Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

Japan Tankan Small Manufacturing Outlook Index (Q4)

Japan Tankan Small Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)A:--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)A:--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)A:--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)

U.K. Rightmove House Price Index YoY (Dec)A:--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)

China, Mainland Industrial Output YoY (YTD) (Nov)A:--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)A:--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)A:--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)A:--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)A:--

F: --

P: --

Canada Existing Home Sales MoM (Nov)

Canada Existing Home Sales MoM (Nov)A:--

F: --

P: --

Canada National Economic Confidence IndexA:--

F: --

P: --

Canada New Housing Starts (Nov)A:--

F: --

U.S. NY Fed Manufacturing Employment Index (Dec)

U.S. NY Fed Manufacturing Employment Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)A:--

F: --

P: --

Canada Core CPI YoY (Nov)A:--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)A:--

F: --

P: --

U.S. NY Fed Manufacturing Prices Received Index (Dec)A:--

F: --

P: --

U.S. NY Fed Manufacturing New Orders Index (Dec)A:--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)A:--

F: --

P: --

Canada Core CPI MoM (Nov)A:--

F: --

P: --

Canada Trimmed CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)A:--

F: --

P: --

Canada CPI YoY (Nov)A:--

F: --

P: --

Canada CPI MoM (Nov)A:--

F: --

P: --

Canada CPI YoY (SA) (Nov)A:--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)A:--

F: --

P: --

Canada CPI MoM (SA) (Nov)A:--

F: --

P: --

Federal Reserve Board Governor Milan delivered a speech U.S. NAHB Housing Market Index (Dec)--

F: --

P: --

Australia Composite PMI Prelim (Dec)

Australia Composite PMI Prelim (Dec)--

F: --

P: --

Australia Services PMI Prelim (Dec)--

F: --

P: --

Australia Manufacturing PMI Prelim (Dec)--

F: --

P: --

Japan Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. 3-Month ILO Employment Change (Oct)--

F: --

P: --

U.K. Unemployment Claimant Count (Nov)--

F: --

P: --

U.K. Unemployment Rate (Nov)--

F: --

P: --

U.K. 3-Month ILO Unemployment Rate (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Including Bonuses) YoY (Oct)--

F: --

P: --

U.K. Average Weekly Earnings (3-Month Average, Excluding Bonuses) YoY (Oct)--

F: --

P: --

France Services PMI Prelim (Dec)

France Services PMI Prelim (Dec)--

F: --

P: --

France Composite PMI Prelim (SA) (Dec)--

F: --

P: --

France Manufacturing PMI Prelim (Dec)--

F: --

P: --

Germany Services PMI Prelim (SA) (Dec)

Germany Services PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

Germany Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Composite PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Services PMI Prelim (SA) (Dec)--

F: --

P: --

Euro Zone Manufacturing PMI Prelim (SA) (Dec)--

F: --

P: --

U.K. Services PMI Prelim (Dec)--

F: --

P: --

U.K. Manufacturing PMI Prelim (Dec)--

F: --

P: --

U.K. Composite PMI Prelim (Dec)--

F: --

P: --

Euro Zone ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Germany ZEW Current Conditions Index (Dec)--

F: --

P: --

Germany ZEW Economic Sentiment Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (Not SA) (Oct)--

F: --

P: --

Euro Zone ZEW Current Conditions Index (Dec)--

F: --

P: --

Euro Zone Trade Balance (SA) (Oct)--

F: --

P: --

U.S. Retail Sales MoM (Excl. Automobile) (SA) (Oct)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Retail sales fell 0.1% in the September quarter, a smaller drop than we expected. Retail spending remains soft, but is likely to firm over the coming months.

Retail sales fell 0.1% in the September quarter, a smaller drop than we expected. Retail spending remains soft, but is likely to firm over the coming months.

September quarter retail sales (volume of good sold): -0.1% (Prev: -1.2%)

Westpac f/c: -0.5%, Market: -0.5%

September quarter nominal retail sales: -0.7% (Prev: -1.4%)

While not quite as weak as expected, September was another soft quarter for New Zealand’s retail sector.

Nominal retail spending fell 0.7% in the September quarter, with the volume of goods purchased down 0.1% (we had expected a sharper 0.5% fall in the volume of goods sold).

Spending in the September quarter was boosted by a rise in vehicle purchases, which can be lumpy on a quarter-to-quarter basis (for instance, this month’s rise followed a sharp drop last quarter).

