Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

France Industrial Output MoM (SA) (Oct)

France Industrial Output MoM (SA) (Oct)A:--

F: --

France Trade Balance (SA) (Oct)A:--

F: --

Euro Zone Employment YoY (SA) (Q3)

Euro Zone Employment YoY (SA) (Q3)A:--

F: --

Canada Part-Time Employment (SA) (Nov)

Canada Part-Time Employment (SA) (Nov)A:--

F: --

P: --

Canada Unemployment Rate (SA) (Nov)A:--

F: --

P: --

Canada Full-time Employment (SA) (Nov)A:--

F: --

P: --

Canada Labor Force Participation Rate (SA) (Nov)A:--

F: --

P: --

Canada Employment (SA) (Nov)A:--

F: --

P: --

U.S. PCE Price Index MoM (Sept)

U.S. PCE Price Index MoM (Sept)A:--

F: --

P: --

U.S. Personal Income MoM (Sept)A:--

F: --

P: --

U.S. Core PCE Price Index MoM (Sept)A:--

F: --

P: --

U.S. PCE Price Index YoY (SA) (Sept)A:--

F: --

P: --

U.S. Core PCE Price Index YoY (Sept)A:--

F: --

P: --

U.S. Personal Outlays MoM (SA) (Sept)A:--

F: --

U.S. 5-10 Year-Ahead Inflation Expectations (Dec)A:--

F: --

P: --

U.S. Real Personal Consumption Expenditures MoM (Sept)A:--

F: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

U.S. Consumer Credit (SA) (Oct)A:--

F: --

China, Mainland Foreign Exchange Reserves (Nov)

China, Mainland Foreign Exchange Reserves (Nov)A:--

F: --

P: --

Japan Trade Balance (Oct)

Japan Trade Balance (Oct)A:--

F: --

P: --

Japan Nominal GDP Revised QoQ (Q3)A:--

F: --

P: --

China, Mainland Imports YoY (CNH) (Nov)A:--

F: --

P: --

China, Mainland Exports (Nov)A:--

F: --

P: --

China, Mainland Imports (CNH) (Nov)A:--

F: --

P: --

China, Mainland Trade Balance (CNH) (Nov)A:--

F: --

P: --

China, Mainland Exports YoY (USD) (Nov)A:--

F: --

P: --

China, Mainland Imports YoY (USD) (Nov)A:--

F: --

P: --

Germany Industrial Output MoM (SA) (Oct)

Germany Industrial Output MoM (SA) (Oct)A:--

F: --

Euro Zone Sentix Investor Confidence Index (Dec)A:--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

U.K. BRC Like-For-Like Retail Sales YoY (Nov)

U.K. BRC Like-For-Like Retail Sales YoY (Nov)--

F: --

P: --

U.K. BRC Overall Retail Sales YoY (Nov)--

F: --

P: --

Australia Overnight (Borrowing) Key Rate

Australia Overnight (Borrowing) Key Rate--

F: --

P: --

RBA Rate Statement RBA Press Conference Germany Exports MoM (SA) (Oct)--

F: --

P: --

U.S. NFIB Small Business Optimism Index (SA) (Nov)--

F: --

P: --

Mexico 12-Month Inflation (CPI) (Nov)

Mexico 12-Month Inflation (CPI) (Nov)--

F: --

P: --

Mexico Core CPI YoY (Nov)--

F: --

P: --

Mexico PPI YoY (Nov)--

F: --

P: --

U.S. Weekly Redbook Index YoY--

F: --

P: --

U.S. JOLTS Job Openings (SA) (Oct)--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)--

F: --

P: --

U.S. EIA Short-Term Crude Production Forecast For The Year (Dec)--

F: --

P: --

U.S. EIA Natural Gas Production Forecast For The Next Year (Dec)--

F: --

P: --

U.S. EIA Short-Term Crude Production Forecast For The Next Year (Dec)--

F: --

P: --

EIA Monthly Short-Term Energy Outlook U.S. API Weekly Gasoline Stocks--

F: --

P: --

U.S. API Weekly Cushing Crude Oil Stocks--

F: --

P: --

U.S. API Weekly Crude Oil Stocks--

F: --

P: --

U.S. API Weekly Refined Oil Stocks--

F: --

P: --

South Korea Unemployment Rate (SA) (Nov)

South Korea Unemployment Rate (SA) (Nov)--

F: --

P: --

Japan Reuters Tankan Non-Manufacturers Index (Dec)--

F: --

P: --

Japan Reuters Tankan Manufacturers Index (Dec)--

F: --

P: --

Japan Domestic Enterprise Commodity Price Index MoM (Nov)--

F: --

P: --

Japan Domestic Enterprise Commodity Price Index YoY (Nov)--

F: --

P: --

China, Mainland PPI YoY (Nov)--

F: --

P: --

China, Mainland CPI MoM (Nov)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Bitcoin fell near $121,000 after hitting a record $126,000 earlier this week, but analysts say the “Uptober” bullish trend remains intact amid strong ETF inflows, low exchange supply, and resilient long-term holders.

