Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Japan Tankan Small Manufacturing Outlook Index (Q4)

Japan Tankan Small Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)A:--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)

U.K. Rightmove House Price Index YoY (Dec)A:--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)

China, Mainland Industrial Output YoY (YTD) (Nov)A:--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)A:--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)A:--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)A:--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)A:--

F: --

P: --

Canada Existing Home Sales MoM (Nov)

Canada Existing Home Sales MoM (Nov)A:--

F: --

P: --

Canada National Economic Confidence IndexA:--

F: --

P: --

Canada New Housing Starts (Nov)A:--

F: --

U.S. NY Fed Manufacturing Employment Index (Dec)

U.S. NY Fed Manufacturing Employment Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)A:--

F: --

P: --

Canada Core CPI YoY (Nov)A:--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)A:--

F: --

P: --

U.S. NY Fed Manufacturing Prices Received Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing New Orders Index (Dec)A:--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)A:--

F: --

P: --

Canada Core CPI MoM (Nov)A:--

F: --

P: --

Canada Trimmed CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)A:--

F: --

P: --

Canada CPI YoY (Nov)A:--

F: --

P: --

Canada CPI MoM (Nov)A:--

F: --

P: --

Canada CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)A:--

F: --

P: --

Canada CPI MoM (SA) (Nov)A:--

F: --

P: --

Federal Reserve Board Governor Milan delivered a speech U.S. NAHB Housing Market Index (Dec)--

F: --

P: --

Australia Composite PMI Prelim (Dec)

Australia Composite PMI Prelim (Dec)--

F: --

P: --

Australia Services PMI Prelim (Dec)--

F: --

P: --

Australia Manufacturing PMI Prelim (Dec)--

F: --

P: --

Japan Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. 3-Month ILO Employment Change (Oct)--

F: --

P: --

U.K. Unemployment Claimant Count (Nov)--

F: --

P: --

U.K. Unemployment Rate (Nov)--

F: --

P: --

U.K. 3-Month ILO Unemployment Rate (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Including Bonuses) YoY (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Excluding Bonuses) YoY (Oct)--

F: --

P: --

France Services PMI Prelim (Dec)

France Services PMI Prelim (Dec)--

F: --

P: --

France Composite PMI Prelim (SA) (Dec)--

F: --

P: --

France Manufacturing PMI Prelim (Dec)--

F: --

P: --

Germany Services PMI Prelim (SA) (Dec)

Germany Services PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Services PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. Services PMI Prelim (Dec)--

F: --

P: --

U.K. Manufacturing PMI Prelim (Dec)--

F: --

P: --

U.K. Composite PMI Prelim (Dec)--

F: --

P: --

Euro Zone ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Germany ZEW Current Conditions Index (Dec)--

F: --

P: --

Germany ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (Not SA) (Oct)--

F: --

P: --

Euro Zone ZEW Current Conditions Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (SA) (Oct)--

F: --

P: --

U.S. Retail Sales MoM (Excl. Automobile) (SA) (Oct)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

UK 30-year gilt yields surged to 5.71%, their highest since 1998, after a government reshuffle raised doubts over fiscal credibility. Sterling fell 1%. European bond yields also hit multi-year highs on debt concerns.

Global bond markets came under pressure in European session, led by a sharp selloff in long-dated UK gilts. Yield on UK 30-year surged past 5.65% to its highest in 27 years, breaking above the peak set in April. Investors are increasingly concerned that Prime Minister Keir Starmer’s government may abandon fiscal discipline ahead of the upcoming Budget.

French bonds also came under strain, with the 30-year yield climbing to its highest since 2009 as Prime Minister François Bayrou scrambles to shore up parliamentary support ahead of next week’s confidence vote. U.S. Treasury yields are climbing in tandem, with the 30-year approaching 5%—a level last seen in July.

The catalyst in the UK was Starmer’s reshuffle of his Downing Street team, including the appointment of Darren Jones as chief secretary to the Treasury to manage delivery of priorities. The changes, intended to strengthen economic governance ahead of the Budget, have instead rattled markets, with traders worried about a lack of coherent strategy to revive growth while borrowing continues to swell.

