Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The EUR/USD pair rallied sharply to 1.1735 on Friday, propelled by a sustained sell-off in the US dollar. The move followed a widely anticipated Federal Reserve rate cut, which was accompanied by guidance that proved more accommodative than markets had expected.

The EUR/USD pair rallied sharply to 1.1735 on Friday, propelled by a sustained sell-off in the US dollar. The move followed a widely anticipated Federal Reserve rate cut, which was accompanied by guidance that proved more accommodative than markets had expected.

Chair Jerome Powell explicitly ruled out further rate hikes, and the Fed's updated "dot plot" projections now indicate only one additional cut for 2026 – a more measured path of easing than previously anticipated.

Adding to dollar weakness, the Fed announced it would begin purchasing short-term Treasury bills to bolster banking system liquidity – a measure that pushed Treasury yields lower. This was compounded by economic data showing initial jobless claims rose last week at their fastest pace in nearly four and a half years, reinforcing the case for a more supportive policy stance.

The broader external environment is turning increasingly unfavourable for the greenback. While the Fed signals a slower pace of easing, markets are concurrently pricing in a relatively tighter policy trajectory for central banks in Australia, Canada, and the Eurozone. This divergence has driven the dollar lower against most major currencies this week, with its most pronounced decline coming against the euro.

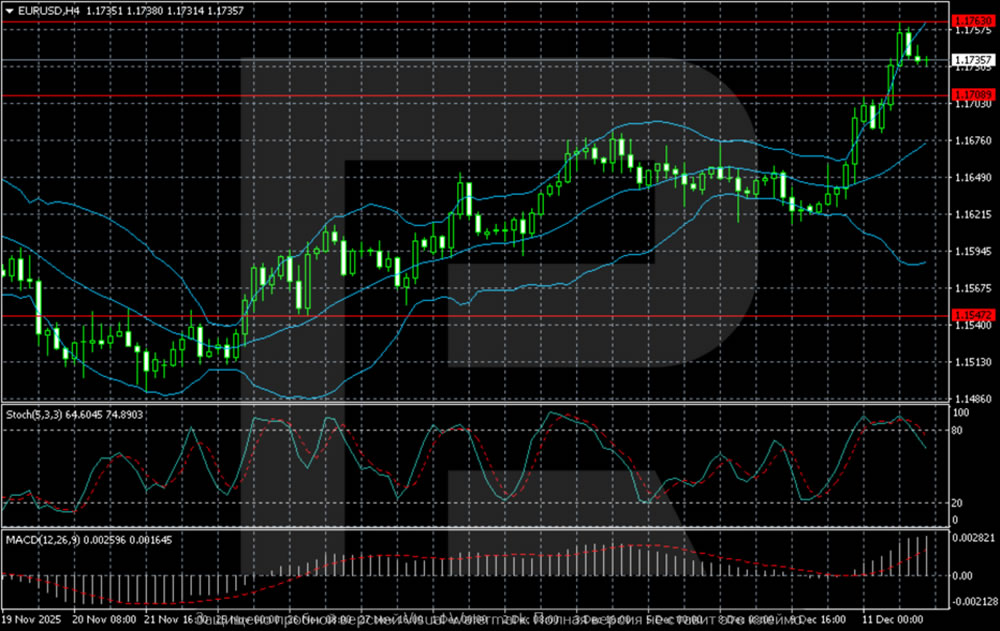

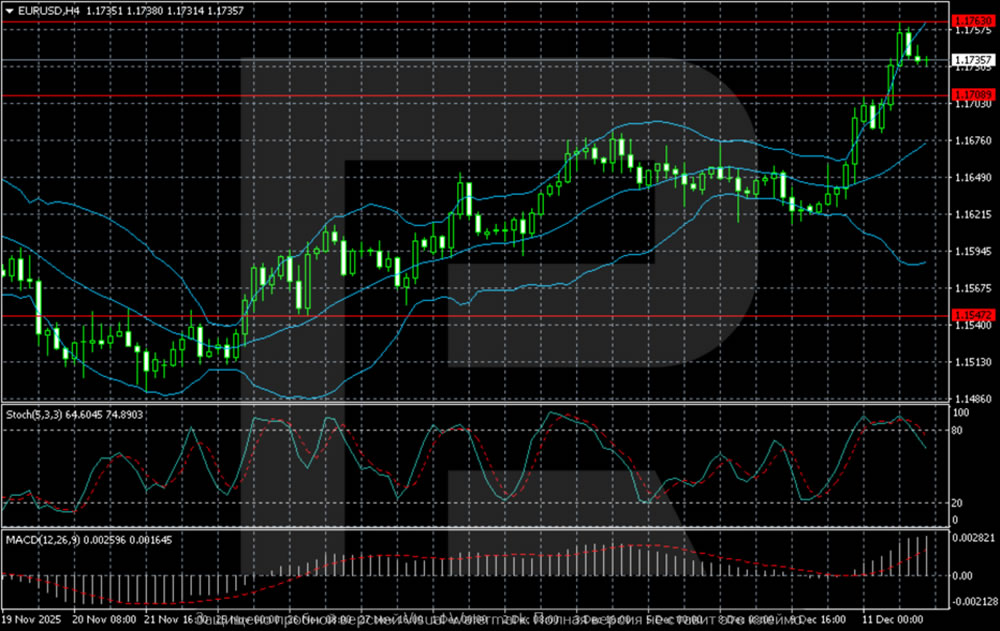

H4 Chart:

On the H4 chart, EUR/USD exhibits a robust bullish trend, trading near a key resistance zone at 1.1760–1.1780. The pair is holding firmly above the middle Bollinger Band, confirming buyer dominance. The upward slope and gradual widening of the upper band signal rising volatility and sustained momentum following a breakout to new highs.

Provided the price remains above the 1.1709 support, the market retains strong potential to challenge the 1.1780 ceiling. A decisive breakout and close above this zone would open a clear path towards 1.1850. Should a pullback materialise, the nearest significant support lies at 1.1650, the previous breakout point. A break below 1.1547 would be required to signal a deeper correction towards the lower Bollinger Band.

H1 Chart:

On the H1 chart, the pair is consolidating after a powerful impulse wave that targeted the 1.1760–1.1780 resistance area. The current correction is finding initial support at 1.1709, a level from which the latest acceleration originated.

The Stochastic oscillator is declining from overbought territory, increasing the probability of a near-term pause or shallow pullback. Nevertheless, the underlying structure remains bullish, with the price trading above the middle Bollinger Band, which now serves as dynamic support.

A confirmed breakout above 1.1780 would signal a continuation of the uptrend, with subsequent targets at 1.1820 and 1.1850. Conversely, a sustained move below 1.1709 would provide the first technical indication of fading bullish momentum, potentially triggering a correction towards the next demand zone in the 1.1650–1.1620 range.

EUR/USD has broken out decisively on the back of a dovish Fed pivot and a shifting global rate differential. The technical picture is firmly bullish, with the pair now testing a major resistance cluster near 1.1780. A successful breakout above this level would likely accelerate gains towards 1.1850. In the near term, the 1.1709 support is critical; holding above it keeps the immediate upward bias intact, while a break below would suggest a period of consolidation is needed before the next directional move.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

EURUSD 2026-2027 forecast: key market trends and future predictions

EURUSD 2026-2027 forecast: key market trends and future predictions Gold (XAUUSD) forecast 2026 and beyond: expert insights, price predictions, and analysis

Gold (XAUUSD) forecast 2026 and beyond: expert insights, price predictions, and analysis