However, looking under the surface, the softness in New Zealanders’ spending appetites remains clear. Spending in core (excl. vehicles and fuel) categories was down 0.8% over the past three months and is down 2.8% over the past year.

Looking at the longer-term trends in the retail sector, sales have been trending down over the past year as households have wound back their spending in response to increases in living costs and high interest rates. There has been particular softness in discretionary spending areas, like purchases of household furnishings and spending in bars and restaurants.

We expect that the September quarter will be the low point for retail sales. Tax cuts were rolled out in late July. In addition, the financial headwinds that have squeezed household spending power over the past year are now easing, with inflation dropping back and interest rates falling. It will take time for the full impact of those changes to pass through to households’ back pockets. However, confidence is on the rise.

Against that backdrop, we expect to see retail spending gradually pushing higher as we go into the holiday shopping season, with a more meaningful rise expected through mid-2025.

While firmer than expected, today’s figures were broadly in line with the continued softness in economic growth that we’re forecasting in the September quarter (we’re forecasting a 0.2% fall in GDP over the quarter). We’ll take a closer look at how our forecast for GDP growth is shaping up over the next couple of weeks as additional data on September quarter activity is released.

The Reserve Bank of New Zealand will kick-start the end of year policy meetings of the major central banks when it announces its decision on Wednesday. Having stood out as being ultra-hawkish during the global tightening cycle, the RBNZ performed a major policy reversal over the summer by embarking on a loosening campaign even before the Fed had started its own.

With the annual rate of CPI falling within its 1-3% target band, inflation expectations settling around 2.0% and GDP growth remaining sluggish, policymakers have little reason to be cautious and a back-to-back 50-basis point cut is fully priced in. There is even speculation that the RBNZ might opt for a triple reduction of 75 basis points, which can be justified by the fact that, after November, policymakers won’t meet again until February.

Should the RBNZ surprise with a hefty cut, it will be difficult for the New Zealand dollar to regain its footing against the US dollar, and it could tumble to fresh 2024 lows.

The US economic agenda will get back into full gear next week as a flurry of releases are on the way before traders abandon their desks for the Thanksgiving holiday. Politics briefly eclipsed monetary policy after Donald Trump’s shock election win. But the focus is primarily back on the Fed now amid growing doubts about how many times the US central bank will be able to cut rates even before the incoming administration’s inflationary policies have seen the light of day.

Expectations of a 25-bps reduction in December currently stand at between 60% and 55% as Fed officials have turned more hawkish after a string of upbeat indicators on the economy, but more importantly, after the decline in underlying inflation stalled again.

Fed Char Powell has joined the FOMC’s hawkish camp, flagging the possibility of a pause. Hence, the likelihood of a cut will depend on how strong or weak the next inflation and jobs reports are before the December meeting.

The PCE inflation report, out on Wednesday, is up first on the schedule. Powell recently said he sees core PCE edging up from 2.7% to 2.8% in October, which would mark a setback for the Fed. The projection for headline PCE is a pickup from 2.1% to 2.3%.

Both the headline measures of PCE and CPI inflation have maintained a clearer downward path than the core readings, and if the incoming numbers do not throw this trend into question, the Fed might still have some manoeuvrability to trim rates in December.

Should the PCE price indices fail to shed any light on the Fed’s next move, investors will look to the minutes of the Fed’s November policy meeting due the same day for fresh policy insight. There will also be plenty of other data to sift through on Wednesday. Personal income and consumption will be quite important, followed by durable goods orders for October and the second estimate of Q3 GDP growth.

A day earlier, new home sales and the Conference Board’s consumer confidence gauge are likely to attract some attention too. US markets will be shut on Thursday for Thanksgiving Day and the stock market will close early on Friday, which means there will only be light trading. Nevertheless, those choosing not to make a weekend of it will have the Chicago PMI to keep them entertained.

The US dollar has been extending its post-election rally over the past week. But its gains are now looking overstretched. Any disappointing data therefore risks triggering a sharp correction.

Despite rising pessimism about the European growth outlook, ECB policymakers have been pushing back on investor expectations of a 50-bps rate cut in December. The recent jump in negotiated wages – a key metric for the ECB – and services inflation continuing to hover around 4% underline policymakers’ concerns about cutting too fast.

