News

Analysis

7x24

Quotes

Economic Calendar

Video

Data

- Names

- Latest

- Prev

Trending Topics

To quickly learn market dynamics and follow market focuses in 15 min.

In the world of mankind, there will not be a statement without any position, nor a remark without any purpose.

Inflation, exchange rates, and the economy shape the policy decisions of central banks; the attitudes and words of central bank officials also influence the actions of market traders.

Money makes the world go round and currency is a permanent commodity. The forex market is full of surprises and expectations.

Latest Update

How to Make Forecasts with Pre-trained Machine Learning Models?

Curious about my trading success with a self-trained Decision Tree model on US stocks? Stay tuned for valuable insights and a test script of the strategy for your reference!

Full Course: Optimize Parameters for Machine Learning Model that Gives a Sharpe Ratio 5% +

Today, we delve into how to optimize machine learning model parameters to triple your invested capital and achieve an impressive Sharpe ratio of 5%+ in just 350 trades.

Full Course: Begin Mining in 10 Minutes

Think you need a super-powered computer to mine crypto? Not at all! Your trusty home computer can do the job just fine. I'll show you how to start mining from the comfort of your own home.

Full Course: How to Auto-Generate Triangle Patterns

Triangle patterns serve as crucial reference signals within the realm of trading, and today I am thrilled to unveil a remarkably efficient tool that expedites the detection of trading signals.

View All

No data

Latest Update

How to Make Forecasts with Pre-trained Machine Learning Models?

Curious about my trading success with a self-trained Decision Tree model on US stocks? Stay tuned for valuable insights and a test script of the strategy for your reference!

Full Course: Optimize Parameters for Machine Learning Model that Gives a Sharpe Ratio 5% +

Today, we delve into how to optimize machine learning model parameters to triple your invested capital and achieve an impressive Sharpe ratio of 5%+ in just 350 trades.

Full Course: Begin Mining in 10 Minutes

Think you need a super-powered computer to mine crypto? Not at all! Your trusty home computer can do the job just fine. I'll show you how to start mining from the comfort of your own home.

Full Course: How to Auto-Generate Triangle Patterns

Triangle patterns serve as crucial reference signals within the realm of trading, and today I am thrilled to unveil a remarkably efficient tool that expedites the detection of trading signals.

The resurgence of the pandemic as well as the supply chain crisis continue to slow the pace of global economic expansion. All factors - the uneven development of the world's economies, the slowdown of the euro area economy, inflation and labour indicators falling short of expectations - have mounted headwinds on the euro.

Due to growing supply chain bottlenecks caused by Covid-19, the expansion of world economic activity has shown a clear weakness, and economic recovery dragged by the relaxation of covid controls in various countries halted. Economic growth still be a task of primary importance in European market under the shadow of the pandemic. Hence, what does the euro-zone economy head to at this point and what will it do to the euro?

Traumatized by pandemic and supply chain bottlenecks, world economy is developing unevenly, with the pace of recovery in developed countries significantly higher than in developing countries, while supply chain bottlenecks remain an urgent worldwide problem to be solved.

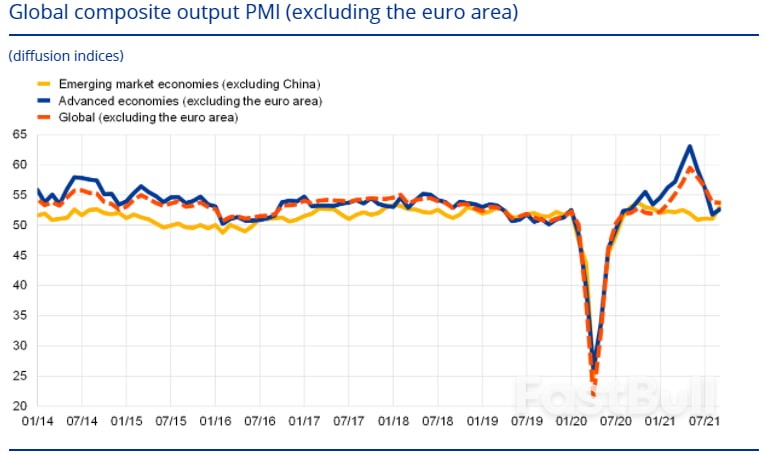

The global composite output Purchasing Managers’ Index (PMI) – excluding the euro area –confirmed that growth momentum moderated in the third quarter of 2021, although it remained well above its historical average. Specifically, industrial production momentum continued to soften in advanced economies in July. Growth momentum in emerging market economies remained softer than in advanced economies, especially in the manufacturing sector.

