Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

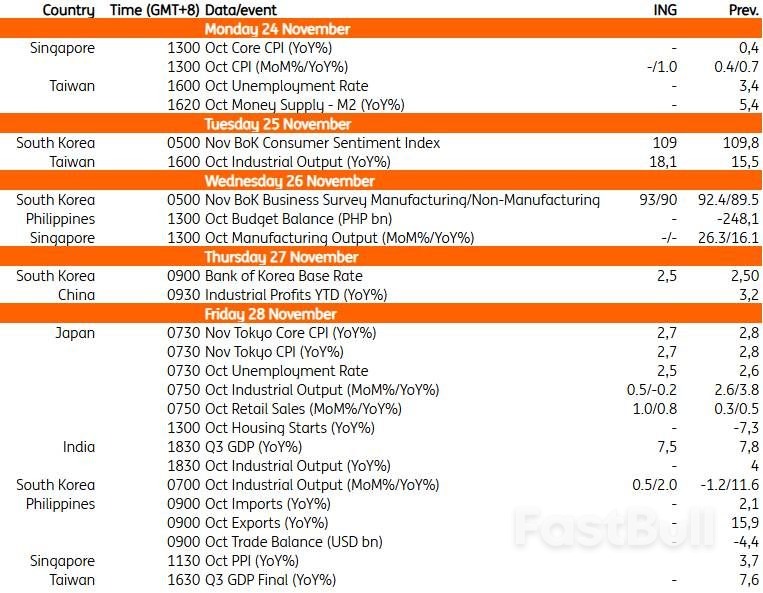

South Korea: BOK to stand pat, while industrial production continues growing The Bank of Korea will likely keep the policy rate

The Bank of Korea will likely keep the policy rate at 2.50% on Thursday for another month, with a minor dissent vote expected. The Bank of Korea is likely to prioritise concerns about financial instability over inflation. Given no clear signs that housing prices have settled and the FX market remains volatile, the BoK has reason to keep rates unchanged. Also Thursday, the BoK releases its outlook report. Amid easing trade tensions and a stronger-than-anticipated semiconductor cycle, we believe the BoK will revise up its 2025 GDP forecast to 1.1% from 0.8% and its 2026 forecast to 1.9% from 1.6%. A GDP outlook below 2% is likely to support the BoK's continued easing policy stance. The recent hike in KTB yields reflected Governor Rhee's hawkish remarks - signalling a possible change of policy direction - during an earlier media interview. We think his remarks at press conference should be more balanced and highlight that policy decisions are data-dependent.

Industrial production is forecasted to increase for a second consecutive month, driven by strong chip output. The longer-than-expected Chuseok holiday, combined with the 2nd cash payout program, should boost service activity.

China's industrial profits data, out Thursday, will round out the month's data releases. The data has been showing signs of improvement in the past few months, with profits so far up 3.2% YoY, year-to-date, through September, thanks to two straight months of YoY profit growth above 20% in August and September. This was boosted by a supportive base effect. Support from this effect should gradually wane in the 4Q data, but be enough to keep profit growth solidly positive in October. The industries that have been seeing strong export demand such as rail, ships, and aerospace, computers, communication, other electronic equipment manufacturing, and electrical machinery & equipment manufacturing have generally been outperformers so far this year. This trend should continue.

Tokyo's consumer price index inflation is expected to rise 2.7% YoY in November, supported by solid wage gains. The weaker JPY probably added upward pressure. Industrial production will likely remain positive following Japan's trade agreement with the US. Despite a contraction in the third quarter, recent data suggest an economic recovery, supporting the Bank of Japan's continued policy normalisation. Market expectations for a December rate hike have fallen sharply over the week. We believe that recent BoJ comments indicate at least three board members support a more hawkish stance. However, it remains unclear if others will agree. We continue to forecast a rate hike in December, though the likelihood of a delay to January is rising.

We expect Taiwan's industrial production data, out Tuesday, to continue its streak of strong growth, accelerating slightly to 18.1% YoY. Strength has been quite heavily concentrated in the Information & Electronic Industries and remains vulnerable to a downturn if demand in this sector slows. While market debate on this possibility has increased recently, we do not yet see it affecting the October data.

We expect India's GDP growth in the third quarter to slow down modestly to 7.5% YoY. Export growth began to slow in 3Q due to the impact of 50% tariffs on US exports. But private consumption growth remained relatively strong, driven by GST rate cuts and the consequent boost in consumer goods purchases.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up