Markets have assigned about a 25% probability for a 50-bps move in December, which may be overstating the true odds if the latest ECB rhetoric is to be believed. This implies there’s quite a mountain to climb to push the chances for a 50-bps cut substantially higher.

Nevertheless, Friday’s flash CPI figures will be watched closely. In October, headline CPI accelerated from 1.7% to 2.0%. A further increase to 2.4% is forecast for November, which could dash hopes for a larger cut even more, potentially helping the euro to stop the recent bleeding against the greenback.

Ahead of the CPI numbers, Monday’s Ifo business survey out of Germany will be on investors’ radar amid worries about how the political uncertainty in the country is affecting business confidence.

In Australia, the latest CPI stats will also be doing the rounds. The monthly readings for October are due on Wednesday, while on Thursday, Q3 capital expenditure data will be monitored. Annual inflation fell to 2.1% in September, which is at the lower end of the RBA’s 2-3% target band. Yet, the RBA is not ready to start taking its foot off the brake, and investors don’t foresee a rate cut before May 2025 at the earliest.

If CPI edges up to 2.3% in October as expected, there might be some support for the Australian dollar versus its stronger US counterpart.

Another currency struggling to keep its head above water is the Canadian dollar. The Bank of Canada has been more aggressive than other central banks in slashing rates, and this explains why the loonie is the third worst performing major currency this year.

A fifth consecutive rate cut is likely in December but bets for a second 50-bps cut faded after the recent hotter-than-expected CPI report. Friday’s Q3 GDP print will probably not be a game changer for the BoC, but there could still be a sizeable reaction in the loonie from any big surprises.

Adding to Friday’s data barrage are the Tokyo CPI figures for November. Inflation in Tokyo fell below the Bank of Japan’s 2.0% target in October, but this hasn’t dissuaded policymakers from wanting to raise interest rates further. The question now is more about the timing. With investors split 50-50 about the possibility of a rate increase in December, stronger-than-forecast numbers could bolster bets for a year-end hike, lifting the yen.

Global Markets: The US Treasury curve flattened a bit on Friday. 2Y Treasury yields rose a couple of basis points and the yield on 10Y UST’s came down a similar amount. The 10Y yield is now 4.4%. EURUSD drifted down to the low end of 1.04 on Friday but has risen in early trading today to 1.0481. The rest of the G-10 FX pairs also show some early strength today after losing ground on Friday. USDJPY has dropped from 154.8 to 154.17 so far today. The moves are being interpreted as reflecting President-elect Trump's more measured pick of Scott Bessent as Treasury Secretary. Asian FX was mixed on Friday. The KRW lost more than half a per cent, rising to 1406, and the TWD was also soft. But there were gains for the THB and IDR. Some broader gains seem likely today. US equities made small gains on Friday, but Chinese equity markets remained very soft. The CSI 300 dropped 3.1% and the Hang Seng was down 1.89%

G7 Macro: Last week ended fairly quietly, though some stronger-than-expected US PMI figures may encourage thoughts that we get another fairly decent non-farm payroll release next week. Who knows…this number remains a lottery. Today, Germany’s Ifo survey is probably the pick of the day, and will likely confirm the weak activity that we already know about. This week’s highlight will be the US core PCE inflation figures, which will likely show that inflation continues to be stubborn, and may weigh on rate cut expectations.

China: The PBOC is scheduled to announce the medium-term lending facility rate this morning. We expect the rate to be held unchanged at 2.0% after no adjustments to the 7-day reverse repo rate so far this month.

Taiwan, China: October industrial production data will be published in the afternoon. We expect growth to moderate to 9.2% YoY after the last five months of low to mid-double-digit growth, taking into account a less supportive base effect. In recent months, the strength has been primarily driven by the Computers, Electronic & Optical Products and semiconductor categories, and while this trend is expected to continue the base effect becomes less supportive in the fourth quarter.

Singapore: October inflation data is due out at 1300 SGT today and will likely show the headline rate dropping below 2.0%, while the core rate eases a little lower from 2.8% in September. We don't expect the Monetayr Authority of Singpaore to softening inflation data until next year.

