Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The Bank of England cut interest rates on Thursday after a narrow vote by policymakers but it signalled that the already gradual pace of lowering borrowing costs might slow further.

The Bank of England cut interest rates on Thursday after a narrow vote by policymakers but it signalled that the already gradual pace of lowering borrowing costs might slow further.

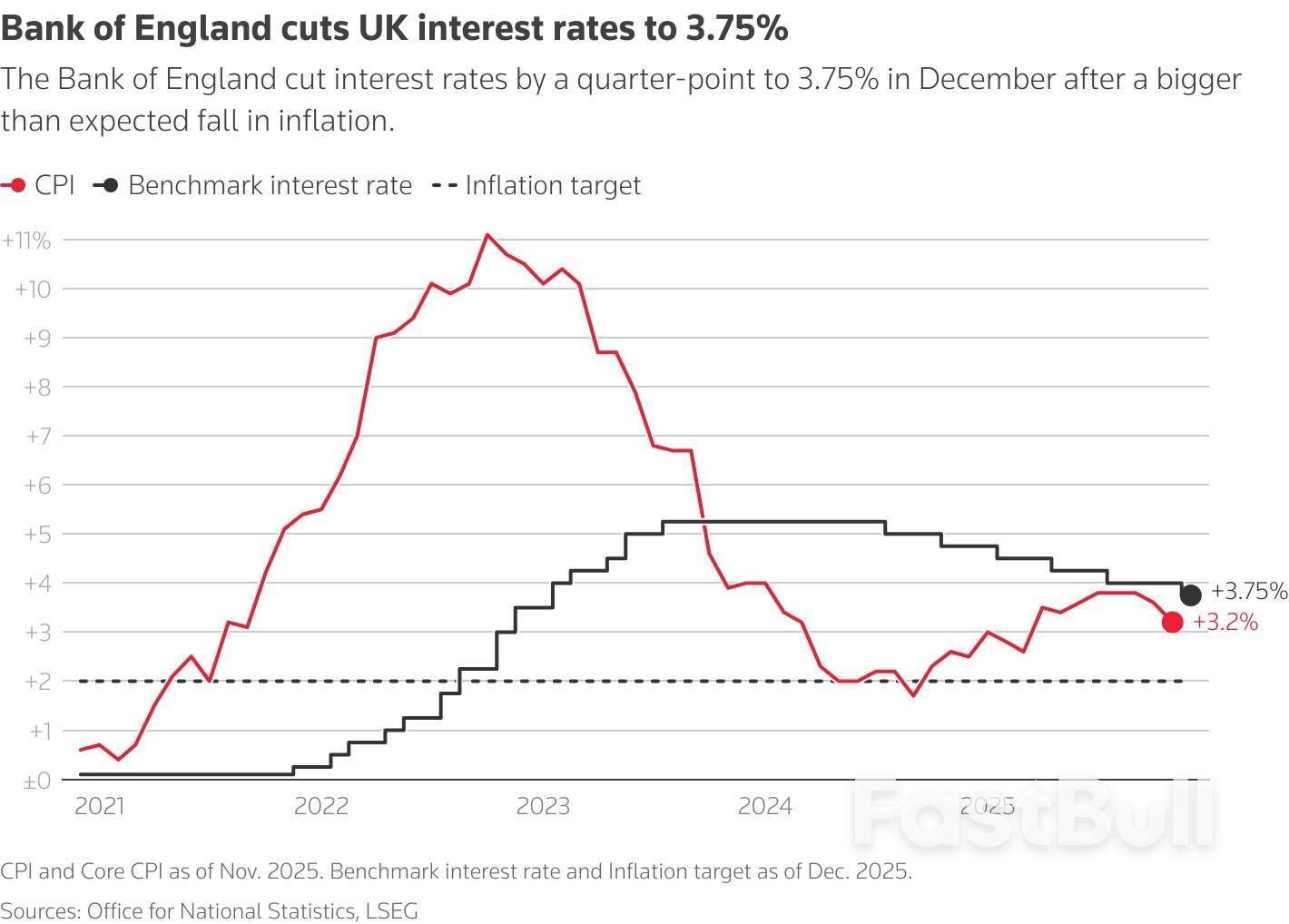

After a big drop in inflation and a new forecast from BoE staff that the economy is stagnating, five Monetary Policy Committee members voted to lower the BoE's benchmark rate for the sixth time since August 2024 to 3.75% from 4%.

The four other members supported no change as they worried about the potential for inflation - still the highest among the Group of Seven economies - to remain too high.

Analysts polled by Reuters last week had mostly expected a 5-4 vote for a rate reduction as Britain's economy struggles to grow and inflation falls.

Governor Andrew Bailey changed his view and voted for a cut as he sees inflation returning close to the BoE's 2% target as soon as April or May next year, about a year earlier than forecast by the central bank just last month.

But he cautioned that inflation still posed some risks.

"The calls will become closer, and I would expect the pace of cuts, therefore, to ease off at some point," he told broadcasters. "But I'm not going to judge exactly when that is, because it's too uncertain at the moment."

Sterling strengthened by as much as a cent against the U.S. dollar after the decision, before paring gains.

Interest-rate-sensitive two-year gilt yields - which were at their lowest since August 2024 before the decision was announced - rose as much as 6 basis points as investors saw slightly less chance of more than one rate cut next year.

A line chart with the title 'Britain's inflation and interest rates'

A line chart with the title 'Britain's inflation and interest rates'Sanjay Raja, chief UK economist at Deutsche Bank, said he was sticking to his forecast of two more quarter-point cuts in 2026 - in March and in June - but said there was a chance the BoE could move more slowly and ultimately have to cut rates more.

