Markets

News

Analysis

User

24/7

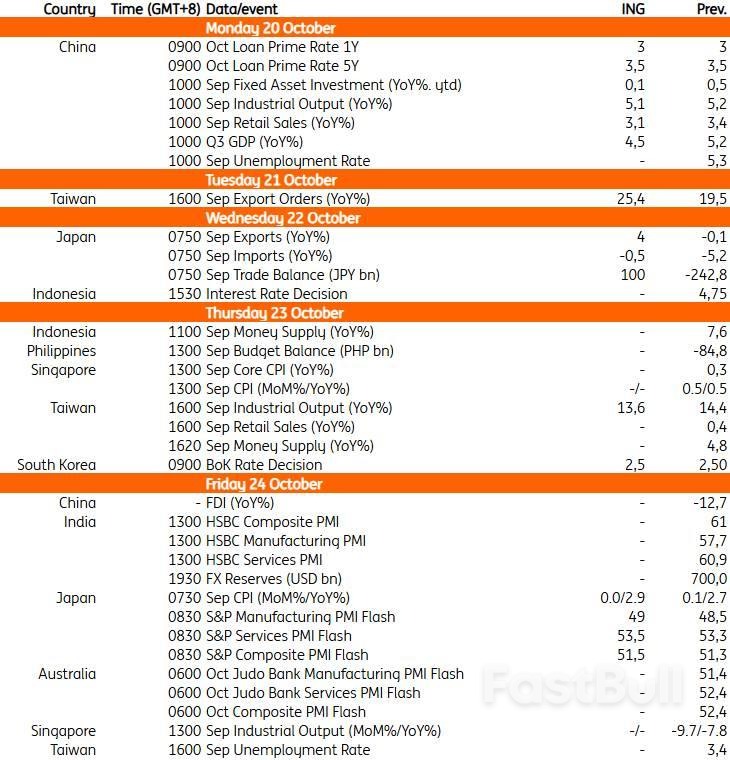

Economic Calendar

Education

Data

- Names

- Latest

- Prev

On Dec 29, 1989, the Nikkei 225 stock index reached an intraday high of 38,957.44 points, having grown sixfold during the decade.

On Dec 29, 1989, the Nikkei 225 stock index reached an intraday high of 38,957.44 points, having grown sixfold during the decade. That day marked the end of the Japanese bubble, which began in 1985 when the yen weakened to a record low of 260 against the US dollar in February, causing the September Plaza Accord to increase the rate “voluntarily”. The rapid appreciation of the yen to 123 by November 1988 saw a massive rise in real estate and stock market prices, when Japan reported GDP growth of 6.7% that year. In the Lost Decades after 1990, Japanese growth averaged around 1% per year, even as the population began to age and the stock market began to fall to a record low, to 7,695 points by February 2009, before recovering to its 1989 peak in December 2024.

The stock market was so weak that beginning in 2011, the Bank of Japan (BoJ) started buying Nikkei 225 exchange-traded funds, and owned as much as 75% of all Nikkei 225 ETFs issued by 2017. By 2021, it owned roughly 10% of the free float of Nikkei 225 stocks. Buying stock ETFs and massive Japanese government bonds (JGBs) was the Abenomics quantitative easing policy launched by the legendary BoJ governor Haruhiko Kuroda to revive the Japanese economy. The BoJ shifted the huge JGB portfolio out of the long-term pension funds to its books, causing the outflow of yen funds to earn higher US interest rates and dividends.

In September 2025, the BoJ announced the unwinding of its total ETF purchases by roughly US$2.5 billion annually, out of its book value holdings of ¥37.1 trillion (US$250.7 billion). The market value of the BoJ’s holdings is estimated at ¥85 trillion. So far, the looming sales have not affected Japanese stock prices. Why?

