- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Despite vast reserves, Venezuela's oil revival poses immense costs and political hazards for US energy firms.

The U.S. government is presenting American energy giants with a historic opportunity: the chance to rebuild Venezuela’s shattered oil industry. But for companies like Exxon Mobil, Chevron, and ConocoPhillips, it’s an offer that might be too risky to accept.

Following the hypothetical ouster of Venezuelan President Nicolas Maduro, the Trump administration reportedly plans to meet with oil executives to map out a strategy for boosting the nation's crude production. The prize is access to the world’s largest oil reserves, totaling over 300 billion barrels—roughly one-fifth of the entire global supply. Yet, a closer look reveals a minefield of economic and political challenges.

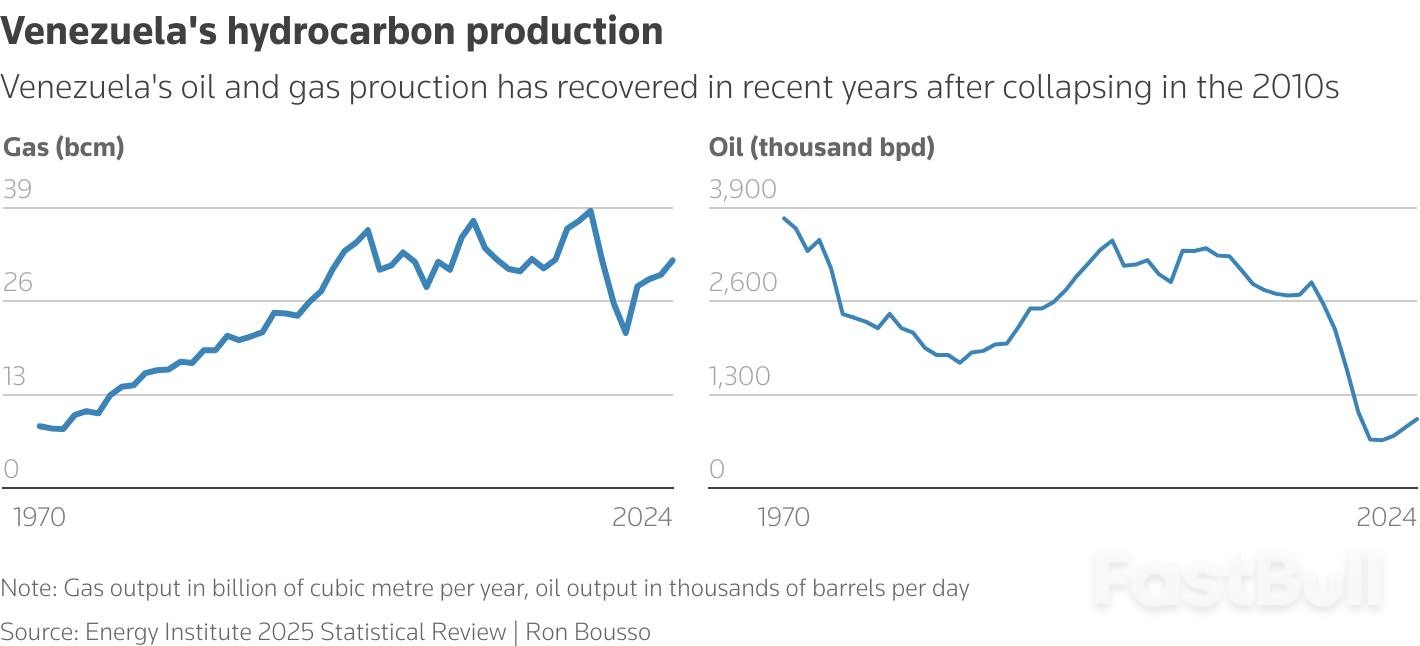

The potential upside in Venezuela is immense. After years of mismanagement and crippling U.S. sanctions, the country's oil output has plummeted. From a peak of over 3.5 million barrels per day (bpd) in the 1970s, when it accounted for 8% of global supply, production fell below 1 million bpd last year, making up less than 1% of the world's total.

An opening of this magnitude is rare. It echoes historic moments like the fall of the Soviet Union in the 1990s and the aftermath of Saddam Hussein's rule in Iraq, both of which saw Western energy majors scramble for control of valuable assets. The timing also seems opportune, as company boards have recently approved billions in new investments to expand their global market share.

However, reviving Venezuela’s oil sector is far from a straightforward proposition.

Serious operational and financial hurdles lie beneath the ground, casting doubt on the profitability of Venezuelan oil.

Technical and Cost Hurdles

Most of Venezuela's reserves, concentrated in the Orinoco belt, consist of heavy and extra-heavy crude. This highly viscous oil is difficult and expensive to handle. It must be blended with lighter diluents and processed through specialized upgraders before it can be extracted, transported, and refined.

This energy-intensive upgrading process also carries a significant carbon footprint. As governments worldwide move toward taxing emissions, the cost of producing these carbon-heavy grades could rise even further.

Unfavorable Breakeven Economics

According to consultancy Wood Mackenzie, the breakeven cost for key grades in the Orinoco belt already averages over $80 a barrel. This places Venezuelan production at the high end of the global cost curve for new projects. For comparison, heavy oil from Canada has an average breakeven point of around $55 a barrel.

These figures clash with the current strategies of U.S. majors, which are focused on low-cost fields.

• Exxon Mobil is targeting a global production breakeven of $30 a barrel by 2030, driven by assets in Guyana and the U.S. Permian shale basin.

• Chevron has a similar target.

• ConocoPhillips aims to generate free cash flow even if oil prices drop to $35 a barrel.

With crude oil currently trading around $60, and boards demanding strict spending discipline, convincing executives to invest billions in high-cost Venezuelan barrels is a tough sell. Carlos Bellorin, an analyst at Welligence Energy, notes, "The opportunity must be compelling enough to offset the substantial political risk that will persist in the years ahead." Unless a new, industry-friendly government in Venezuela dramatically reforms tax and royalty policies, the numbers simply don't add up.

Beyond the geology and economics, the political landscape in Venezuela presents an even greater deterrent.

Investing in Deep Uncertainty

Oil companies are accustomed to political risk, having operated for decades in volatile regions like Libya, Iraq, and Angola. But the current situation in Venezuela—marked by an uncertain power transition—is exceptionally hazardous.

Without a stable government in Caracas capable of earning the trust of international investors and banks, major firms will be hesitant to make long-term commitments. The appeal of buying cheap assets evaporates if the contracts underpinning them cannot be trusted.

The Peril of Aligning with U.S. Foreign Policy

U.S. oil majors have spent decades carefully cultivating an image of independence from American foreign policy, assuring investors that their decisions are driven solely by shareholder returns. Being seen as instruments of the U.S. president’s agenda could damage that reputation.

This creates a difficult dynamic. President Trump claimed he spoke with major U.S. energy firms about his plans for Venezuela, a statement company executives refuted. While contradicting the White House carries its own risks, especially as government involvement in the economy grows, openly aligning with its foreign policy is equally perilous.

Ultimately, the oil giants will likely signal a willingness to explore opportunities in Venezuela, partly to appease the administration. But the real question is whether they will commit billions of dollars to a country synonymous with corruption and economic chaos. For now, that seems to be a risk too great to take.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up