Adding to the unease, speculation has resurfaced that Chancellor Rachel Reeves could be sidelined. Markets have been sensitive to such risks before—when questions arose over Reeves’ position in July, gilt yields spiked on fears she might be replaced by a more left-leaning figure less committed to fiscal prudence. The latest political maneuvering has revived those anxieties.

The immediate market reaction suggests little confidence in the government’s direction. Investors are interpreting the moves as paving the way for more gilt issuance, higher inflation, and weaker commitment to fiscal rules. Expectations are building that the Budget could lean heavily on borrowing to fund spending promises rather than tax hikes, amplifying the pressure on long-dated debt.

In currency markets, Sterling has been the weakest performer of the day, weighed down by fiscal and political concerns. Yen and New Kiwi followed on the downside, while Ddollar rebounded on support from rising Treasury yields. Loonie and Swiss Franc also gained, while Euro and Aussie traded mid-pack.

In Europe at the time of writing, FTSE is down -0.60%. DAX is down -1.57%. CAC is down -0.31%. UK 10-year yield is up 0.077 at 4.831. Germany 10-year yield is up 0.044 at 2.794. Earlier in Asia, Nikkei rose 0.29%. Hong Kong HSI fell -0.47%. China Shanghai SSE fell -0.45%. Singapore Strait Times rose 0.52%. Japan 10-year JBG yield fell -0.019 to 1.606.

ECB Executive Board member Isabel Schnabel pushed back against further monetary easing, telling Reuters that policy maybe already “mildly accommodative” and that she sees no case for another rate cut at present. She noted that the economy has held up better than expected, underpinned by robust domestic demand and bolstered by a “significant fiscal impulse” from Germany’s investment plans in infrastructure and defense.

Schnabel also argued that global tariffs imposed by the Trump administration are likely “on net inflationary”, even without EU retaliation. “If you have an increase in input prices globally due to tariffs, and these propagate through global production networks, this will increase inflationary pressures everywhere,” she said.

Schnabel also dismissed concerns that a stronger Euro might weigh heavily on price dynamics. She said currency appreciation tied to improving Eurozone growth prospects would have a more limited pass-through, adding, “I am less concerned about exchange rate developments.” She stressed that she sees little chance of inflation expectations de-anchoring to the downside after years of price overshoots.

Looking forward, Schnabel warned that a more fragmented world with tighter supply chains, higher fiscal spending, and aging populations is structurally inflationary. In such an environment, she argued, “central banks around the world start to hike interest rates again may come earlier than many people currently think.”

Eurozone headline inflation inched higher in August, with the flash CPI rising to 2.1% yoy from 2.0% yoy, in line with expectations. The increase came largely from a slower drag in energy prices, though food and services inflation moderated slightly from July levels.

Core CPI, excluding food, energy, alcohol, and tobacco, remained unchanged at 2.3% yoy, defying expectations of a slight dip to 2.2% yoy. The measure has now held steady since May.

By component, food, alcohol and tobacco continued to drive the highest annual inflation rate at 3.2%, followed by services at 3.1%. Non-energy industrial goods stayed muted at 0.8%, while energy prices fell -1.9% from a year earlier. The data suggest inflation continues to stabilize near the ECB’s 2% target.

BoJ Deputy Governor Ryozo Himino warned in a speech today that U.S. trade policies are likely to weigh on Japan’s economy, with overseas slowdowns and weaker corporate profits feeding through domestically. While accommodative financial conditions should cushion the hit, Himino said the baseline scenario is for Japan’s growth to “moderate,” with downside risks from tariffs deserving greater attention.

Looking further ahead, Himino said Japan’s growth should eventually recover as overseas economies return to a more stable expansion path. But in the near term, the tariff shock remains the key uncertainty, with the risk of a “larger-than-expected impact” now seen as more pressing than the chance of a mild outcome.

On inflation, Himino noted that headline prices remain above the BoJ’s 2% target, by a “considerable margin”, due in part to surging rice prices and spillovers to other goods. However, he stressed headline inflation is expected to “decline in due course” as food-related effects fade. Underlying inflation, meanwhile, remains below target but is steadily rising, despite some potential “temporary halts”, supported by a wage–price feedback loop.

