- WTI

- XAUUSD

- XAGUSD

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

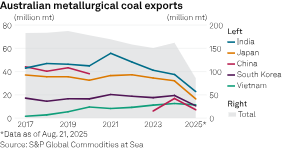

Australian metallurgical coal producers expect higher exports to India but are facing increasing competition from the US and Russia, according to S&P Global Commodities at Sea data.

Australian metallurgical coal producers expect higher exports to India but are facing increasing competition from the US and Russia, according to S&P Global Commodities at Sea data.BHP Group Ltd., Whitehaven Coal Ltd. and Yancoal Australia Ltd. outlined increased met coal production in fiscal 2025 while talking up India's demand growth, which could help arrest declining average realized prices. Platts assessed the premium hard coking coal Australia export FOB East Coast price at $187.50/mt on Aug. 22, down from $200.50/mt a year prior.

While Japan accounts for about half of Whitehaven's total volume, "India has actually emerged with 11% now, which is good because that footprint we know will expand considerably as we go forward," Paul Flynn, managing director and CEO, said Aug. 21 during a fiscal 2025 call with analysts.In fiscal 2025, India shot up to become Whitehaven's second-largest export destination with A$795 million in revenue — all of it met coal — behind Japan's A$2.73 billion, according to the miner's annual report.

"Structurally, India is very dependent on the seaborne market for met coal. It has next to nothing in terms of its own resource ... and Australia is already the largest supplier to India of its metallurgical coal demand," Flynn said during a same-day media call."With the growth in blast furnace construction capacity in [India], we can see an outlook for growth in metallurgical coal demand that's very strong; and we see limited opportunities in the pipeline for new supply to come on, hence our view that prices will continue to tighten and you'll see better pricing emerge as a result," Flynn added.

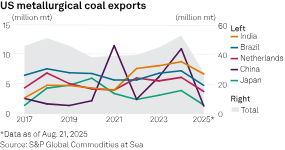

While Australia's total met coal exports rose annually in 2024, the downtrend in exports to India that started in 2021 persisted, according to CAS data. In 2024, exports to India comprised 37.5 million mt of Australia's total of 161.9 million mt.China's return to procuring Australian coal, after banning coal from Down Under in 2020, is partly responsible for Australia's falling exports to India in recent years, said Pranay Shukla, head of dry bulk freight and commodities research at Commodity Insights, in an interview. India diversifying met coal supplies, including from the US, is also a factor, Shukla added.

India's met coal imports from the US steadily increased after 2021, hitting a record 8.8 million mt in 2024, second only to China's 11 million mt. India is already the lead destination for US met coal this year with 6.7 million mt as of Aug. 21, ahead of Brazil's 4.8 million mt and the Netherlands' 3.7 million mt. China stood at 1.4 million mt amid trade tensions with the US.The US, whose coal industry is now aided by an accommodative president, was India's third-highest met coal source behind Australia and Russia in 2024. Russia's exports to the subcontinent have also risen since 2021.

A slowdown in China's property sector lowered demand and cut met coal prices across product categories in fiscal 2025, and "India's demand has also been tempered by the early onset of the monsoon season along with higher levels of domestic production," Yancoal said Aug. 19 in its half-year report.However, "the Indian growth opportunity is real," Mark Salem, Yancoal's executive general manager of marketing, said on an analyst call Aug. 20.

"The advantage of the Indian market is that India does not produce its own metallurgical coal, unlike China. Therefore, based on their GDP growth assumptions and this demand profile based on their infrastructure plans, they will need the coking coal to meet that growth requirement," Salem said.BHP CEO Mike Henry also highlighted India as "a bright spot for commodity demand" during an Aug. 19 fiscal 2025 results call.

"Indian pig iron production growth remained strong" during fiscal 2025, and "robust hard coking coal imports from developing countries such as India will lead to growing and resilient demand for decades to come," BHP said in its results."India will likely remain the fastest-growing major economy, driven by sustained public investment, improving monetary conditions and resilient service sector activity," BHP said.

However, Henry noted on the call that BHP had underestimated the resilience of steel demand in China, whose production is believed to have peaked in 2020.BHP has seen "robust commodity demand in China from the continued strong growth there, including from the infrastructure and electrification sectors, even as demand from the property sector remains subdued," Henry added.

Flynn also pointed to Chinese policy being "focused on constraint of surplus production of coal and of course, surplus steel production."Whitehaven's coal exports to China surged by over 957% to A$571 million in fiscal 2025 — all metallurgical — to become the miner's third-highest export destination after not even making its top 10 in fiscal 2024.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up