Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Japan Tankan Small Manufacturing Outlook Index (Q4)

Japan Tankan Small Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)A:--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)

U.K. Rightmove House Price Index YoY (Dec)A:--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)

China, Mainland Industrial Output YoY (YTD) (Nov)A:--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)A:--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)A:--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)A:--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)A:--

F: --

P: --

Canada Existing Home Sales MoM (Nov)

Canada Existing Home Sales MoM (Nov)A:--

F: --

P: --

Canada National Economic Confidence IndexA:--

F: --

P: --

Canada New Housing Starts (Nov)A:--

F: --

U.S. NY Fed Manufacturing Employment Index (Dec)

U.S. NY Fed Manufacturing Employment Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)A:--

F: --

P: --

Canada Core CPI YoY (Nov)A:--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)A:--

F: --

P: --

U.S. NY Fed Manufacturing Prices Received Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing New Orders Index (Dec)A:--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)A:--

F: --

P: --

Canada Core CPI MoM (Nov)A:--

F: --

P: --

Canada Trimmed CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)A:--

F: --

P: --

Canada CPI YoY (Nov)A:--

F: --

P: --

Canada CPI MoM (Nov)A:--

F: --

P: --

Canada CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)A:--

F: --

P: --

Canada CPI MoM (SA) (Nov)A:--

F: --

P: --

Federal Reserve Board Governor Milan delivered a speech U.S. NAHB Housing Market Index (Dec)--

F: --

P: --

Australia Composite PMI Prelim (Dec)

Australia Composite PMI Prelim (Dec)--

F: --

P: --

Australia Services PMI Prelim (Dec)--

F: --

P: --

Australia Manufacturing PMI Prelim (Dec)--

F: --

P: --

Japan Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. 3-Month ILO Employment Change (Oct)--

F: --

P: --

U.K. Unemployment Claimant Count (Nov)--

F: --

P: --

U.K. Unemployment Rate (Nov)--

F: --

P: --

U.K. 3-Month ILO Unemployment Rate (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Including Bonuses) YoY (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Excluding Bonuses) YoY (Oct)--

F: --

P: --

France Services PMI Prelim (Dec)

France Services PMI Prelim (Dec)--

F: --

P: --

France Composite PMI Prelim (SA) (Dec)--

F: --

P: --

France Manufacturing PMI Prelim (Dec)--

F: --

P: --

Germany Services PMI Prelim (SA) (Dec)

Germany Services PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Services PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. Services PMI Prelim (Dec)--

F: --

P: --

U.K. Manufacturing PMI Prelim (Dec)--

F: --

P: --

U.K. Composite PMI Prelim (Dec)--

F: --

P: --

Euro Zone ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Germany ZEW Current Conditions Index (Dec)--

F: --

P: --

Germany ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (Not SA) (Oct)--

F: --

P: --

Euro Zone ZEW Current Conditions Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (SA) (Oct)--

F: --

P: --

U.S. Retail Sales MoM (Excl. Automobile) (SA) (Oct)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Bank of Korea Gov. Rhee Chang-yong speaks in this Feb. 18 photo. The Korean central bank is widely expected to lower its policy rate by 0.25 percentage point next week in an effort to prop up the economy, a poll showed Friday.

Bank of Korea Gov. Rhee Chang-yong speaks in this Feb. 18 photo.

The Korean central bank is widely expected to lower its policy rate by 0.25 percentage point next week in an effort to prop up the economy, a poll showed Friday.

According to a survey conducted by Yonhap Infomax, the financial news arm of Yonhap News Agency, 20 out of 21 local analysts and experts polled predicted the Bank of Korea (BOK) will cut its base rate to 2.75 percent from the current 3 percent at its next rate-setting meeting slated for Tuesday.

In January, the BOK kept its benchmark interest rate frozen in the wake of the weak local currency amid political chaos and uncertainties stemming from U.S. President Donald Trump's new administration.

The on-hold decision came on the heels of two rate cuts in the October and November meetings.

