- WTI

- XAUUSD

- XAGUSD

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

We will soon find out if tariffs are unconstitutional.

We will soon find out if tariffs are unconstitutional.

Nov 5th will be a key date for markets: the Supreme Court will start hearing arguments on Trump's IEEPA tariffs.

And while markets don't seem particularly focused on this event, I believe it's crucial to be prepared for it.

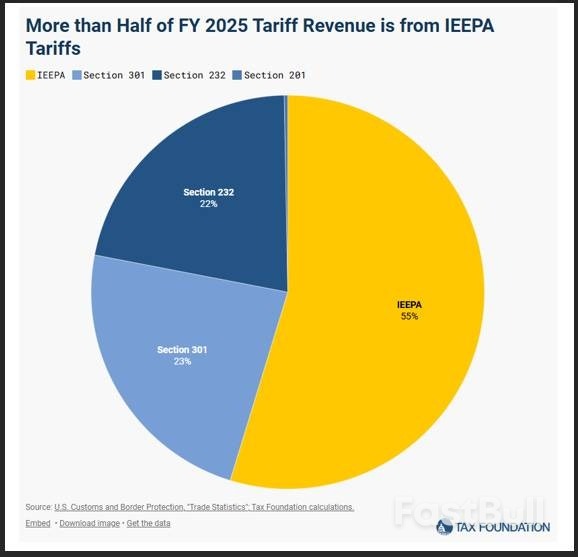

If the Supreme Court strikes down IEEPA tariffs as unconstitutional, around 55% of the US tariff income would be wiped out from the 2026 budget and US companies would be eligible for a refund for the 2025 tariffs paid under the IEEPA regime.

In numbers, we are talking about a $150-200bn annualized tariff income loss for the US.

Now, you all know that from a strict monetary perspective, the US tariffs act like a tax.

Data is uncontroversial there: tariffs are being paid by US consumers and corporates (mostly corporates), which is akin to an increase in corporate tax rate that reduces companies' margins.

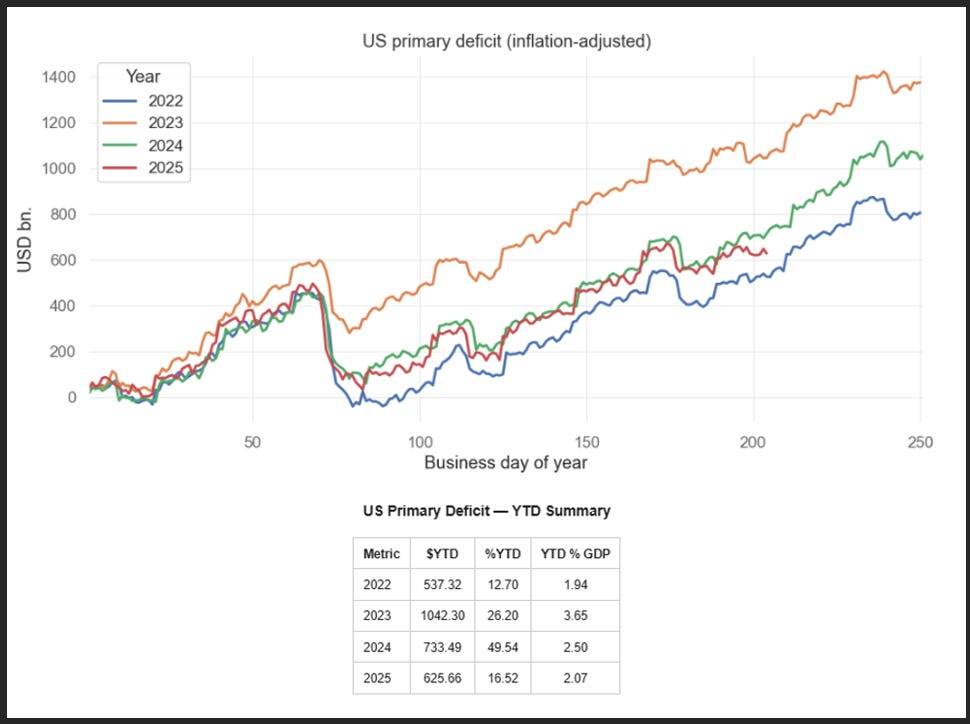

If the Supreme Court undoes IEEPA tariffs, this would be the equivalent of a ~200bn fiscal stimulus:

In 2025, the US government has injected $626 billion in the US economy – this is a much lower pace than 2023-2024. The slowdown in US primary deficit spending is mostly due to tariffs.