The broader trend of low yen exchange rates, low interest rates and slow and steady balance sheet reforms in the Japanese economy in the last two decades has caused a gradual return to greater productivity and revival. When the yen is on a downward trend, the carry trade, in which the borrower borrows yen to invest in US markets with higher interest rates, will earn positive carry, being a higher interest rate return and higher foreign exchange profits because the yen is expected to depreciate against the US dollar. The risk is that the yen suddenly appreciates, so hedge funds and speculative housewives who manage the bulk of Japanese household savings (the apocryphal Mrs Watanabe) are mainly responsible for taking such risks. Since Kuroda launched his unusual monetary policy, the yen has depreciated from a peak of 77.3 against the US dollar in January 2012 to 160 by July 2024, before higher inflation and interest rate hikes caused some appreciation back to the 145 to 150 range today.

During this period of a weak yen, Japanese holdings of long-term US Treasuries went from US$1.1 trillion at end-2012 to US$2.5 trillion at end-2024, according to US Treasury data. However, according to the Japanese Ministry of Finance’s net international investment position data, Japanese gross holdings of foreign portfolio investments grew from ¥308.1 trillion (US$4 trillion at an exchange rate of 76) to ¥693.9 trillion (US$4.4 trillion at an exchange rate of 157). If the dollar were to depreciate against the yen, Japanese holders of US dollars would start diversifying out of the greenback.

The size of Japanese flows into US dollar assets annually has been a significant factor in global liquidity and market prices. Japan alone held 13.5% of long-term US Treasuries in 2012, and even after the rise of Chinese holdings, the ratio at end-2024 was still 11%. Thus, if Japan were to reduce its holdings of US Treasuries or repatriate dollar holdings back to yen assets, the impact on the exchange rate and US financial assets would be significant.

The rise of the Japanese stock market reflects that portfolio rebalancing. If Japanese corporations and investors were to repatriate dollars to yen assets, what would they buy? The largest portion should be bonds, but bond prices are very high because of the current low interest rates. If inflation increases, at the current rate of 3% per annum, then bond prices would suffer capital depreciation. Land prices are still depressed except in key urban areas due to the ageing population and decline in birth rates. Thus, Japanese corporations have begun to buy back their own stock with their cash flow.

According to the latest available information, Japanese corporations bought back ¥14.9 trillion of their own stock in 2024, which was 1.7 times the previous year’s level. In the first half of 2025, they already bought back ¥9.4 trillion and may exceed ¥20 trillion for the full year of 2025. Thus, in addition to foreigners buying Japanese equity due to reasonable earnings valuation and the prospect of a stronger yen, it is the Japanese companies themselves that are driving up their own share prices.

Japanese companies have a reputation of being modest in their publicity of their achievements in reforms, mainly because of two decades of struggling with keeping jobs and improving their product quality and innovation. Nevertheless, foreign manufacturers appreciate that Japan has world-class research and development and high quality labour but ageing corporations, due to retiring owners/entrepreneurs. So, private equity firms have been buying up Japanese companies with good intellectual property rights and engineering skills. Japanese conglomerates have also begun to appreciate that instead of having a mixed group of subsidiaries under one umbrella, it would be more profitable to separately list their semiconductor or specialist engineering arms to get higher valuations.

With geopolitical tensions rising, Japan will increase its spending in defence and military technology, which will also drive the economy forward. Broadly speaking, we see a general rebalancing of global financial markets creating higher prospects for the Japanese stock market as the world needs to de-dollarise due to the growing and unsustainable US fiscal debt. The problem with forecasting the Japanese economy is that the yen has been far more volatile due to the carry trade that can swing the market up and down. One shrewd market observer thinks that at the end of year, the yen could be either 120 or 180 against the US dollar. So what you make on the stock market could be offset by the yen depreciation.

With the recent election of the first Japanese female Liberal Democratic Party leader Sanae Takaichi, the Nikkei 225 hit a record high of 48,000 points. The yield on the 30-year JGBs touched 3.333%, also an all-time high. Will prospectively the first female prime minister in the history of Japan undertake major reforms to revive its economy? That is the big question facing not just investors in Japan, but will have an impact on global financial markets in the days to come.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up