"The country is facing growing downside risks centering on weak domestic demand, while the won's further weakness seems limited, which would lead the BOK to lower the policy rate by 25 basis points," said Kim Seon-tae, an expert from KB Kookmin Bank.

Nineteen out of the 21 analysts polled anticipated the key rate to be lowered to 2.5 percent in the first half of this year.

The central bank is scheduled to present an adjusted growth forecast Tuesday. BOK Gov. Rhee Chang-yong has hinted at slashing the outlook to around 1.6 percent from its previous forecast of a 1.9 percent expansion.

Korea's potential growth rate is at 2 percent, and this year may mark the first time ever that the country's yearly growth rate falls below the level.

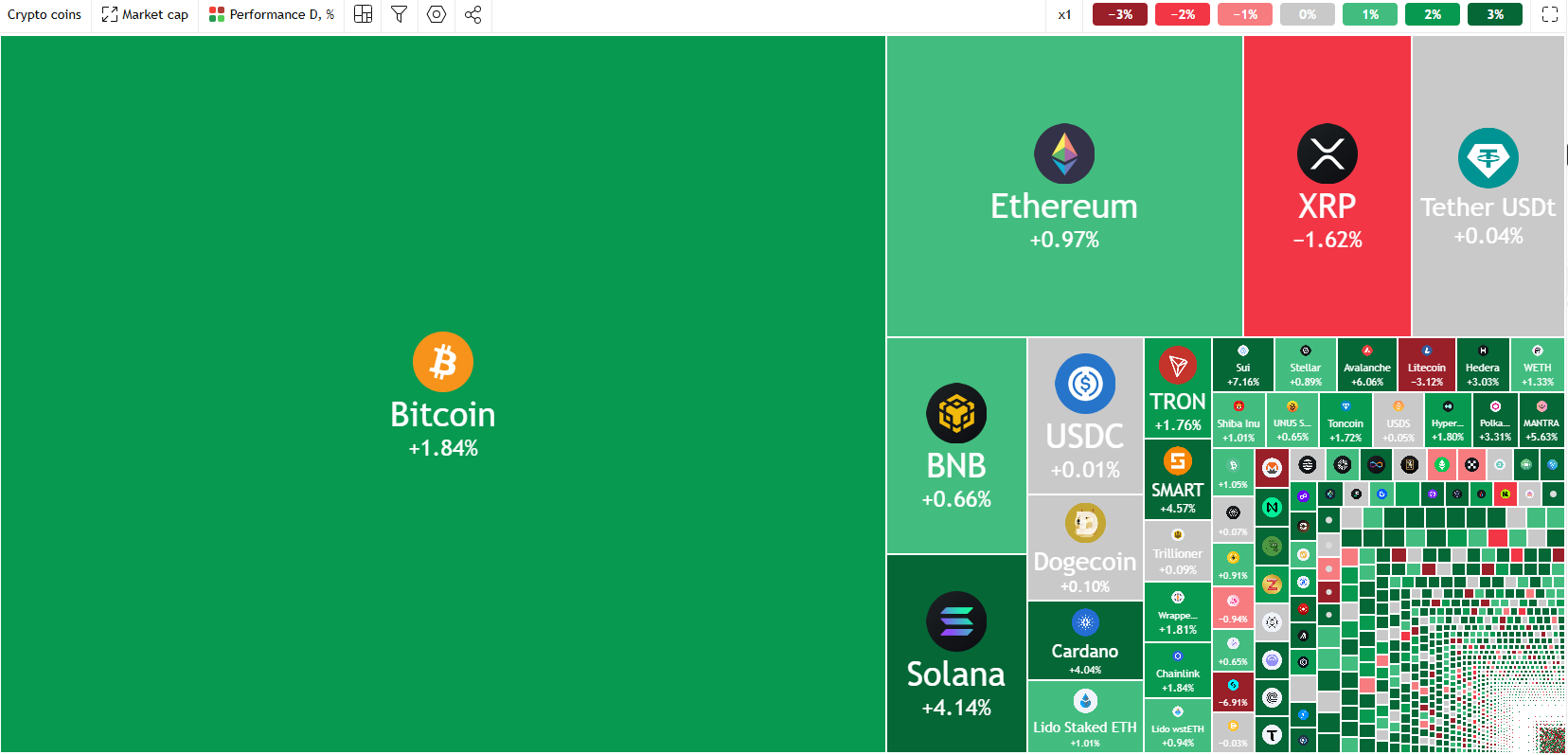

Bitcoin (BTC/USD) is holding above $95k but facing significant resistance.

