Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

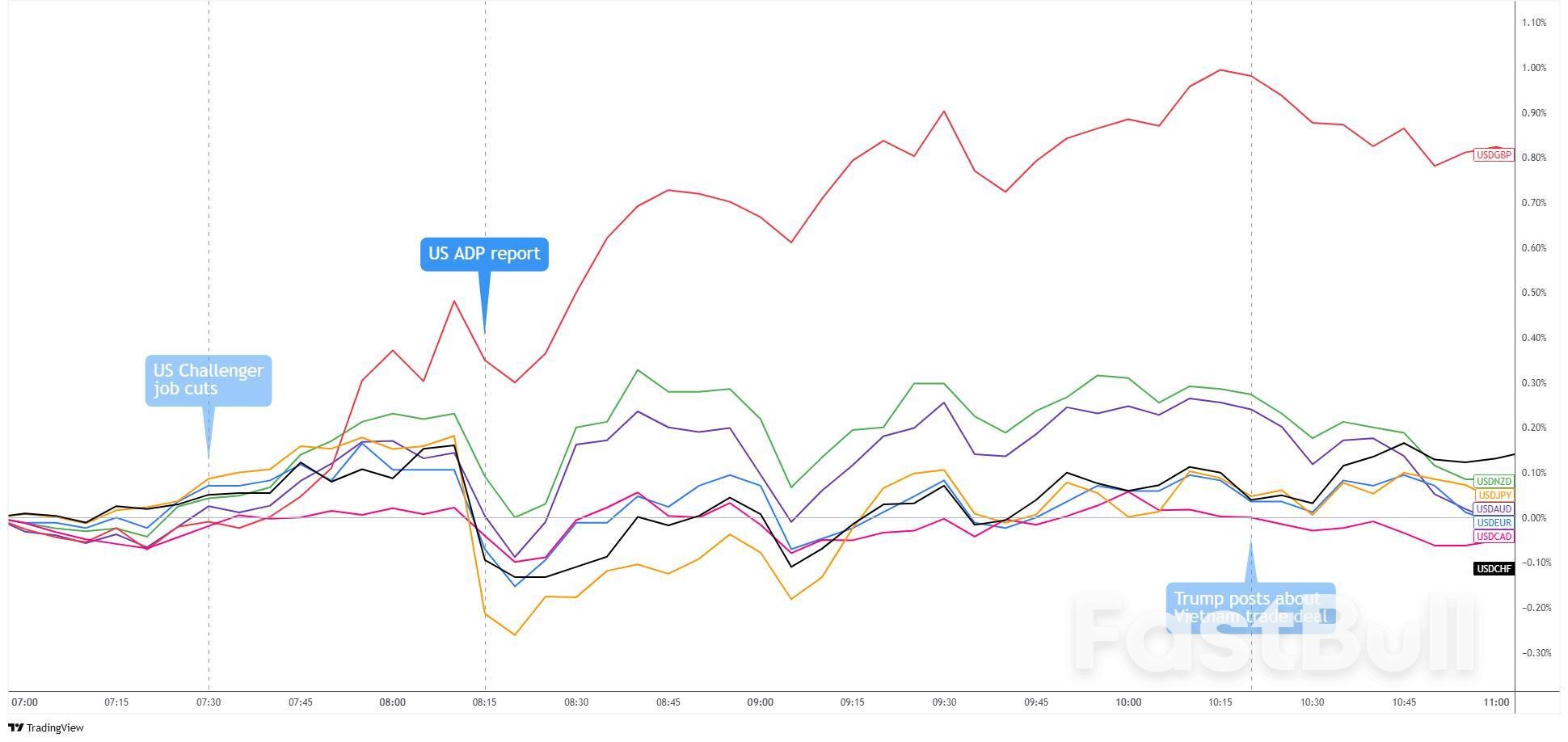

The Australian dollar dropped on a CPI miss, the Japanese Nikkei declined on weak retail data and BOJ caution, tech shares traded positively, while Hong Kong and China equities moved lower.

What happened in the Asia session?

The Australian dollar dropped on a CPI miss, the Japanese Nikkei declined on weak retail data and BOJ caution, tech shares traded positively, while Hong Kong and China equities moved lower. Defensive positioning persists ahead of the Fed and BOJ meetings, amid global trade policy uncertainty and anticipation of significant economic data and earnings releases.

Market focus remains on the near-term U.S. rate path, the sustainability of the U.S.–China tariff truce, and signs of growth stabilization or policy easing in the Asia-Pacific region. Overall, Asian markets are treading water, reacting more to policy and macro headlines than to individual data points, as risk events accumulate on the calendar and volatility could rise in the next 24–48 hours.

What does it mean for the Europe & US sessions?

Markets are entering the European and U.S. sessions with a cautious tone. The details of the U.S.–EU trade agreement are weighing on the euro and European stocks while supporting the dollar. U.S. equities are consolidating near their highs but face potential tests with the upcoming Federal Reserve decision and a wave of major earnings reports. Oil remains sensitive to global headlines, while gold stays steady as inflation and trade risks sustain demand. Traders should remain alert to significant headline risks from central banks, trade negotiations, and earnings in the coming hours.

