Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Forex currencies have been dormant since the beginning of August as Markets haven’t found what they want in the latest key data reports.

Forex currencies have been dormant since the beginning of August as Markets haven’t found what they want in the latest key data reports.

As previously thought, the latest NFP, PPI, and CPI combo reports would have expected to relieve volatility in FX. But volatility there wasn’t.

After receiving all the most influential market data, the next step will be next Wednesday’s FOMC rate decision (September 17).

Prior to the CPI release, expectations for a 50 bps cut were priced at 10% and are now closer to 5%. The 25 bps cut, however, is still priced to be a sure thing.

Indeed, when looking at Market reactions in other assets, it seems that the theme that is developing is one of a less prolonged impact of tariffs.

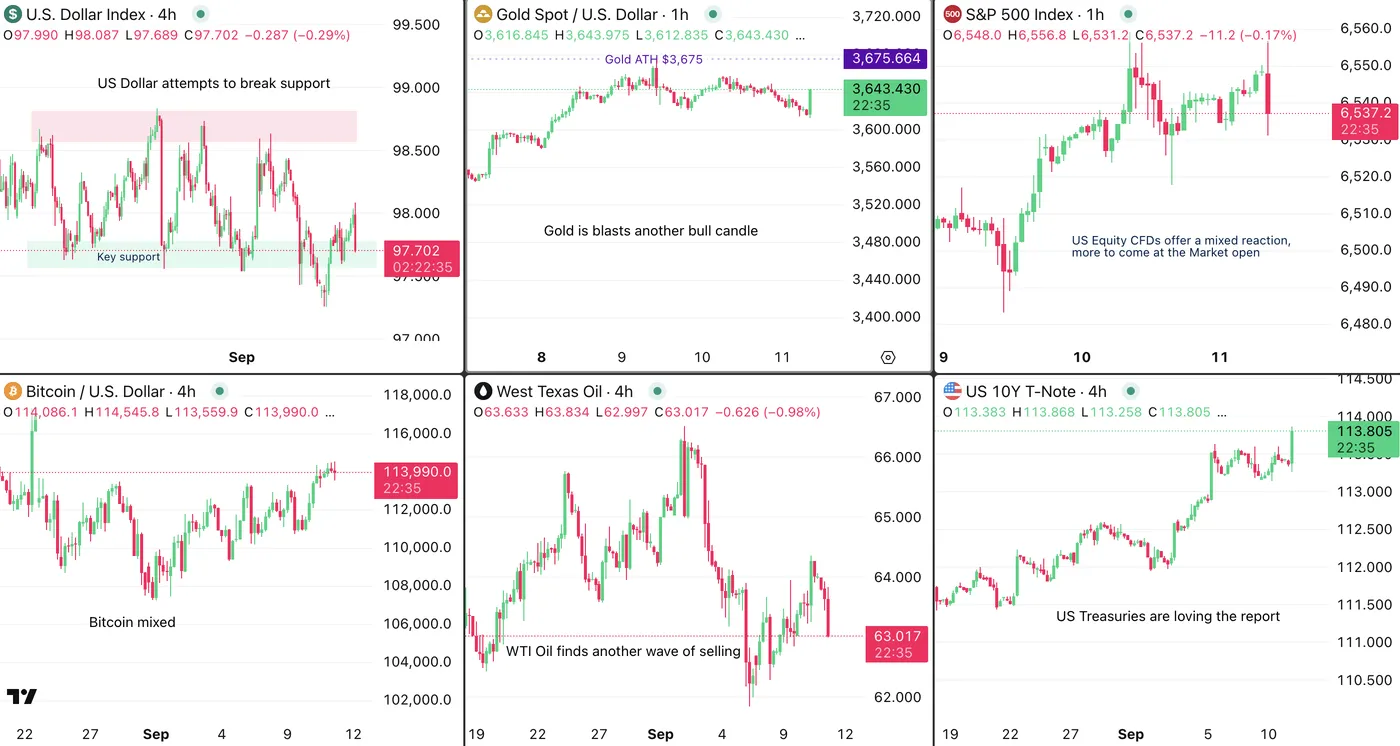

Despite an as expected 0.3% report, participants bidding on Bonds and Gold point toward a repricing of lower long-run inflationary impact of tariffs (while they are just starting to bite now), which is flattening the US Yield curve.

Until now, pricing has been one of lower short-term inflation expectations versus higher ones in the long run.

Despite the immediate US Dollar selloff, FX currencies are hesitant and hang close to unchanged on the session.

Discover major currency pairs charts and levels, after first peaking at reactions to other asset classes.

An overlook at cross-assets market reactions: Bonds and Gold are loving it, USD corrects.

The most volatile FX pair is enjoying the ongoing selloff in the US Dollar but has yet to break out of its mid-range pivot zone.

Some ongoing selling might be pushing prices out of this region however this move still has to develop.

Wicky action at the extremes prove that participants are still hesitant on the upcoming direction for currencies.

A 25 bps confirming could still provide some strength to the USD which helps to explain why participants are still looking at each other to see who moves first

Levels to watch for USDJPY:

AUDUSD has rebounded significantly since its August 1st lows and by evolving in an intermediate upward channel, heads to retest its yesterday and 2025 highs (0.6535).

Some hesitation at the current levels is forming and will be essential to monitor.

Levels to watch for AUDUSD:

EURUSD still evolves within its August range after a failed upside breakout in yesterday’s session.

Buyers have pushed towards a retest of the resistance but seem to be running out of steam.

Levels to watch for EURUSD:

USDCHF 2H Chart, September 11, 2025, Source: TradingView

The Swiss franc had strengthened immensely in the beginning of the month which pushed USDCHF towards a retest of its 2025 Main support (0.7916 week lows).

However, despite a selling candle from the data, hesitation comes at the 50-period MA which will also be key to upcoming action: A rejection of the MA could provide a boost to the pair, while a breakdown could also lead to further downside.

Levels to watch for USDCHF:

GBPUSD has, like its European neighbor, been stuck in a 2,000 pip range since the middle of August (1.34 to 1.36).

The buying reaction to the CPI report is once again met with some hesitation as prices are meeting the range resistance.

Watch the immediate low-slope downward channel that may shape today’s price action.

Levels to watch for GBPUSD:

USDCAD is virtually unchanged after the report – By attaining the upper bound of its upward channel, mean-reversion selling seems to occur but real momentum has yet to materialize.

Levels to watch for USDCAD:

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Natural Gas (NG) Price Chart

Natural Gas (NG) Price Chart WTI Price Chart

WTI Price Chart Brent Price Chart

Brent Price Chart