Revert the IEEPA tariffs, and the US will be going back to the glorious money-printing days of 2024 at least.

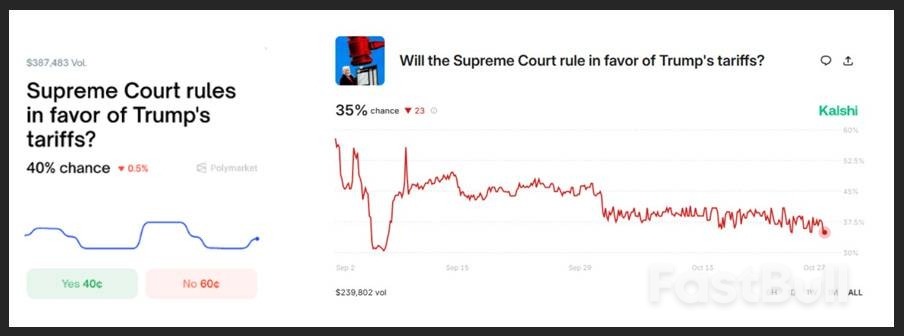

So, what are the odds that the Supreme Court will strike down Trump's IEEPA tariffs?

Prediction platforms suggest 60-65% odds, although volumes are quite small:

We can actually get an idea of the real market-implied odds by looking at another market: the newly set-up ''Tariff Refund Trade'' that certain banks are allowing hedge funds to invest in.

"Wall Street banks are arranging bets on President Donald Trump's tariffs being struck down by the Supreme Court — long-shot trades that could pay off handsomely for hedge funds betting against the legality of the administration's flagship policy.

Jefferies Financial Group Inc. and Oppenheimer & Co. are among firms brokering the deals, matching investors with companies that have paid tariffs to import goods into the US, according to people with knowledge of the matter and correspondence seen by Bloomberg News."

In the trades, the importing companies essentially sell to investors any future rights to claim refunds on their tariff bills, which could come if the nation's top court sides with an ongoing legal challenge to Trump's tariffs. The companies sell at a discount to their expected refunds, meaning investors would reap the upside in the event of a favorable ruling. The banks arranging the deals take a cut.

For example, a hedge fund might pay somewhere between 20 to 40 cents for each dollar of claims they could get back in refunds, giving them an upside of several times their bet, according to the correspondence and some of the people, who asked not to be identified discussing potential terms. Most of the trades range in size from $2 million to $20 million, with few over $100 million, one of the people said.''

It would seem that hedge funds are paying ~30% on average upfront for the trade, which implies roughly the same probability that tariffs are deemed unconstitutional.

But companies are cashing in months in advance the US government refund that would come if IEEPA tariffs are shut down, so we need to make an adjustment for that.

This cross-check says the real market-implied odds of tariffs deemed unconstitutional are closer to the 40-45% area, while prediction platform sit around 60-65%.

Call it 50-50: a coin toss.

Now, let's assume the Supreme Court strikes IEEPA tariffs down.

Can we say with 100% certainty that this will be akin to a ~200bn fiscal stimulus?

Not so fast.

Trump can also set tariffs under Section 232, 301 and 122.

Section 232 covers the sectorial tariffs under commerce authority, and Section 301 the ''fentanyl-like'' tariffs under USTR authority – both fall under the executive (President) powers, not the Congress.

Section 122 also falls under Presidential powers, and it would allow Trump to go for global 15% tariffs for 150 days before Congress would have to approve.

I am saying this because while the Supreme Court might strike down IEEPA tariffs, the Trump administration has seven Section 232 sectoral investigations ending by January 2026 and could come up with more Section 301 or blanket Section 122 tariffs to offset the Supreme Court decision.

Nevertheless, we are going into a coin-flip decision and markets might find reasons to celebrate a Supreme Court decision to strike down IEEPA tariffs – but Trump has weapons to counter such decisions.

Regardless of the Supreme Court decision, the global money printing machine will accelerate.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up