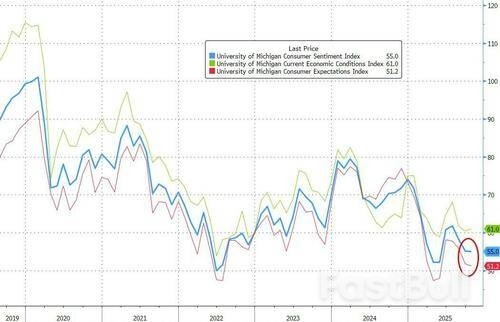

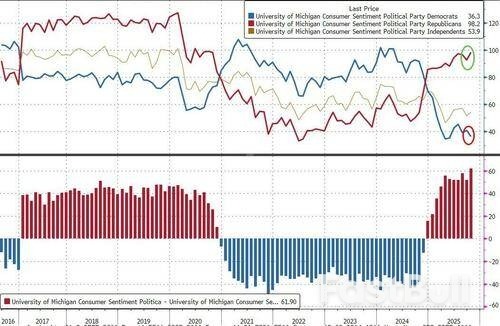

Amid a barren landscape of macro data due to the shutdown, the fact that many are strongly focused on the incredibly noisy and historically dismissed University of Michigan sentiment survey for any signals on inflation expectations or job hopes is in itself noteworthy.

So, with a big pinch of salt we dig in and see that the preliminary October headline sentiment index dropped very marginally (but was better than expected - 55.0 vs 54.0 exp vs 55.1 prior) with Current Conditions rising (from 60.4 to 61.0) and Expectations falling (from 51.7 to 51.2)...

On the inflation side, 1Yr expectations fell to 4.6% from 4.7% (while 5-10Y expectations were flat at 3.7%)...

On the unemployment side, the balance of respondents who expect a rise in unemployment rose modestly (but remain near multi-year lows)...

Under the hood, Republicans' confidence is at cycle highs while Democrats' confidence fell to Trump term lows...

UMich Surveys of Consumers Director, Joanne Hsu, noted that "improvements this month in current personal finances and year-ahead business conditions were offset by declines in expectations for future personal finances as well as current buying conditions for durables. Overall, consumers perceive very few changes in the outlook for the economy from last month. Pocketbook issues like high prices and weakening job prospects remain at the forefront of consumers’ minds."

Meanwhile, Hsu notes that "interviews reveal little evidence that the ongoing federal government shutdown has moved consumers’ views of the economy thus far."

Canada’s economy added a staggering 60k jobs in September (+0.3% month/month), 55k more than consensus expectations for a 5k gain. The details were similarly strong with full-time positions jumping 106k, and the private sector rising 22K.

The unemployment rate held steady at 7.1% in September, as the labour force more than made up for the past two months of losses, adding 72k workers.

Job gains were concentrated in manufacturing (+28k), health care and social assistance (+14k), and agriculture (+13k). The biggest losses were seen in wholesale and retail trade (-21k), construction (-8.2k), and transportation and warehousing (-7.4k).

Wage growth was steady in September with average hourly wages up 3.6% versus a year ago.

Well, that’s quite the surprise. Canada’s job market looks like it recovered all of August’s losses in September. Importantly, even for a noisy data series, this is a strong result. That said, it’s important to note that the unemployment rate remained unchanged as the labour force jumped by an even greater amount. Considering population growth slowed to 28k people, the biggest surprise was a large influx of new workers despite a weak job market.

The Bank of Canada’s next decision is due at the end of the month and this surprise from the labour market could change the calculus on the decision. However, underlying inflation continues to hover within the target range and the unemployment rate suggest that the labour market still has excess slack. The next inflation report is due on the 21st and the bar will be even higher for inflation to underperform and bring the BoC onside for another rate cut. Markets seems to agree as the pricing for a rate cut materially deteriorated this morning.

The RBA has almost certainly not yet decided whether or not to cut the cash rate in November. The data flow from here will determine the outcome, with hesitation now likely to result in more cuts later.

It’s almost certain that RBA has not yet decided whether or not to cut the cash rate at its November meeting. If the meeting were held today, they would keep rates on hold, awaiting further data. Several potentially decisive data releases are due before the actual meeting, though, including the September labour data and the full quarterly CPI. Until then, we need to hold two possible futures in mind: hold or cut.

