Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Japan Tankan Small Manufacturing Outlook Index (Q4)

Japan Tankan Small Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)A:--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)

U.K. Rightmove House Price Index YoY (Dec)A:--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)

China, Mainland Industrial Output YoY (YTD) (Nov)A:--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)A:--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)A:--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)A:--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)A:--

F: --

P: --

Canada Existing Home Sales MoM (Nov)

Canada Existing Home Sales MoM (Nov)A:--

F: --

P: --

Canada National Economic Confidence IndexA:--

F: --

P: --

Canada New Housing Starts (Nov)A:--

F: --

U.S. NY Fed Manufacturing Employment Index (Dec)

U.S. NY Fed Manufacturing Employment Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)A:--

F: --

P: --

Canada Core CPI YoY (Nov)A:--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)A:--

F: --

P: --

U.S. NY Fed Manufacturing Prices Received Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing New Orders Index (Dec)A:--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)A:--

F: --

P: --

Canada Core CPI MoM (Nov)A:--

F: --

P: --

Canada Trimmed CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)A:--

F: --

P: --

Canada CPI YoY (Nov)A:--

F: --

P: --

Canada CPI MoM (Nov)A:--

F: --

P: --

Canada CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)A:--

F: --

P: --

Canada CPI MoM (SA) (Nov)A:--

F: --

P: --

Federal Reserve Board Governor Milan delivered a speech U.S. NAHB Housing Market Index (Dec)--

F: --

P: --

Australia Composite PMI Prelim (Dec)

Australia Composite PMI Prelim (Dec)--

F: --

P: --

Australia Services PMI Prelim (Dec)--

F: --

P: --

Australia Manufacturing PMI Prelim (Dec)--

F: --

P: --

Japan Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. 3-Month ILO Employment Change (Oct)--

F: --

P: --

U.K. Unemployment Claimant Count (Nov)--

F: --

P: --

U.K. Unemployment Rate (Nov)--

F: --

P: --

U.K. 3-Month ILO Unemployment Rate (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Including Bonuses) YoY (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Excluding Bonuses) YoY (Oct)--

F: --

P: --

France Services PMI Prelim (Dec)

France Services PMI Prelim (Dec)--

F: --

P: --

France Composite PMI Prelim (SA) (Dec)--

F: --

P: --

France Manufacturing PMI Prelim (Dec)--

F: --

P: --

Germany Services PMI Prelim (SA) (Dec)

Germany Services PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Services PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. Services PMI Prelim (Dec)--

F: --

P: --

U.K. Manufacturing PMI Prelim (Dec)--

F: --

P: --

U.K. Composite PMI Prelim (Dec)--

F: --

P: --

Euro Zone ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Germany ZEW Current Conditions Index (Dec)--

F: --

P: --

Germany ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (Not SA) (Oct)--

F: --

P: --

Euro Zone ZEW Current Conditions Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (SA) (Oct)--

F: --

P: --

U.S. Retail Sales MoM (Excl. Automobile) (SA) (Oct)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

The Canadian dollar held near 1.3912 as markets awaited Powell’s Jackson Hole speech. Traders eye June retail sales rebound, while U.S.-Canada trade tensions persist. USD/CAD tests key resistance at 1.3926.

