Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Amid a blizzard of contradictory signals, it's becoming increasingly difficult to get any visibility on the U.S. labor market.

Amid a blizzard of contradictory signals, it's becoming increasingly difficult to get any visibility on the U.S. labor market. But of all the numbers that feed into the all-important unemployment rate, the one worth paying most attention to may be continuing weekly jobless claims.

Federal Reserve Chair Jerome Powell has said that while he and his colleagues look at the "totality" of the data, the best gauge of the health of the labor market is the unemployment rate. That's currently 4.2%, low by historical standards, and consistent with an economy operating at full employment.

But it is a lagging indicator, meaning that once it starts to rise sharply, the economy will probably already be in a very precarious position. And it is also being depressed by labor demand and supply factors unique to the U.S.'s current high tariff, low immigration era.

Economic growth is slowing. Broadly speaking, it is running at an annual rate of just over 1%, half the pace seen in the last few years. Unsurprisingly, firms' hiring is slowing too.The latest Job Openings and Labor Turnover Survey, or JOLTS, showed hiring in June was the weakest in a year, while July's nonfarm payrolls report and previous months' revisions were so disappointing that President Donald Trump fired the head of the agency responsible for collecting the data.

But the unemployment rate isn't rising, largely because firms aren't firing workers. Why? Perhaps because they are banking on tariff and inflation uncertainty lifting in the second half of the year. It's also possible that firms are still scared form the post-pandemic labor shortages.Whatever the reason, the pace of layoffs simply has not picked up, the monthly JOLTS surveys show. Layoffs in June totaled 1.6 million, below the averages of the last one, two and three years.Meanwhile, lower immigration, increased deportations, and fewer people re-entering the labor force are offsetting weak hiring, thus keeping a lid on the unemployment rate. The labor force participation rate in July was 62.2%, the lowest since November 2022.

And what about weekly jobless claims, another key variable in the labor market picture? In previous slowdowns, rising layoffs would be reflected in a spike in the number of people claiming unemployment benefits for the first time.That's not happening either. Last week's 226,000 initial claims were right at the average for the past year, and only a few thousand higher than the averages over the past two and three years."It's a low fire, low hire economy," notes Oscar Munoz, U.S. rates strategist at TD Securities.

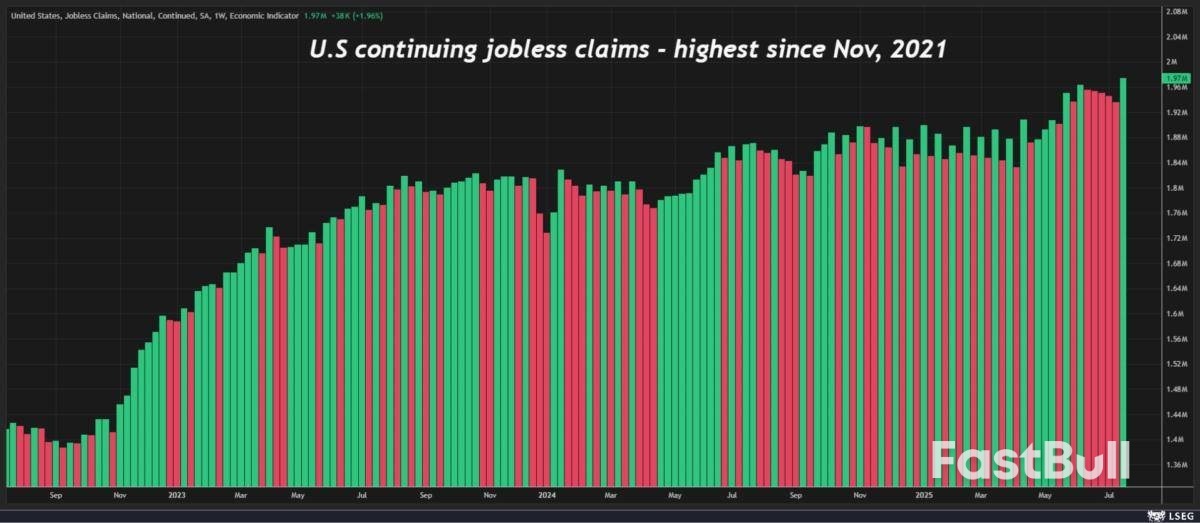

One high-frequency number that has gone under the radar, but which merits more attention is continuing jobless claims, which measures the number of workers continuing to file for unemployment benefits after losing their jobs. Rising continued claims suggest people actively looking for a job are struggling to get one, a sign that the labor market could be softening.

That figure spiked last week to 1.97 million, the highest since November 2021, which in theory should put upward pressure on the unemployment rate.Using the 'stock' versus 'flow' analogy, continuing claims are the 'stock,' and weekly claims are the 'flow'. Everyone will have their own view on what's more important, but right now initial claims are offering no guidance while continuing claims are pointing to softening in the job market.

Munoz and his colleagues at TD Securities estimate that continuing claims of around 2.2 million would be consistent with an unemployment rate of 4.5%, a level of joblessness most economists agree would prompt the Fed to trim rates.That's also the year-end unemployment rate in the Fed's last economic projections from June, a set of forecasts which also penciled in 50 bps of easing by December.An unemployment rate of 4.4% would probably tip the balance on the Federal Open Market Committee, while 4.3% would make it a much closer call, perhaps a coin toss.

Further muddying the picture, other indicators suggest the labor market is ticking along nicely. July's payrolls report showed that average hourly earnings last month rose at a 3.9% annual rate, consistent with the level seen in the past year. And the average number of hours worked was 34.3 hours, right at the mean for the past two years.These numbers and the JOLTS data are released monthly, and there will be one more of each before the Fed's September 16-17 policy meeting.But if the increased focus on the unemployment rate means investors want a more regular labor market temperature check, they should keep a close eye on weekly continuing claims.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up