Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Mexico’s planned tariffs on Chinese goods add pressure as Beijing battles U.S. trade levies, testing China’s export resilience and 5% GDP growth goal.

Key Points:

China’s economy faces a pivotal test this quarter as tariff developments challenge the growth outlook. Recent economic indicators have raised concerns about Beijing achieving its 5% GDP growth target for 2025.The US and China extended the trade war truce in August, leaving Chinese goods exposed to US tariffs averaging 55%. In contrast, Beijing maintained the 10% levy on US shipments bound for China.

Avoiding a sweeping 145% US tariff on shipments to the US was critical. However, the US administration’s proxy trade war via third-country tariffs continues to gain momentum. Reports of Mexico’s plans to raise tariffs on Chinese goods signal another roadblock, challenging efforts to bypass US tariffs.Mexico has become a crucial hub for Chinese automakers targeting the US. BYD, Chery, and MG Motors have reportedly invested over $700 million in local plants. New tariffs on shipments to Mexico, coupled with existing US tariffs on Mexican exports, could dent demand for Chinese autos and parts.

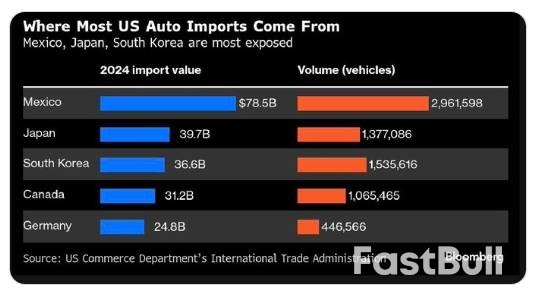

For context, Mexico accounted for the largest share of US auto imports, underscoring Mexico’s importance for auto manufacturers.

Bloomberg – US Auto Imports By Country

Bloomberg – US Auto Imports By CountryIn July, the US administration targeted another of China’s key trade routes, Southeast Asia. A 40% US levy on transshipments from Vietnam and a 19% tariff on Indonesian goods could affect Chinese exports. Chinese exports surged 7.2% year-on-year in July, up from 5.8% in June, with Southeast Asia driving growth. But August data will show whether fresh tariffs start to bite.

CN Wire commented on July’s trade data, stating:

“This export resilience persists despite high U.S. tariffs, indicating strong global demand continues to support China’s economy. […]. However, whether this momentum will last remains uncertain, as front-loading effects may fade.”Mexico’s tariff news follows reports of the US administration planning to impose rules of origin for indirect shipments.Natixis Asia Pacific Chief Economist Alicia Garcia Herrero commented on China’s outlook for terms of trade, stating:

“Rerouting will be much harder in the second half. So that’s going to hit Chinese exports indirectly. So, that’s why the second half is tougher and the government has been preparing.”The latest trade developments came as the US and China prepare for the next round of trade talks. China’s chief trade negotiator Li Chenggang plans to return to Washington to discuss trade terms. The outcome of trade talks could be crucial given China’s reliance on ‘third countries’ and tariffs targeting Chinese shipments.

On Wednesday, August 27, Mainland China’s CSI 300 and the Shanghai Composite Index pulled back 1.49% and 1.76%, respectively, after briefly reaching new year-to-date highs.Despite the retreat, optimism over Beijing’s 5% GDP growth target, supported by policy measures, continues to bolster demand for Mainland-listed stocks. The CSI 300 and the Shanghai Composite were up 1.19% and 0.58%, respectively, during the August 28 morning session.

Both indexes continue to outperform the Nasdaq Composite Index but trail the Hang Seng Index year-to-date. CSI 300 gained 9.4% in August and 12.7% YTD. Shanghai Composite rose 8.5% in August and 14.1% YTD. The Hang Seng leads, up 24.8% YTD, well ahead of the Nasdaq’s 11.8%Trade developments and Beijing’s next stimulus measures remain crucial to market momentum. An escalation in US-China trade tensions and delays in fresh stimulus could unravel the bullish sentiment.

CSI 300 – Nasdaq Composite Index – Daily Chart – 280825

CSI 300 – Nasdaq Composite Index – Daily Chart – 280825The next moves in US-China trade talks and Beijing’s stimulus drive will set the tone for markets in the coming weeks.However, crucial economic indicators will also affect market trends. August’s NBS private sector PMIs on Sunday, August 31 and September 1 will draw interest. The PMIs will reveal whether tariffs added more pressure on China’s manufacturing sector midway through Q3. Weak numbers could raise expectations of fresh stimulus from Beijing.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up