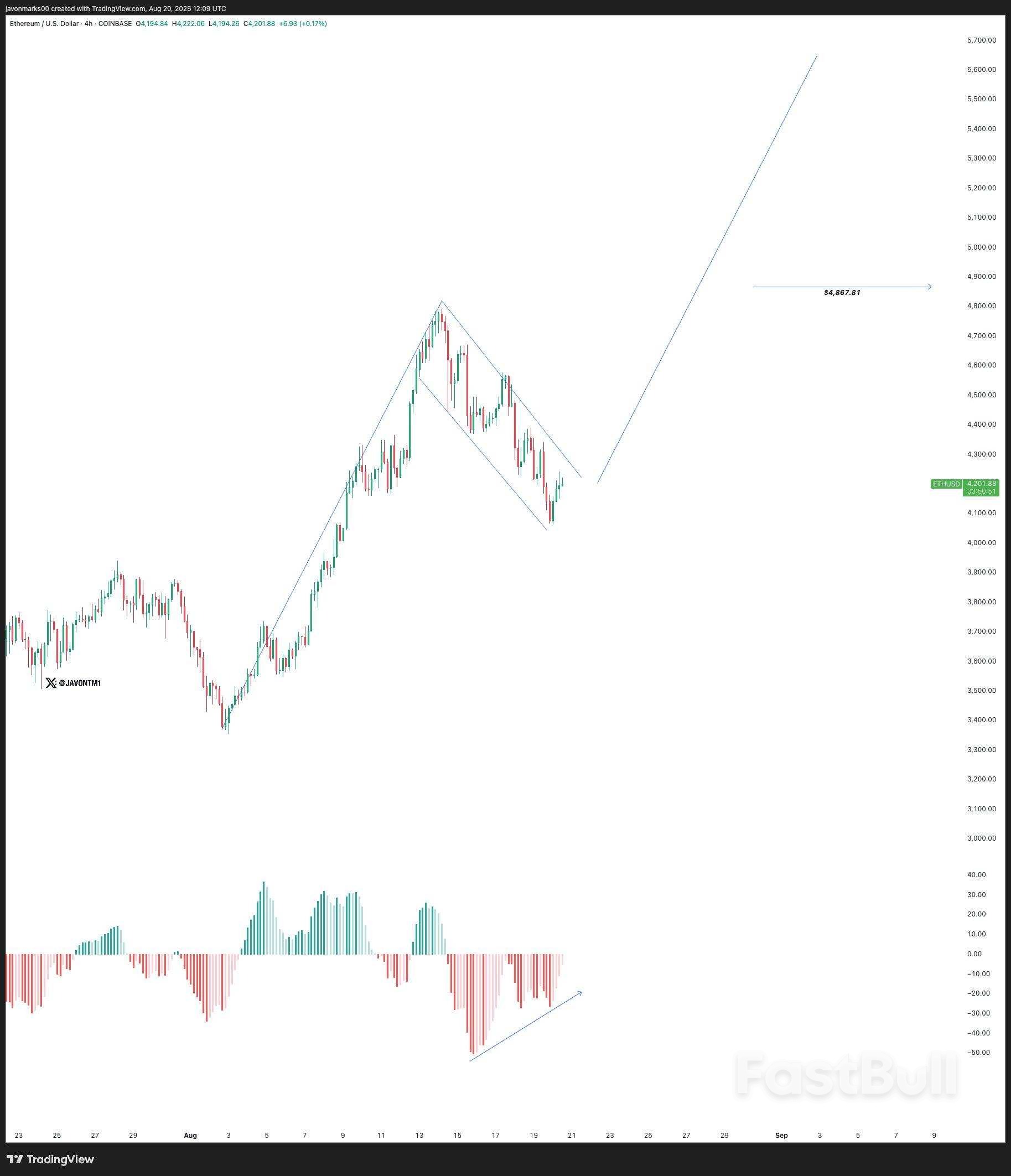

The asset is currently consolidating just below critical resistance levels, leaving traders divided between expectations of a bullish breakout and concerns that further retracement could follow.

Market analysts point to Ethereum’s daily chart, where price action has carved out a classic bull flag formation. This pattern typically signals continuation after a pause, suggesting that consolidation may soon give way to fresh momentum.

The recent pullback has been relatively orderly, with ETH maintaining higher lows even as selling persists. If Ethereum can break above resistance, analysts believe the move could carry prices toward $4,800 in the short term, and potentially as high as $5,500 if momentum builds. Failing to hold $4,200, however, may tilt sentiment toward deeper retracement.

Adding fuel to the debate, BlackRock recently reduced its exposure to Ethereum by unloading more than $254 million worth of the asset. The sale rattled markets, with some viewing it as simple profit-taking after ETH’s rally, while others fear it signals weakening institutional demand.

Uniswap Whales Are Dumping – Can UNI Survive the Next Correction?

Despite the headline-grabbing exit, technical indicators remain supportive. Chart structures still lean bullish, and analysts argue that Ethereum’s long-term trajectory is unlikely to be dictated by a single institutional move.