The August CPI indicator did imply an ugly result for the September quarter. Our own nowcast for the trimmed mean measure is a ‘big’ 0.8%qtr that could easily round up to a 0.9%, a result that would surely stay the RBA’s hand. Looking at the detail, though, outside home-building costs it is not clear that the August data provided much signal of an ongoing higher rate of inflation than expected. As we noted at the time, the result in market services was mixed, with some personal services inflation below our forecasts while the cost of eating out was stronger. The latter suggests that, following a period of retrenchment in hospitality (evident in the labour account employment data), improving conditions have allowed for some margin repair. Some of the price gains may also indirectly relate to recent annual award wage increase; though this is a normal seasonal effect, its size will depend on how margins react. Neither of these influences on price growth are likely to be sustained if demand remains patchy.

We therefore think the economy could be in for something like a re-run of late 2023, when an upside surprise in September quarter inflation was followed by a downside surprise (to something more like our own near-cast) in the December quarter. The result was a hike in late 2023 followed by an ‘on-the-fly’ pivot following the February 2024 meeting – from flagging possible further hikes in the post-meeting statement to ‘not ruling anything in or out’ in the media conference. That message landed a lot better, and sure enough, the next move was, eventually, a cut.

We are also mindful of the two-sided risks around both the labour market and household spending data. We will know more about the labour market shortly when the September monthly labour force data is released next week, completing the picture for the quarter. So far, we see a gradual softening in employment growth as demand pivots away from the jobs-rich ‘care economy’. The unemployment and underemployment consequences of this are being masked by an unwind in the extra labour supply induced by earlier cost-of-living pressures. With demographic drivers still implying an upward trend in labour force participation, we see more latent labour market slack emerging over time and weighing on wages growth and inflation. There is precedent for this outcome in Australia’s experience in the late 2010s.

On household spending, the August Household Spending Indicator, released after the September RBA Monetary Policy Board (MPB) meeting, was notably below market expectations. This accords with our assessment that the expected recovery in consumer spending has been patchy and that the strength in national accounts consumption in Q2 partly reflected some one-off factors such as insurance payouts and the unwinding of some electricity rebates. Though we see two-sided risks around the consumption outlook, the more downbeat tone from consumer sentiment in recent months certainly suggests that underlying momentum is still subdued. Given how weak real household incomes have been for a number of years, this ongoing pessimistic tone does not surprise us.

Recall also that a recovery in household spending is necessary to counterbalance the slowdown in public sector demand growth that is already underway. Faster growth in household spending should only stay the MPB’s hand from further rate cuts if the pick-up is stronger than implied by the RBA’s August forecasts. These were constructed on an assumption of a couple more cash rate cuts, as the market was pricing at the time. Far too many observers are in the habit of seeing any pick-up in demand or housing prices as something for policy to react against, rather than as the expected and intended transmission of monetary policy. The Governor’s comments at the latest media conference show that the RBA, at least, does understand the difference.

The rates outlook boils down to the issue of how much signal to take from an upside surprise in one quarter in terms of what that means for subsequent quarters. RBA Governor Bullock has on several occasions insisted that ‘we will be guided by our forecasts’. However, that statement sits a bit uncomfortably with the flat profile for the RBA’s trimmed mean inflation forecasts and the unemployment rate. These give the impression of a set of forecasts being used as a communication device to explain and frame a policy decision rather than an independent input into that decision. This is understandable and perhaps inevitable given the judgement involved in synthesising the output of many different models and information sources. However, it does hold the risk that the policy view helps shape the forecast rather than the other way around.

What’s left in these circumstances is reactivity to incoming data – that is, to the recent past. As well as making policy less predictable – contrary to the MPB’s stated intentions – it is not a great way to run an economy policy setting that affects the economy with a lag, especially when inflation has been within the target range for a little while now at the same time as policy is likely still restrictive.

Bottom line: the odds that the RBA cuts in November are, at this point, below 50% but still a long way from zero. The data flow could change things again. Frankly, the prospect of flip-flopping a ‘call’ as the month goes on is unattractive, especially when it is quite obvious that the policymakers have not made up their mind yet. We must hold the two possibilities in mind at least until the labour market data come in. (A good-enough labour market result would make it unlikely that the RBA would cut, even if the September quarter CPI comes in a little more benign than we currently expect.)

The RBA communications schedule has half a dozen speeches between now and the November meeting that will be opportunities for it to provide guidance on some of its key forecast judgements, though they all pre-date the release of the September quarter CPI. If the RBA does hold in November, though, our conviction that they end up cutting in February rises, as does our expectation that the trough will be 2.85% rather than something higher. The more the MPB hesitates in the face of uncertainty, the more likely it is that domestic inflation pressures surprise it on the downside next year, and trimmed mean inflation turns out more like the Westpac Economics forecast than the August RBA one.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up