Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

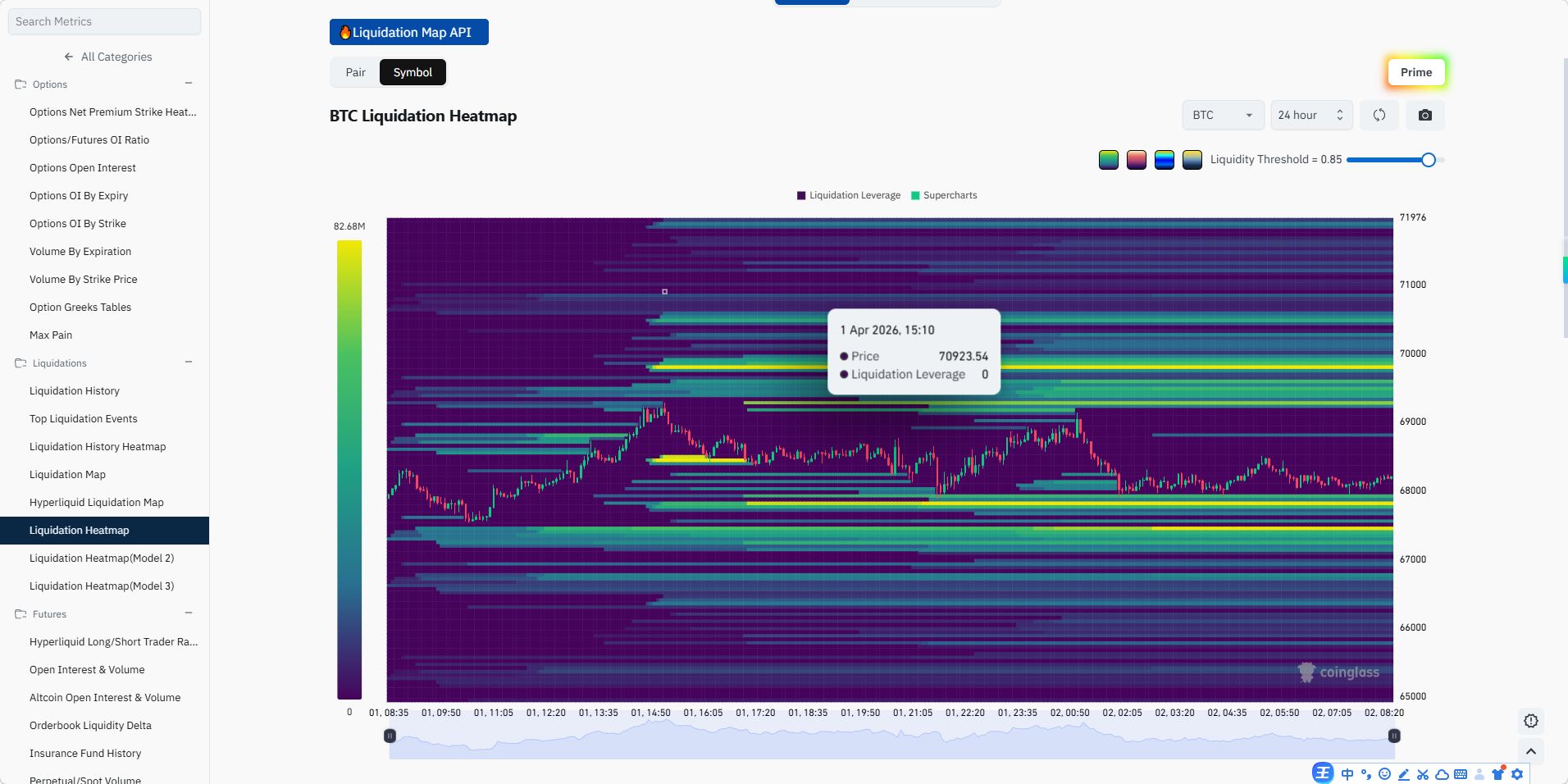

What to know Bitcoin surges to $91,000 due to institutional interest. Driven by Fed rate cut expectations. Investor confidence grows despite previous decline.

Bitcoin's price has surged back to $91,000 as of late November 2025, buoyed by institutional investor activity and favorable macroeconomic signals, notably due to potential Federal Reserve rate cuts.

This resurgence highlights market sensitivity to economic policy shifts, influencing both Bitcoin's valuation and wider cryptocurrency sentiment, with Ethereum also seeing gains above $3,000.

Bitcoin's price reached $91,000 in late November 2025, marking a strong recovery from previous lows near $80,000.

This rebound matters as it signals renewed institutional interest and aligns with expectations for a potential Federal Reserve rate cut.

Bitcoin has experienced a notable recovery attributed to macroeconomic optimism and institutional investor movements. Wall Street's growing interest in digital assets has driven increased trading volumes. Experts highlight support levels as crucial for ongoing price rallies.

The rebound follows an approximately 20% decline over the past month, impacted by market fluctuations and selling pressure from US-based investors. Analysts like Daan Crypto Trades emphasize the importance of the $89,000-$91,000 range.

The immediate effect on the cryptocurrency market has been significant, with a surge in trading volumes and increased buying pressure. Institutional trading volumes hitting $78 billion indicate significant inflows pushing the price above $91,000. Institutional investors leading the charge reflect heightened confidence.

Economically, expectations of a Federal Reserve rate cut have bolstered risk asset sentiment, further influencing Bitcoin's price trajectory. Ethereum similarly reacted, surpassing the $3,000 mark.

Similar rebounds have been observed during periods of anticipated monetary easing. Historical trends show support levels around $89,000-$91,000 often foreshadowing further rallies.

Experts speculate on potential outcomes, citing past rallies where sustained price levels led to significant gains. Michael Feroli, Economist at J.P. Morgan, noted,

"While the next FOMC meeting remains a close call, we now believe the latest round of Fedspeak tilts the odds toward the Committee deciding to cut rates in two weeks from today,"

Continued institutional interest and macroeconomic factors remain pivotal for future price stability.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up