The balance between short-term caution and long-term optimism is defining Ethereum’s market narrative. If the bull flag confirms with a decisive breakout, Ethereum could not only challenge $5,500 but also position itself closer to retesting all-time highs.

While institutional flows may spark volatility, Ethereum’s price path remains heavily dependent on technical performance and retail conviction. For now, the asset sits at a pivotal level where the next breakout or breakdown will likely dictate momentum heading into the final months of the year.

The Reserve Bank of New Zealand (RBNZ) doesn’t need to be too stimulatory with policy because it views the recent lull in economic activity as temporary, according to chief economist Paul Conway.“We are seeing the weakness in the second quarter as a short-run phenomena driven by policy uncertainty that held back investment and created a bit of uncertainty for households,” he said in an interview on Friday in Wellington. “We do think that’s going to dissipate. I don’t think we need to be overtly stimulatory.”

The central bank lowered the Official Cash Rate (OCR) to 3% this week and surprised markets by signalling two further cuts to 2.5% by year-end. Having brought the OCR down from 5.5% in this easing cycle, policy settings are now seen as neutral rather than restrictive, and the RBNZ expects the economy to pick up in response.“That is going to encourage economic growth, like taking your foot off the brake is going to make the car go faster,” Conway said.

The RBNZ projects the OCR will average 2.6% in the year through March 2027, according to its monetary policy statement released on Wednesday. Conway said the level remains a neutral setting — one which neither curbs nor stimulate demand. He also noted that neutral is a range between 2.5% and 3.5%, but shouldn’t be viewed mechanistically.

“It’s not like there’s a magical number of the OCR beneath which the economy starts to recover,” he said.

New Zealand will likely post nil growth in the six months through September, the RBNZ said this week. Uncertainty over the impact of US tariff policies on global activity has had an out-sized impact on businesses, leading to less investment and hiring, while consumers curbed discretionary spending and stopped buying houses, it said.“The uncertainty has cleared a bit,” said Conway, adding that he expects the nation will bounce out of this “economic funk” by the end of the year.

“The concern around growth is that New Zealanders, we sort of talk ourselves into a deeper funk that persists into next year,” he said. “That’s the main growth risk and we’re at a turning point clearly.”

While a strong export performance is supporting growth, the revival of the housing market and its impact on residential construction will be fundamental to the economic recovery, Conway said. The RBNZ forecasts house prices will fall marginally this year after previously seeing a 3.5% gain in its May projections, but sees a lift in values in 2026.

Conway said New Zealand’s efforts to correct a supply imbalance by building more houses has been a factor in capping prices, though it’s too early to call a structural change.A better balanced market is “wonderful but it does have implications for the broader economy,” he said. “How can we grow this economy without that wealth effect coming through the housing market?”Alongside housing, the other key driver of the economy has been strong population growth via migration. Both of those channels appear to have changed recently, Conway said. Data this week showed people are leaving the nation at the highest rate in 13 years.

“It gets back to that question of where will growth come from,” he said. “If the housing market is working properly and there’s increased demand for houses, you get increased residential investment. So that’s economic activity. With migration, we’re forecasting it to turn around but that is shrouded in uncertainty.”

As investors wait anxiously for Federal Reserve Chair Jerome Powell’s keynote speech at the Jackson Hole symposium today, the rates market is responding to a mix of robust economic and price signals and hawkish statements from Powell's colleagues.

The Fed futures market has reduced the chances of a rate cut next month to just 70% from almost a sure thing not that long ago. Two-year Treasury yields have also matched their highest level since August 1 as some Fed officials - including Cleveland Fed boss Beth Hammack, Atlanta's Raphael Bostic and Kansas City's Jeffrey Schmid – expressed doubts about the wisdom of a September cut, with inflation still well above target and business surveys showing renewed vigour in the U.S economy.

U.S. stock futures steadied early Friday but only after this week’s tech stock wobble resulted in five straight daily loss in the S&P 500. The dollar notched its best level in about 10 days, with the yen at its weakest since August 1 on softer Japanese inflation data.