Summing up, Himino said the BoJ’s baseline scenario assumes headline inflation will cool, while core prices continue to edge toward 2%. If that path holds, it would be appropriate for the central bank to keep raising rates gradually, fine-tuning monetary accommodation in line with improving economic activity and stable price gains.

Daily Pivots: (S1) 0.8632; (P) 0.8652; (R1) 0.8665;

EUR/GBP’s strong rally today solidifies the case that corrective pattern from 0.8752 has completed at 0.8595. Intraday bias is back on the upside for retesting 0.8752. Firm break there will resume whole rally from 0.8221. Next target is 0.8867 fibonacci level. For now, further rise is expected as long as 0.8636 support holds, in case of retreat.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it’s reversing the down trend from 0.9267 (2022 high). But even if it’s a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8513) will argue that the pattern has completed and bring retest of 0.8221 low.

Rothschild & Co. is set to take over the United Arab Emirates subsidiary of the Liechtensteinische Landesbank, bolstering its presence in one of the world’s hottest markets for wealth management.The so-called referral agreement with LLB will add assets worth about 1 billion Swiss francs ($1.2 billion) to Rothschild’s Dubai-based franchise, according to a statement on Tuesday. LLB will focus on its locations in Liechtenstein, Switzerland, Austria and Germany, while recommending Rothschild & Co. to clients in the United Arab Emirates.

“In recent years, we have experienced continuous strong growth in our global Wealth Management and Middle East businesses,” Rothschild & Co. Executive Chairman Alexandre de Rothschild said in a separate statement. The latest deal “represents our high conviction in the UAE’s potential, given the increasing concentration of both regional and global wealth here.”The Paris-based bank opened a wealth management office last year in Dubai, where it will have about 25 employees after the agreement with LLB. The move will help the firm step up its regional offerings across public and private markets, as well as corporate advisory.

Other global firms have also bolstered their presence in the region in the past few years to capitalize on the burgeoning market for the ultra-rich. Citigroup Inc., Deutsche Bank AG, UBS AG and JPMorgan Chase & Co. have recruited private bankers while Azura Partners, a wealth manager founded by a former Julius Baer Group Ltd., is relocating its headquarters to Abu Dhabi from Monaco.Rothschild’s move is also another sign that major banks have shrugged off the geopolitical instability that marked the region in previous months. The world’s richest people and their wealth managers continue to flock to the region, lured by low taxes, business-friendly regimes and year-round sunshine.

Still, some firms have faced issues in the region, including HSBC Holdings Plc. Its Swiss private bank is ending relationships with wealthy Middle Eastern clients as part of efforts to lower its exposure to individuals it deems high-risk, Bloomberg News has reported.

Gold prices extended their rally on Tuesday, reaching 3,490 USD per troy ounce, approaching an all-time high. The metal found support in growing expectations of a Federal Reserve rate cut as soon as September, along with a concurrent weakening of the US dollar.

Last week’s US inflation report bolstered hopes of a shift towards a more accommodative monetary policy. Markets are now pricing in an almost 90% probability of a 25-basis-point rate cut. Officials from the central bank itself reinforced this view after Mary Daly, President of the Federal Reserve Bank of San Francisco, openly expressed her support for such a move.

The key event risk this week will be the US Non-Farm Payrolls (NFP) report, expected to define the scale and pace of the upcoming rate-cutting cycle.

US trade policy is also creating substantial uncertainty. An appeals court ruled that the majority of tariffs imposed by Donald Trump were illegal, but kept them in force until 14 October to allow for an appeal to the Supreme Court. This political uncertainty is further fuelling demand for safe-haven assets.