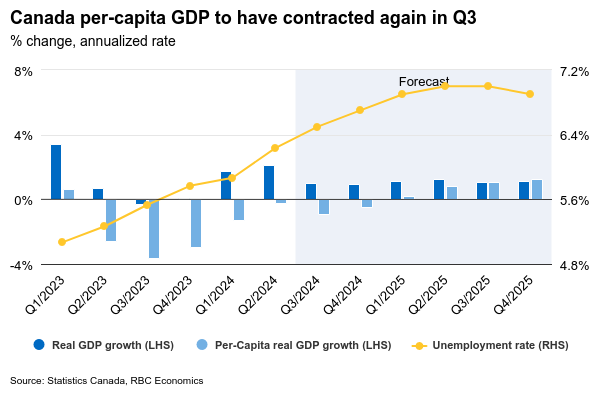

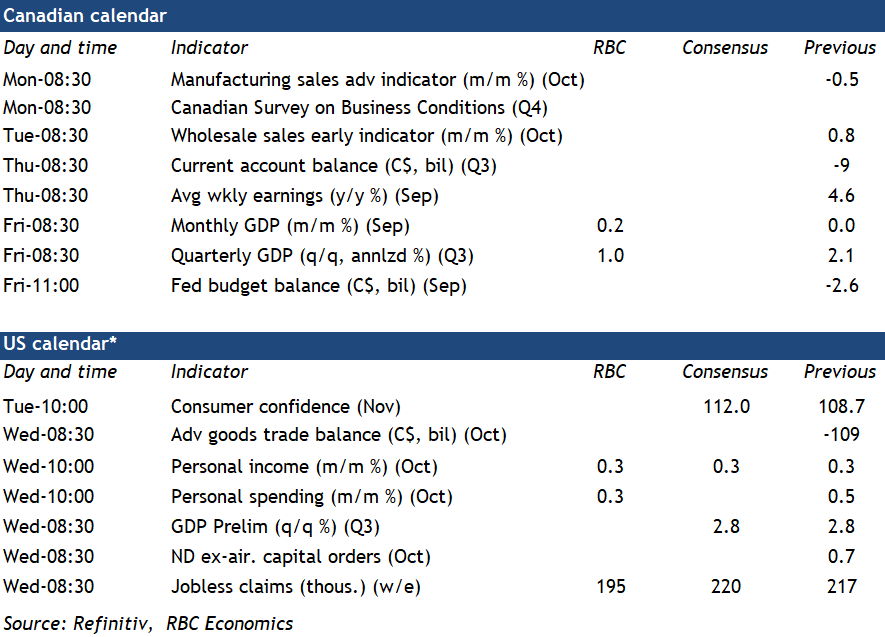

We look for gross domestic product growth in Canada to have picked up slightly to 0.2% in September on Friday after holding steady in August. That should leave the Q3 reading in line with our projection for a 1% annualized increase—slightly below the Bank of Canada’s 1.5% forecast and less than half the 2.1% rise in Q2.

Consumer spending likely increased in Q3 given a 5% (annualized rate) rise in retail sales, but a pullback in equipment imports is flagging a drop in business investment after a surprisingly large Q2 increase. A small pick-up in home resales in August and September likely drove residential investment higher in Q3, the first increase in four quarters.

The 0.2% increase we expect in September GDP is lower than Statistics Canada’s 0.3% advance estimate, with the rise partly due to the rail transportation bounce-back after disruptions in August. Wholesale and retail sale volumes rose in September, but manufacturing output likely contracted again, while hours worked fell 0.4% in September.

More importantly, the increase in Q3 GDP won’t prevent another contraction in real per-person activity, extending that downward trend for a sixth consecutive quarter. The soft growth backdrop and broadly easing inflation pressures are the main reasons our own base-case projections look for another 50 basis point rate cut from the Bank of Canada in December.

September’s GDP report will also include annual benchmark revisions with early estimates already suggesting that the level of GDP in 2023 was 1.3% higher than previously estimated. However, that is unlikely to change the broader trajectory for per-capita output, which has been persistently lower and consistent with a rising unemployment rate and slowing inflation pressures.

We expect U.S. personal spending to grow by 0.3% in October, down from the 0.5% in the prior month. Retail sales came in at 0.4% during that month, also grew at a slower pace than in September.

U.S. Personal income likely rose 0.3% in October. Disruptions from hurricanes and a large strike in the manufacturing sector paused job growth in October (+12k), but wages rose.

Job openings in the Canadian September SEPH data will be watched closely for signs of further softening in the labour market. Job openings have been declining, and we continue to expect wage growth to slow.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up