While spot Bitcoin ETFs have attracted substantial investments, there have been recent net outflows, and on-chain data suggests a cooling down in speculative appetite.

Strategy’s potential Bitcoin purchase, following a $2 billion fundraising, could be a catalyst for a future bull run.

Bitcoin has regained momentum after finding support at the key $95k level this week before rising to trade at 98357 at the time of writing. The recent consolidation suggests that Bitcoin could be ready for its next big rally, with a move higher looking appealing once more.

Crypto Heatmap, February 20, 2025

Source: TradingView (click to enlarge)

ETF Flows

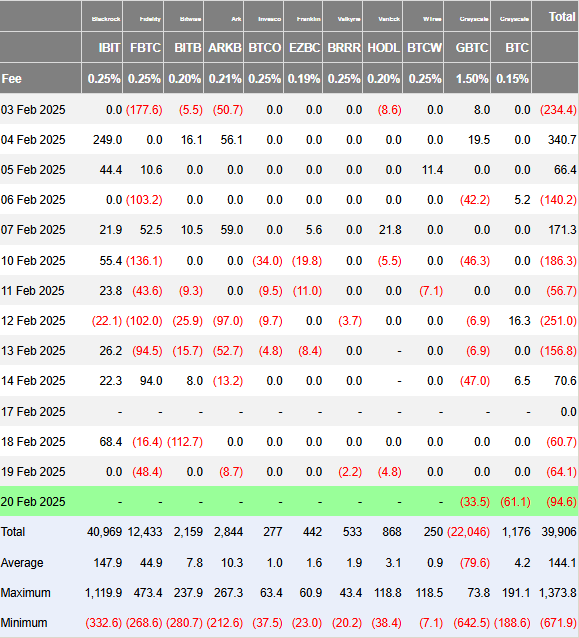

Even though Bitcoin’s price fell from its all-time high on January 20, data from CoinShares shows that spot ETFs tied to Bitcoin have still attracted a huge $5.6 billion in new investments.

However, over the last few days we have seen a consistent amount of net outflows with figures of 60.7, 64.1 and 94.6 million USD in net outflows since Tuesday.

