Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Tariff revenue is falling while refund lawsuits and legal risks continue to grow. Farmers and consumers face higher costs, with limited relief from temporary carveouts. Financial stress is rising as trade uncertainty spreads and liquidity signals weaken.

Tariffs have re‑emerged as a central pillar of U.S. trade policy. While the policy aims to reshape global trade and support domestic industries, early signs indicate falling revenue, rising costs, and growing legal risks. Economic and financial indicators now suggest mounting pressure across multiple sectors. This article presents the analysis of recent U.S. tariff actions, refund risks, and trade policy shifts, including the implications of the Trump-era trade measures.

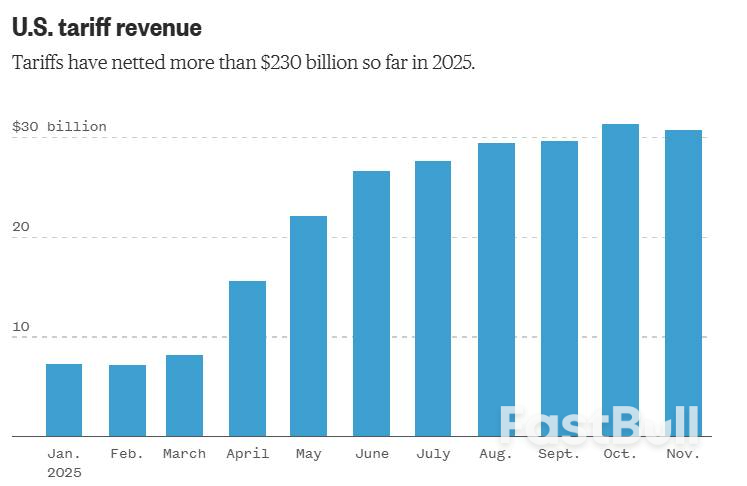

At a recent rally in Pennsylvania, President Trump expressed strong support for the use of tariffs. However, after lifting tariffs on items such as coffee, oranges, and cocoa, monthly tariff revenue declined from $31.35 billion in October to $30.76 billion in November. This marked the first monthly drop since the reimplementation of broad-based duties.

Since the start of his tariff policy, multiple proposals have been discussed regarding how the revenue could be used. These range from issuing direct payments to households to offsetting recent tax adjustments. However, these plans remain unconfirmed and have not been implemented.

Moreover, looming over the tariff debate is a Supreme Court case that could strike down most of the tariffs introduced under the Trump administration. If the court rules against them, the government may owe businesses up to $100 billion in refunds.

Several companies, including major retailers like Costco, have already filed lawsuits seeking repayment. They argue that the use of emergency powers under the IEEPA law may be found unlawful.

If the court agrees, it could challenge the legal basis of the tariffs and potentially increase the federal government's debt burden.

On the other hand, tariffs had a significant impact on U.S. farmers. During the early phase of the trade conflict, China halted purchases of American soybeans, causing prices to collapse and exports to slow.

In response, the administration announced a $12 billion bailout for the agricultural sector, stating that tariff revenue would fund the program. While farmers accepted the aid, many noted it fell short of addressing long-term challenges related to lost market access and profitability.

In recent months, policymakers introduced additional carveouts, including tariff reductions on beef, coffee, and bananas. These changes suggest increasing pressure on the tariff policy, highlighting how certain industries and consumers have been negatively affected.

Recent statements acknowledge that tariffs impose costs on domestic consumers. Independent estimates suggest that the average U.S. household has paid around $1,200 more as a result of these duties, adding pressure during a period of elevated inflation.

In practice, tariffs increase import costs for U.S. companies, which are often passed on to consumers through higher prices. This dynamic can reduce demand, strain household budgets, and weigh on overall economic activity.

Trade risks now extend beyond China. The U.S.-Indonesia trade deal faces uncertainty, with reports citing Jakarta's failure to meet certain commitments. If the agreement collapses, it could weaken broader trade objectives.

At the same time, U.S. officials approved chipmaker Nvidia to sell high-performance H200 chips to China. This move reflects a shift toward a more flexible and adaptive trade policy. In my view, it represents a pragmatic adjustment that strikes a balance between economic priorities and broader strategic interests.

The policy direction eases earlier restrictions. It also creates uncertainty over how national security concerns are balanced against the benefits of trade. This evolving approach underscores the complexity of modern trade policy, where economic competitiveness and security considerations must often be reconciled.

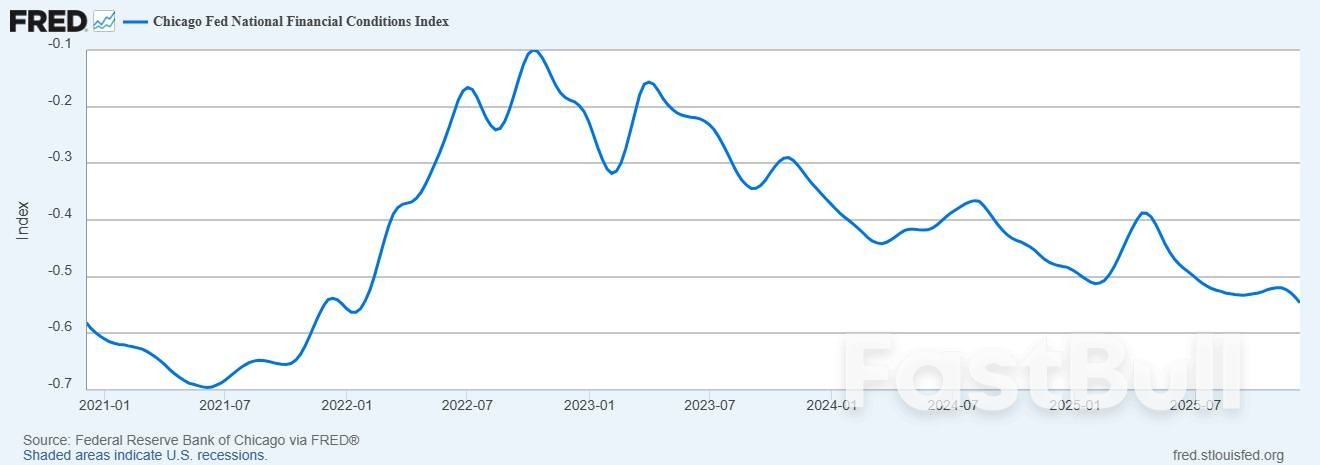

Beyond tariffs, broader financial indicators show warning signs. Unemployment claims dropped sharply. However, this decline might be due to seasonal distortions rather than genuine improvement.

The Chicago Fed National Financial Conditions Index fell to -0.546, indicating loose monetary conditions. While easy money supports elevated stock prices, it also increases the risk of asset bubbles.

The Trump trade war represents a high-stakes shift in U.S. trade strategy with broad economic consequences. Tariff revenue is declining, legal refund risks are increasing, and key industries, such as agriculture, continue to face pressure. Households are paying more, and financial markets are showing signs of stress. As trade relationships evolve and new policy adjustments emerge, the future direction of U.S. trade strategy remains uncertain and increasingly complex.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

*balance of positive-negative judgments; 2-month moving average, inventory judgment inverted (r.h.axis) Source: Statistics Netherlands, ING Research

*balance of positive-negative judgments; 2-month moving average, inventory judgment inverted (r.h.axis) Source: Statistics Netherlands, ING Research