The U.S. dollar is exhibiting a strong bullish trend today, supported by gains in trade policy, positive economic data, and increased global capital flows ahead of the upcoming Fed decision. Market participants should closely watch for any shift in the Fed’s tone, which could serve as the next key catalyst for the dollar’s direction. The U.S. Dollar Index (DXY) has extended its rally, trading above 98.8 after a 1% surge at the start of the week. This momentum positions the dollar for its strongest week of the year so far, bolstered by recent U.S. trade agreements, including a 15% tariff on EU imports, which have strengthened the U.S. economy while pressuring the euro.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

Gold is trading slightly higher early Wednesday, recovering from three-week lows as risk sentiment turns cautious and traders await clarity from the U.S. Federal Reserve meeting. For now, the yellow metal remains in a consolidation phase, with its direction hinging on upcoming policy decisions and economic headlines. Gold prices are currently around $3,327 per ounce, marking a modest 0.39% gain from the previous day. The precious metal remains within its recent range, holding above the key $3,300 support level despite ongoing market uncertainty.

Next 24 Hours Bias

Weak Bearish

The Australian Dollar remains weak and range-bound above 0.6500, with global risk sentiment, a firm US Dollar, and upcoming domestic inflation data and rate decisions shaping market tone. The outcome of Wednesday’s CPI report and the RBA’s response next week will be decisive for AUD direction in the near term. Key risks include trade headlines, signals from the Federal Reserve, and ongoing volatility in global equity and commodity markets, particularly as China–U.S. negotiations continue.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

The NZD remains weak today, driven by a stronger US dollar, uncertainty surrounding future US tariff policies, and a risk-off sentiment in global markets. With no major domestic news, the outlook depends largely on international developments and central bank signals over the next 24–48 hours.

The New Zealand dollar (NZD/USD) continued its decline, trading around 0.595–0.596 near a one-week low and extending its losing streak to a fourth consecutive session. Over the past month, the NZD has lost about 2.2% in value, reflecting broad weakness against a stronger US dollar, and it is down approximately 0.87% over the past seven days.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

The Japanese yen is trading near multi-session lows, weighed down by external trade dynamics and defensive positioning ahead of the Bank of Japan’s upcoming policy meeting. While markets expect cautious policy signals and an upward revision to the inflation forecast, any unexpected guidance or political developments could trigger volatility in both the yen and Japanese assets over the next 24–48 hours.

Currently, the yen (JPY) is hovering around 148.3–148.5 per U.S. dollar after a sharp three-session decline. The currency is down approximately 3.2% for the month but held relatively steady overnight as traders await central bank decisions and key international developments.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

Today, the euro remains under selling pressure, driven by investor disappointment over the U.S.–EU trade agreement, muted regional data, and caution ahead of the Federal Reserve’s decision. The currency is expected to stay sensitive to macroeconomic headlines and central bank policies as the session unfolds. The euro remains weak and is likely to stay volatile amid export headwinds from U.S. tariffs, a cautious ECB stance, and cooling sentiment ahead of key economic data and a major Fed announcement.

Central Bank Notes:

Next 24 Hours Bias

Medium Bearish

The Swiss franc has softened slightly as global risk sentiment improves and the U.S. dollar rebounds on trade news and Fed policy expectations. The SNB’s policy remains steady following its June rate cut, with near-term direction likely influenced by cross-asset risk trends, U.S. monetary developments, and potential renewed safe-haven demand. The franc faces competing forces, its continued safe-haven appeal versus reduced demand amid improving trade relations. While the SNB’s dovish stance and readiness to intervene highlight concerns about franc strength, recent improvements in inflation may limit the need for further aggressive easing.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

The pound remains soft and defensive heading into July 30, 2025, weighed down by slowing growth, persistent inflation, and expectations of BoE rate cuts. GBP/USD is trading near multi-month lows, while GBP/EUR saw a brief rebound but continues to hover near its 2023–2024 lows. Domestic economic weakness and strong U.S. dollar demand keep sterling under pressure.

Markets are positioned cautiously ahead of the August 7 Bank of England meeting, with at least one rate cut priced in. Focus remains on UK growth signals, particularly monthly GDP releases alongside evolving labor market data and shifts in core inflation. GBP volatility continues to track developments in global risk sentiment, U.S. dollar strength, and changes in trade policy outlook.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

The Canadian dollar enters July 30 under pressure from a strengthening U.S. dollar and ongoing trade uncertainty. With the Bank of Canada widely expected to hold interest rates steady at 2.75%, attention shifts to forward guidance and how policymakers will balance persistent inflation concerns against weak economic growth and external trade risks. Additionally, the Canadian dollar is weighed down by recent U.S. trade agreements with Japan and the EU, which have strengthened the U.S. dollar while leaving Canada without a comparable deal.

Central Bank Notes:

Next 24 Hours Bias

Medium Bearish

Oil prices maintained their recent strength on Wednesday, supported by escalating geopolitical tensions following Trump’s Russia ultimatum, optimism surrounding U.S.-EU trade agreements, and a shift in market sentiment toward bullish positioning. The market remains highly sensitive to developments related to the Russia-Ukraine deadline, Federal Reserve policy signals, and upcoming OPEC+ production decisions.

Next 24 Hours Bias

Weak Bullish

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

GBPJPY Daily Chart, July 30, 2025 – Source: TradingView

GBPJPY Daily Chart, July 30, 2025 – Source: TradingView