Source: Farside Investors

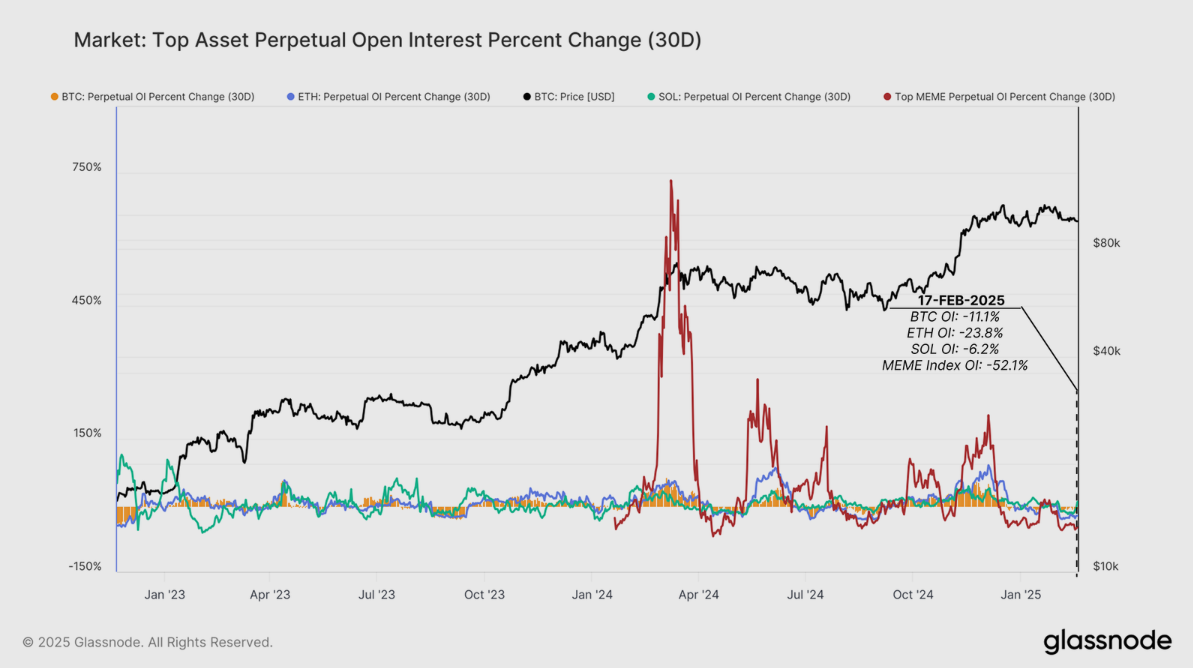

The Week on Chain – Glassnode Data Reveals Downside Risks

Money flowing into the market is slowing down, and trading in derivatives is dropping. The way short-term investors are buying now looks similar to May 2021, which was a tough time for the market.

Overall, in recent weeks markets are seeing the momentum of capital inflows has declined for all digital assets. This signals a meaningful cooling down in speculative appetite and alludes to a potential for capital rotation out of riskier assets on the road ahead.

This is in line with the overall market sentiment at the moment.Although US stock markets continue to hold near highs, the rise of Gold is a clear sign that markets remain nervous as haven demand continues to propel the precious metal to fresh highs.

Momentum in spot markets is slowing down, and less money is going into perpetual futures. This drop in demand has caused a big decline in open interest across major assets, showing less speculative trading and lower profits from cash-and-carry strategies.

The drop in open interest shows that traders are cutting back on risky leveraged bets, likely because the market feels weaker and less certain. The biggest decline is in Memecoins, which usually attract short-term traders but quickly lose popularity when confidence fades.

Source: Glassnode

Microstrategy or ‘Strategy’ Gearing Up for Fresh Buys?

MicroStrategy or as we should get used to calling them, Strategy didn’t buy any Bitcoin last week, keeping its total at 478,740 BTC for the second time.

However, MicroStrategy has hinted at a new Bitcoin purchase with its recent fundraising effort. On February 20, the company announced it had successfully priced a $2 billion offering of 0% convertible notes due in 2030. The deal, set to close on February 21, also gives buyers the option to purchase an extra $300 million in notes.

Will such a purchase prove to be the catalyst for another bull run?

Technical Analysis BTC/USD

Bitcoin (BTC/USD) from a technical standpoint on the daily timeframe sees price eyeing a breakout following a period of consolidation.

The consolidation between 94000 and 100000 has lasted for the last two weeks with Tuesday seeing price dip to a low of 93340 before reclaiming the 95000 handle.

Thursday daily candle did close back above the 100-day MA resting at 97899 but there are significant hurdles ahead. The 50-day MA rests at 99059, just shy of the psychological 100000 level.

Bitcoin (BTC/USD) Daily Chart, February 20, 2024

Source: TradingView.com (click to enlarge)

Dropping down to a two-hour chart and there may be scope for a short term pullback. Significant support rests below current price as we have the 50,100 and 200-day MA converging between the 96000-97000 handles.

This makes this a key area of confluence which could serve as a base for a move toward the 100000 psychological level and beyond.

Immeidate support rests at 97000 before the key 95000 handle comes back into focus.

Resistance rests at 99059 and 100000 before markets will turn their attention toward the 102157 resistance handle.

Bitcoin (BTC/USD) Two-Hour (H2) Chart, February 20, 2024

Support

97000

95000

93200

Resistance

99059

100000

102157

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up