Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Positive US fundamental data may trigger a rally in USDJPY towards 157.50.

Positive US fundamental data may trigger a rally in USDJPY towards 157.50.

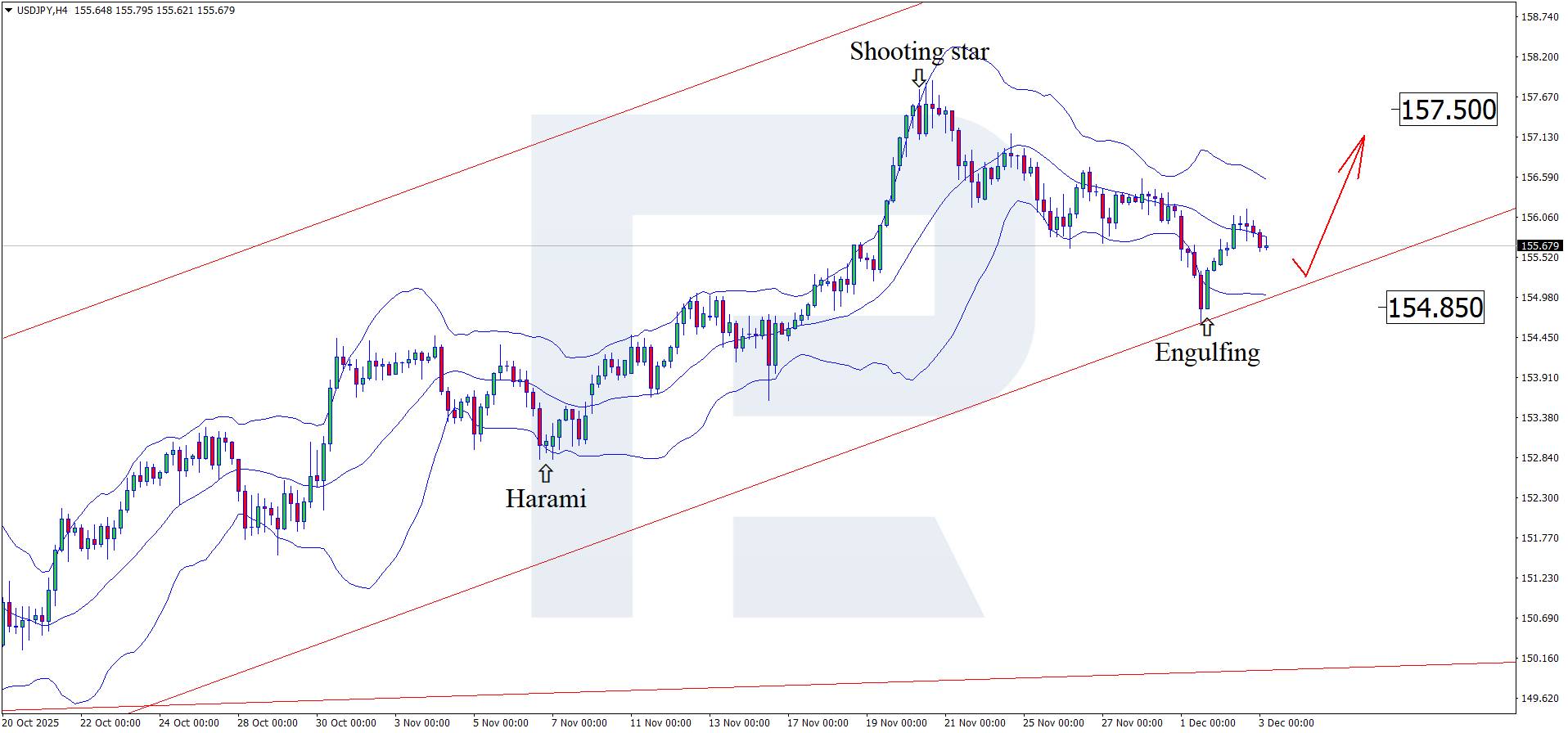

The forecast for 3 December 2025 considers that the USDJPY pair continues its correction, trading near 155.80.

Japan's services PMI covers multiple industries, including transport and communications, financial intermediation, business and household services, information technologies, hospitality, and food services.

The USDJPY forecast for today appears moderately optimistic for the Japanese yen, with the PMI up to 53.2 from 53.1 previously. At the moment, the PMI is above the 50.0 threshold, which may add support to the yen.

The US services PMI is also expected to rise to 55.0 from the previous 54.8. In this case, the increase in momentum may be slightly stronger, but it is still only a forecast. The actual figure may differ significantly, adding either support or pressure to the USD.

According to the forecast for 3 December 2025, ADP nonfarm employment change in the US may fall to 7 thousand, but this is only a projection. Last month, the number of employed grew more strongly than expected. The USDJPY forecast for today takes into account that a stronger-than-expected reading could support the US dollar and push the USDJPY rate higher towards 157.50.

On the H4 chart, the USDJPY pair has formed an Engulfing reversal pattern near the upper Bollinger Band and is currently trading around 155.80. At this stage, it may continue an upward wave following the pattern's signal, with a potential upside target at 157.50.

At the same time, the USDJPY forecast also considers an alternative scenario, where the price corrects towards 154.85 before rising.

Stronger US economic indicators may support the USD. The USDJPY technical analysis suggests a rise towards 157.50 after a correction.

EURUSD 2026-2027 forecast: key market trends and future predictions

EURUSD 2026-2027 forecast: key market trends and future predictionsThis article provides the EURUSD forecast for 2026 and 2027 and highlights the main factors determining the direction of the pair's movements. We will apply technical analysis, take into account the opinions of leading experts, large banks, and financial institutions, and study AI-based forecasts. This comprehensive insight into EURUSD predictions should help investors and traders make informed decisions.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up