At the same time, new data from the World Trade Organization (WTO) point to a steady increase in commercial services trade in the second quarter, although it remains 20 percentage points below its pre-pandemic level. Most governments have eased covid restrictions, while later an uncertain growth on trade and a restrained economy occur, which may be blamed for the supply crisis and rising energy prices.

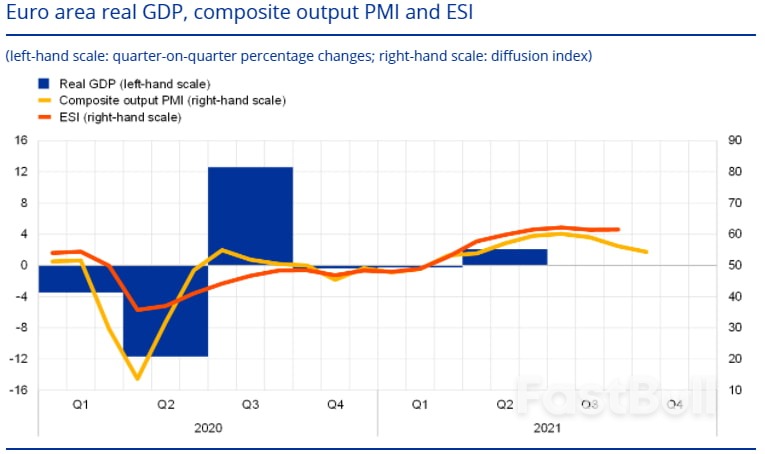

Benefit from the exit of covid controls by European governments and spurring by higher vaccination rates, the EU has seen a strong rebound on the service, such as tourism, as evidenced by a 2.1% of quarterly GDP growth in Q2 and a recovery trend in Q3. However, European GDP growth remains below pre-pandemic levels, when manufacturing production continues to be constrained by the shortage of materials, equipment, labour and rising transportation costs and energy prices.

According to the most recent monthly data from the European Central Bank, euro-area GDP continued to be strong in the third quarter but gradually trended downward from the fourth quarter. Industrial production fell by 1.6%. The more timely composite output Purchasing Managers’ Index (PMI) rose to 58.4 in Q3 of 2021, up from 56.8 in Q2, reflecting falling manufacturing output (to 58.6) and rising activity in services (to 58.4). However, in October the PMI declined further, reaching 54.3, suggesting Manufacturing supply bottlenecks intensified and stocks of purchases reached a record high level.