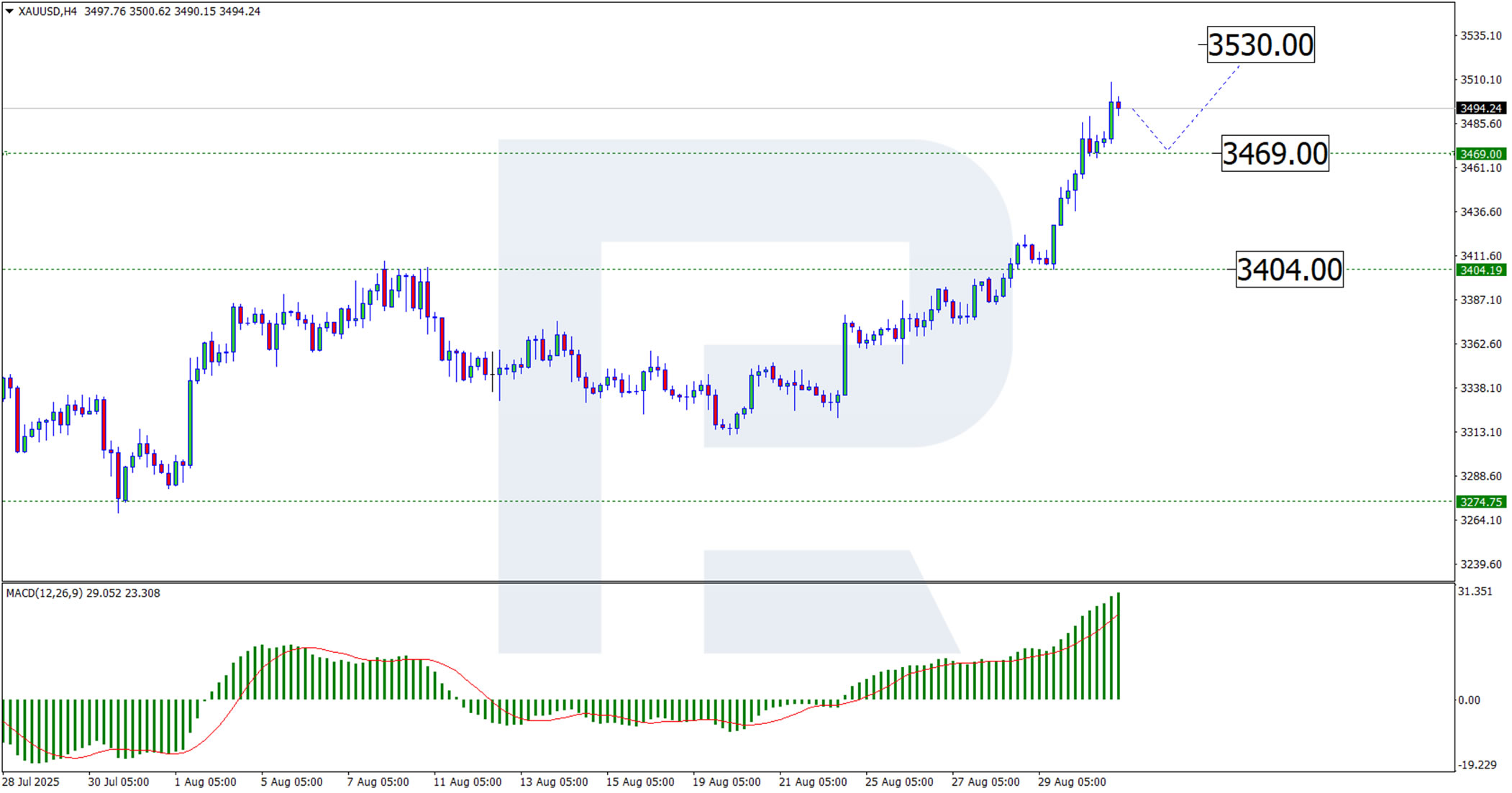

H4 chart:

The XAU/USD pair completed an upward wave towards the 3,508.65 USD level. The focus now shifts to a potential corrective wave towards the breached resistance level, which could now function as support. The target for this correction is 3,469 USD. Against the backdrop of the Federal Reserve’s supportive economic outlook, a test of this support could see prices stage another rally, with the first target likely being the 3,530 USD mark. This scenario is technically supported by the MACD indicator, whose histogram and signal line remain above zero and continue to rise, confirming the potential continuation of the upward trend. However, minor corrections cannot be ruled out.

