Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

We've seen a notable pick-up in Dutch manufacturing production since August this year. In October, production was significantly higher for the third consecutive month than it was for 11 months prior.

We've seen a notable pick-up in Dutch manufacturing production since August this year. In October, production was significantly higher for the third consecutive month than it was for 11 months prior.

The technology industry has played an important part in the recent growth. In both machinery production and in that of electrical appliances and means of transport, we're seeing a clear recovery emerging after a period of stagnation. Like their counterparts in the eurozone, Dutch manufacturers have become somewhat more optimistic about the near future since the summer.

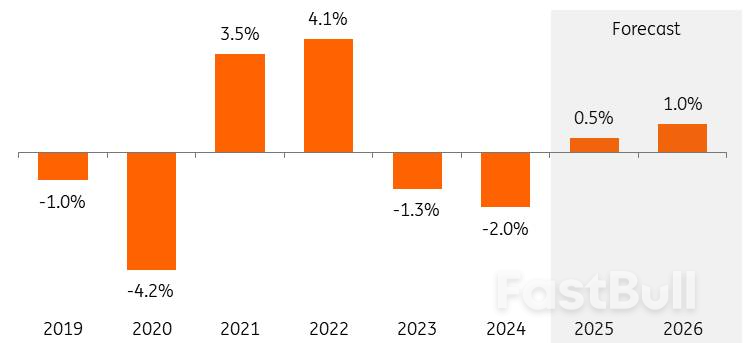

Now that the unrest around trade tariffs is also easing, production could increase further from +0.5% in 2025 to +1.0% in 2026. Still, many factors continue to slow down growth, such as export restrictions and import tariffs, stiff competition from China and structural factors like grid congestion, nitrogen emission limitations and relatively high energy costs.

Volume growth of output of Dutch manufacturing

Increasing consumer spending and additional government investment, in particular, will lead to more manufacturing orders in 2026. Although production expectations have improved and manufacturers have been receiving more new orders for some time, producers have become only slightly more positive about their order books in recent months. Getting the pipeline of customer orders well-filled again is a process that takes time.

It also takes a while for investments in defence, for example, to translate substantially into more orders and production. Expanding production takes time due to staff shortages and the required construction or conversion of factories. In turn, it isn't surprising that progress in producer confidence and the purchasing managers' index is currently stalling around the long-term average. Like the slight improvement in the orders-to-stocks ratio, sentiment indices do not yet point to substantial growth.

Industrial producers' assessment of order books and stocks of finished products*

*balance of positive-negative judgments; 2-month moving average, inventory judgment inverted (r.h.axis) Source: Statistics Netherlands, ING Research

*balance of positive-negative judgments; 2-month moving average, inventory judgment inverted (r.h.axis) Source: Statistics Netherlands, ING ResearchThe gradually increasing global demand for chip machines is yet another growth driver for Dutch manufacturing. The growth of chipmakers and equipment manufacturers remained under pressure in 2025 due to a slower-than-expected normalisation of customer inventories. While semiconductor company ASML continues to keep a close eye on this, ASM and Besi are seeing order growth recover and are optimistic about 2026.

Investors are also anticipating increasing chip machine demand in 2026. The artificial intelligence boom requires additional chips for data centres, for example, which is creating a growing need for production capacity among semiconductor producers. Demand for chips for applications other than AI, such as consumer electronics, automotive and industrial applications, is also improving.

The uncertainty surrounding the size and impact of US President Donald Trump's import tariffs has caused consumers and businesses to spend only reluctantly. As uncertainties are eased by recent trade deals, the outlook for consumption and investment is improving. Nevertheless, the uniform tariff on EU exports to the US – previously an important growth market for Dutch industry – still remains at 15%. Together with the cooling of the US economy, this will dampen export growth in 2026. The 50% rate on European products and parts made of steel and aluminium is still in place. In fact, the US is bringing more and more products with steel and aluminium parts below the high 50% tariff.

Headwinds and uncertainty also remain due to trade restrictions stemming from increasing technological rivalry with and resource dependence on China. Government policy has an increasingly large and unpredictable influence on market conditions.

Think of the intervention in Nexperia's business operations and the subsequent export restrictions of essential automotive chips by China. The restrictions on the export of advanced chip machines to China also directly affect Dutch makers and suppliers. At the same time, the persistently expensive euro against the dollar and rising competition from China, which has intensified since Trump's tariffs, are directly – and, through lower exports, indirectly – at the expense of the demand for Dutch products.

Low demand, high energy costs and cheap imports continue to hurt chemicals and base metals

Companies in the chemical and base metal sectors, in particular, will continue to face three persistent bottlenecks in 2026:

The relatively large number of eight large chemical plants (or parts thereof) that have been closed in the Netherlands this year will also have a negative impact on growth in the coming years, as part of the production (capacity) has been taken out of the market.

In that light, the current downward trend in energy prices is encouraging, but not immediately sufficient for renewed growth. This is also expected to continue in 2026, mainly due to increasing global LNG production capacity (especially in the United States and Qatar), and the gas market will structurally expand. This reduces the chance of extreme price peaks and supply problems. The high transport and processing costs of LNG do ensure that energy in Europe remains relatively expensive. LNG imports will continue to be needed for years to meet energy needs.

In addition to the increasing demand for chip machines, higher government spending on defence is also gradually increasing product demand. For example, for radars from Thales, frigates from Damen Naval and submarine parts from IHC. The €800 billion from the European Commission's ReArm-Europe programme and the new NATO standard of 3.5% of GDP will consolidate long-term investments.

An increasing amount of unused capacity is now being used for defence purposes, such as VDL's old Nedcar factory. Drone manufacturing is a fast-growing branch in which the Netherlands excels, previously for civilian purposes. More and more "dual-use companies" are responding to the new growth market by developing new military resources based on existing civilian applications.

Production growth in the food industry is set to pause in 2026 after a strong increase in 2025. Based on figures from Statistics Netherlands up to and including September, we assume production growth of at least 3% for 2025. This is partly pent-up demand after several lean years; foreign turnover is also currently growing considerably faster than domestic turnover.

In terms of production levels, the sector will come close to 2018's peak. The fact that the expected growth will fall in 2026 is mainly due to supply constraints and limited room for expansion investments. The impact of the shrinking livestock herd on the dairy and meat processing industry plays a major role in this. Still, consumer demand is developing positively, and that provides a counterbalance.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up