* Powell's Jackson Hole speech is typically a scene-setter for Fed policy over the year ahead and is expected to touch on changes to the average inflation targeting strategy as well as defending Fed independence - something in the spotlight again this week after administration demands for board member Lisa Cook to resign over alleged mortgage fraud. With minutes from the latest meeting and the latest Fed speeches showing no consensus on an urgent shift of stance, Powell is unlikely to signal a resumption of easing just yet - with no cast-iron case emerging from the latest sweep of economic data.

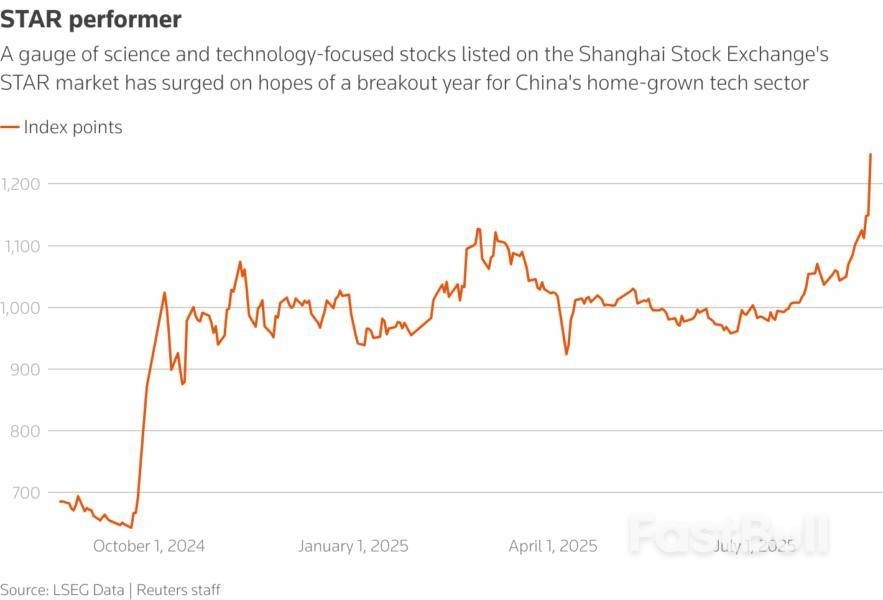

* Chinese stocks appear to be on a roll, with the Shanghai benchmark reclaiming 3,800 for the first time in a decade on domestic tech excitement. Tokyo's Nikkei was flat and the yen weaker on the inflation update there, but political paralysis in Japan is putting pressure on the bond market, with 10-year bond yields hitting the highest since 2008 and 30-year yields rising further to all-time peaks. With persistent calls for Prime Minister Shigeru Ishiba to step down after recent elections, things could come to a head next week when the ruling Liberal Democratic Party releases a report on reasons for the poor poll.

* Even as last weekend's excitement about a Ukraine peace deal has gone cold and Germany's second-quarter GDP was revised lower, European stocks were firmer on Friday - with some optimism about details of the U.S.-EU framework trade agreement released on Thursday and what it means for auto and pharma stocks. But Poland's WIG index posted its biggest decline in more than four months, falling 2.9% after the government proposed a hike to corporate income tax.

* Investors are bracing for volatility as Federal Reserve Chair Jerome Powell walks a fine line between curbing inflation and supporting the labor market, with thin August trading poised to magnify any market moves from his Jackson Hole speech on Friday.

* Vladimir Putin is demanding that Ukraine give up all of the eastern Donbas region, renounce ambitions to join NATO, remain neutral and keep Western troops out of the country, three sources familiar with top-level Kremlin thinking told Reuters.

* The Trump administration is considering a plan to reallocate at least $2 billion from the CHIPS Act to fund critical minerals projects and boost Commerce Secretary Howard Lutnick's influence over the strategic sector, two sources familiar with the matter told Reuters.

* Is the U.S. economic outlook so weak that it warrants multiple interest rate cuts? Or are U.S. markets pulling in huge inflows from abroad because the country's outlook is so attractive? ROI markets columnist Jamie McGeever explores this conundrum in his latest piece.

* Lambasting credit rating agencies is a favorite pastime of many debt market participants. However, writes Income Securities Advisor publisher Marty Fridson, self-interest appears to drive many of the most common criticisms, and history suggests these much-maligned appraisers actually do a pretty good job.

Chart of the day

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up