Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

"...the most anticipated oil supply glut in history"...

There are some extreme dichotomies in the crude complex currently that are worth a quick look...

Amid what Eric Nuttall coined as "the most anticipated oil supply glut in history"...

... crude prices had fallen to 5-month lows just over a week ago. Then Washington unleashed sanctions on two of Russia's oil giants, Rosneft PJSC and Lukoil PJSC (and India and China suggested it would cut back on Russian oil purchases, implying demand for alternatives), prices for oil surged back higher...

OilPrice reports that India imported 19.93 million tons of crude oil last month, a 1.7% increase from August, the Economic Times reported, citing government data. The total is equal to roughly 4.87 million barrels daily.

The annual increase in imports for September was more pronounced, at 6.1%, the data also showed.

In oil products, the government's Petroleum Planning and Analysis Cell reported imports of 4.40 million tons, which was a 20.9% increase on September 2024. Product exports, on the other hand, fell by 4.8% to 6.18 million tons.

But, the publication also reported that Russian exports of crude oil to India declined by 8.4% over the three months to September amid shrinking discounts and tighter availability of barrels. The decline is expected to become sharper in the coming weeks, following the latest U.S. sanctions on Russian oil, targeting two of the largest exporters—Rosneft and Lukoil.

India needs more local discoveries of oil and gas in order to be able to meet future energy demand, the secretary of petroleum and natural gas at the Indian energy ministry said.

"One day, we will be looking at a situation where alternative forms of energy will increasingly matter more for incremental demand satisfaction than fossil fuels," Pankaj Jain said, as quoted by PTI.

Additionally, supertanker freight futures surged on Thursday and Friday after the U.S. sanctions against Russia's biggest oil firms created a rush to replace Russian barrels.

The front-month supertanker contracts on the route Middle East to China, the benchmark route, jumped by 16% on Thursday, to the highest level in nearly two years, according to data from the Baltic Exchange data cited by Bloomberg.

"We anticipate the rush for replacement crudes will be larger and more sustained because of the exhaustive list of Russian producers under OFAC sanctions," Anoop Singh, global head of shipping research at Oil Brokerage, told Bloomberg.

Supertanker rates were already rising earlier this month due to the latest tit-for-tat fees on port callings in the U.S.-China trade spat.

The port fees threaten to create additional vortexes in global oil flows.

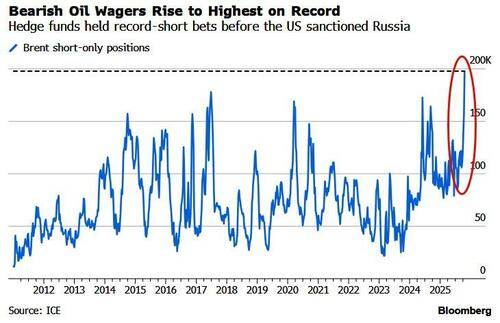

Ahead of the rally, money managers boosted bearish positions on the global benchmark by 40,233 lots to 197,868 in the week ended Oct. 21, according to ICE Futures Europe. That's the most on record... providing a lot of ammunition for a sizable short squeeze...

...as traders worldwide bet on mounting evidence that a long-anticipated supply surplus is finally underway with a flotilla of crude oil on the world's oceans expanded to a fresh high as producer nations keep adding barrels and the tankers sail further for deliveries...

Production is rising from members of the OPEC+ group of nations, which are unwinding earlier output cuts - as well as countries outside the group, predominantly in the Americas, where Guyana recently started pumping from a new offshore field and US output hit a new high.

The build-up comes at a time when demand growth is slowing, with forecasters predicting a surplus that could rise to as much as 4 million barrels a day in the early months of next year.

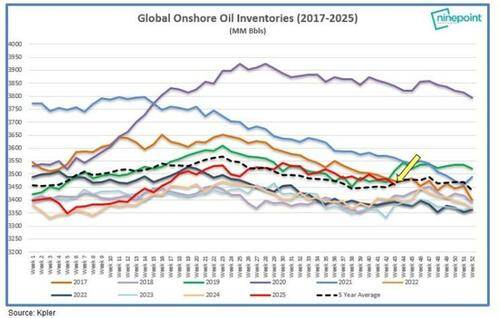

However, as Eric Nuttall reminds, inventory on land is much lower than expected...

"...onshore inventories have FALLEN by 39MM Bbls in the first 20 days of October, and are actually the tightest to the 5 year average in ~ 4 months. It wasn't supposed to be like this!"

...and much of the oil-on-water is already headed to specific processing units.

Finally, remember China is stockpiling 500k barrels-a-day for its own Strategic Petroleum Reserve, so there's plenty of demand (for bulls to squeeze on), but any progress toward peace, such as reviving Budapest meeting plans, may undermine the rally as will chatter that OPEC+ is currently expected to focus on reviving another modest sliver of oil production in December as a base case when key members meet this weekend, according to two delegates.

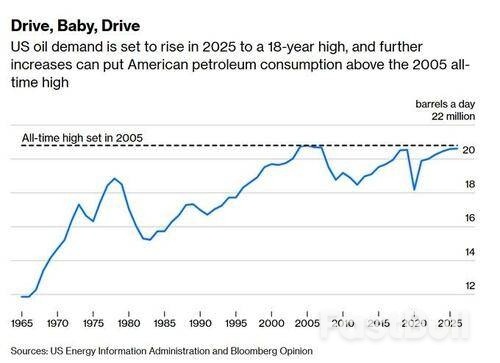

Domestic demand is booming too, as Bloomberg's Javier Blas notes, US oil consumption is heading toward a 18-year high of 20.59 million b/d in 2025. And further increases are likely.

That's a lot of supply, demand, and positioning extremes to consider.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

as of 26 Oct 2025. Past performance is not a reliable indicator of future performance.

as of 26 Oct 2025. Past performance is not a reliable indicator of future performance. as of 26 Oct 2025. Past performance is not a reliable indicator of future performance.

as of 26 Oct 2025. Past performance is not a reliable indicator of future performance. as of 26 October 2025. Past performance is not a reliable indicator of future performance.

as of 26 October 2025. Past performance is not a reliable indicator of future performance.

Daily Natural Gas

Daily Natural Gas