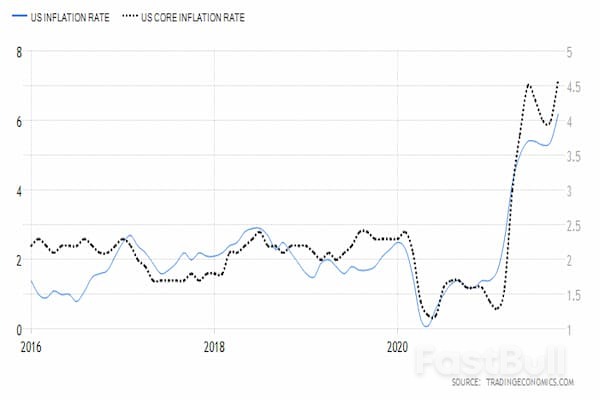

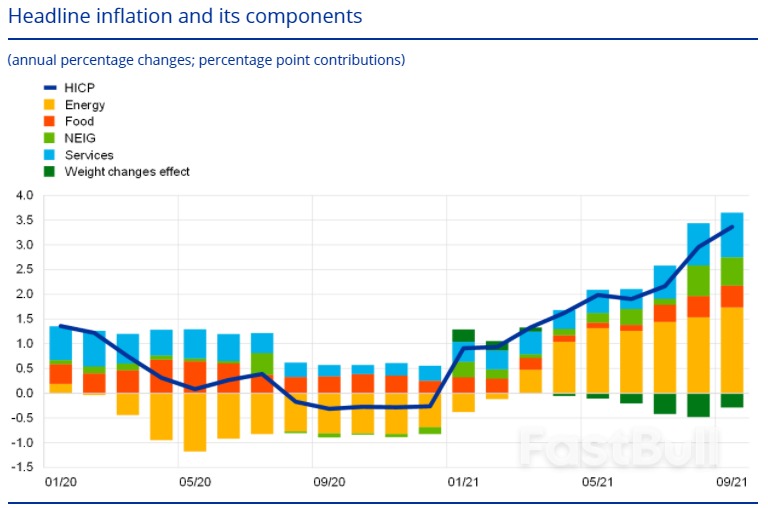

Eurostat's report released in September showed that annual HICP inflation in the euro area rose further to 3.4% in September, up from 3.0% in August, and well above the ECB's stated inflation target. The euro-area inflation is expected to rise further by the end of this year. The inflation spike is mainly affected by three factors: one, the reopening of the euro area economies so that the strong will to recover, demand is stronger than supply leading to higher commodity prices. Second, energy prices rose sharply, accounting for about half of the overall inflation in September. In particular, crude oil prices rose, with OPEC failing to meet its targets in August and September and supply weakening. Third, the base effect associated with the end of the German VAT cut is still pushing up inflation. Based on the combination of the above three factors, inflation in the euro area will remain high.

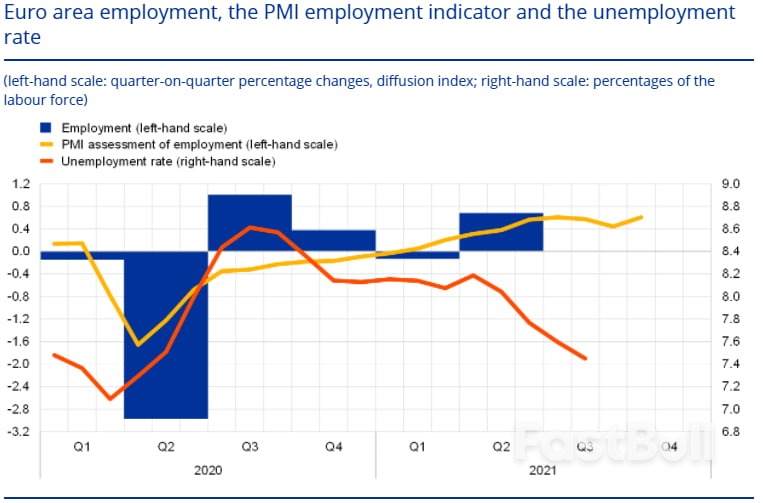

The unemployment rate in the euro area declined in August, still supported by job retention schemes. The rate stood at 7.5% in August, 0.1 percentage points lower than in July and around 0.1 percentage points higher than before the pandemic in February 2020. The number of workers in job retention schemes is declining and represented around 2% of the labour force in August. Employment increased by 0.7% in the second quarter of 2021 and total hours worked increased by 2.3% in the second quarter. However, total hours worked in the second quarter of 2021 remained below the level recorded in the fourth quarter of 2019. Similarly, labour force participation in the second quarter of 2021 was still lower than pre-crisis levels by around 1.4 million people. It suggests that the employment status in the euro area is still not optimistic and will hardly improve in the short term.

Overall, economic outlook for euro area has brightened over the past months but it is mainly relying on the government's easing of control over the epidemic. Nevertheless, the pandemic in the EU remains very serious, perhaps the short-term recovery of the economy is only the "Prague Spring" and it is not sustainable, coupled with the fact that supply chain bottlenecks have still not been effectively addressed. In the long run, it will inevitably continue to drag down European economy. Meanwhile, the euro presents a clear depreciated trend since the end of May; the support level below is weaker, and the overall is in a downward trend.

The risk of loss in trading financial assets such as stocks, FX, commodities, futures, bonds, ETFs or crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No consideration to invest should be made without thoroughly conduct your own due diligence, or consult with your financial advisors. Our web content might not suit you, since we have not known your financial condition and investment needs. It is possible that our financial information might have latency or contains inaccuracy, so you should be fully responsible for any of your transactions and investment decisions. The company will not be responsible for your capital lost.

Without getting the permission from the website, you are not allow to copy the website graphics, texts, or trade marks. Intellectual property rights in the content or data incorporated into this website belongs to its providers and exchange merchants.

At the plenary session of the House of Representatives on the 10th, Hiroyuki Hosoda, the chairman of the largest intraparty faction of the LDP, the Seiwa political research council, was elected as one of the speakers of the House of Representatives. As a rule, the speaker will leave the party membership. For this reason, senior officials of the

At the plenary session of the House of Representatives on the 10th, Hiroyuki Hosoda, the chairman of the largest intraparty faction of the LDP, the Seiwa political research council, was elected as one of the speakers of the House of Representatives. As a rule, the speaker will leave the party membership. For this reason, senior officials of the