James Smith and Chris Turner, economists at ING, said the lines between the two MPC camps had become more blurred. Some of the policymakers who voted for a rate cut showed signs of concern about high wage growth while others among those who called for a hold hinted at diminishing inflation risks.

"That said, we don't view today's decision as a game-changer," they wrote in a note to clients. "Fundamentally, the Bank - or most officials at least - still think further cuts are likely. It has not changed our mind that the Bank will cut rates twice more next year."

Among the senior policymakers who voted against the rate cut, Deputy Governor Clare Lombardelli said she remained more concerned about the risk of inflation proving stronger than expected and the recent data had only softened "at the margin".

Chief Economist Huw Pill said he saw a bigger risk of inflation getting stuck too high than too low.

But Catherine Mann said her decision not to vote for a rate reduction was "quite finely balanced".

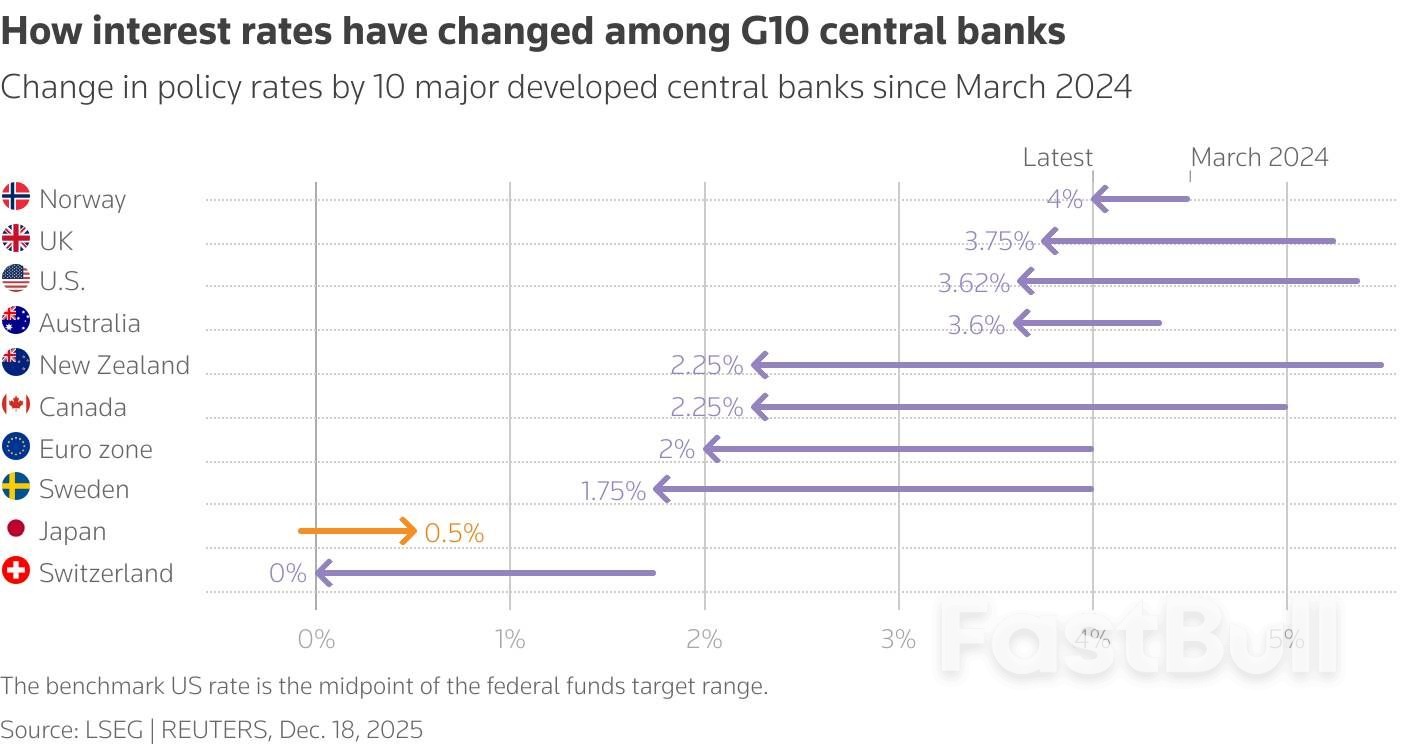

The cut took Bank Rate to its lowest level in nearly three years although it is still almost double the European Central Bank's equivalent rate which it kept on hold on Thursday.

British inflation remains higher than among peer economies - in part because of finance minister Rachel Reeves' decision last year to raise taxes on employers - even after it fell unexpectedly sharply to 3.2% in data released on Wednesday.

Data on Tuesday showed a weakening jobs market including the highest unemployment rate since 2021.

The BoE said it now expected the economy to stagnate in the last three months of 2025, down from a forecast of 0.3% growth made last month, although it thought underlying growth was stronger at about 0.2% a quarter.

Britain's economy shrank by 0.1% in the three months to October amid reports that businesses put investment projects on ice in the run-up to Reeves' budget on November 26.

The BoE said the budget would bring down inflation in 2026 by about half a percentage point due to one-off measures which would then push it up a bit in the following two years.

The budget measures would add at most 0.2% to the size of the economy in 2026 and 2027.

Other major central banks are believed to be close to halting their rate cuts. The U.S. Federal Reserve last week signalled one more move in 2026, while the ECB has probably already come to the end of its monetary loosening cycle.

An arrow chart with the title 'How interest rates have changed among G10 central banks'

An arrow chart with the title 'How interest rates have changed among G10 central banks'728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up