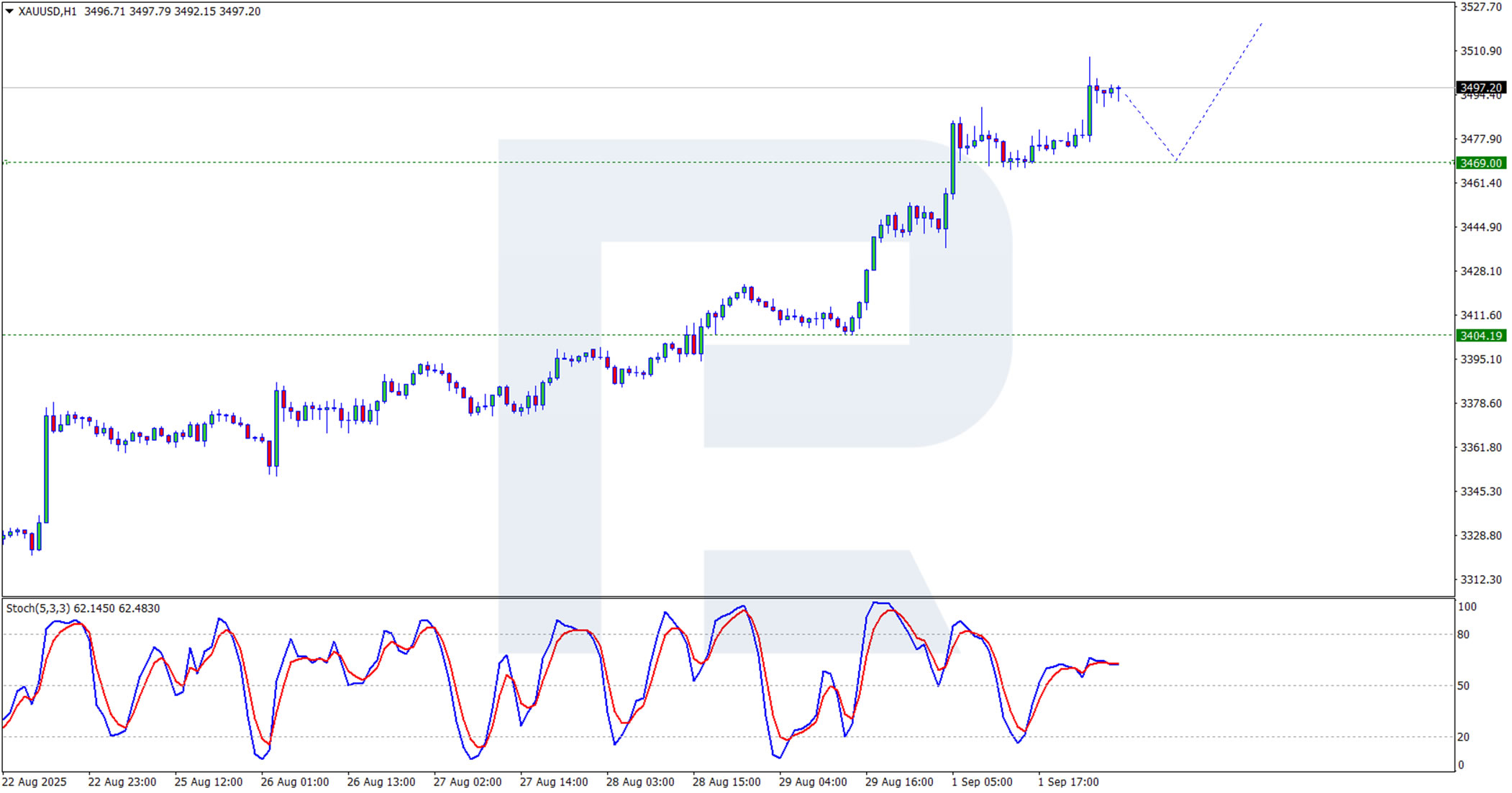

H1 chart:

After testing the 3,500 USD level, the price is forming a corrective wave. The target for this pullback could be the support at 3,469 USD. Testing this level could pave the way for the resumption of the upward trend. This outlook is technically supported by the Stochastic oscillator, whose signal lines, after a period of increase, are now declining towards 50.0.

A combination of dovish Fed expectations, a softer dollar, and geopolitical trade uncertainties continues to support gold prices. The technical picture suggests a brief period of consolidation or a shallow pullback is likely before a potential retest of record highs.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up