would be surprised if we don't have it sealed by the end of the financial year."

Trump has repeatedly signaled that he would lower the sky-high tariffs he imposed on Indian goods, which he enacted partially as a response to the country's purchases of Russian oil. But he has continued to send mixed messages about his views on India's trade practices.

Earlier this week, Trump suggested he might impose new tariffs on Indian rice to address alleged dumping. India is the world's largest rice exporter and the second-largest source of imports for the US. The Indian Rice Exporters Federation said in response that exports to the US remain demand-led, with major American producers not growing a similar crop to Indian basmati.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up