Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Australia's hopes for rate cuts in 2026 have dimmed after RBA Governor Michele Bullock signaled they're no longer on the table – and that a rate hike is now a real possibility.

Australia's hopes for rate cuts in 2026 have dimmed after RBA Governor Michele Bullock signaled they're no longer on the table – and that a rate hike is now a real possibility. With inflation proving stickier than expected and price pressures broadening on everything from housing to everyday essentials, markets are beginning to reprice the path for interest rates.

Here is a lightly edited transcript of the conversation:

Rebecca Jones: This week we were told by RBA Governor Michele Bullock that rate cuts were pretty much off the table and now it looks like we could instead have a rate hike by June. I don't know about you, but that wasn't exactly the festive surprise I was hoping for this week. To take us through the reasons why, and what the coming year holds for the Australian economy, I'm joined by Bloomberg's APAC economy reporter Swati Pandey from our Sydney newsroom. Swati, welcome back to the podcast.

Swati Pandey: Thank you Bec. Delighted to be here.

Jones: Swati, it was widely expected that the RBA would keep interest rates on hold at this week's meeting, which was of course the last one for 2025. That is exactly what happened. But what everyone was waiting to hear was, are we going to get another rate cut? You were at the press conference on Tuesday. What did we hear instead?

Pandey: Yes, you're right Bec, expectation was that the Reserve Bank would leave interest rates unchanged for the third straight meeting at 3.6% and there was not a lot of clarity around what the governor's press conference would bring. So it was quite surprising to a lot of people when she gave a very clear signal that other interest rate cuts are off the table. And given where the economy is tracking, given where inflation was and the upside risks to both, it looks like forget about an interest rate cut—in fact, it's an interest rate hike that we will be staring at for 2026.

Jones: And so when you heard that at the presser, you've got your phone in your hand, you start messaging your contacts. What did they tell you?

Pandey: So as soon as—that was the very first question in fact—that Governor Bullock was asked, whether they considered a cut or whether they considered a hike, and she said they did not explicitly consider a cut but they discussed the circumstances under which interest rates could go up. And then I followed that up by asking what those circumstances were that they discussed, if she could provide some more color. Following that, I started messaging some economists just trying to understand how they were reading the comments because you know when the press conference is on, everybody's watching it. By everybody I mean people who are interested in this, right? So from economists to traders, people overseas as well. And I think half of our newsroom watches it as well. And so a lot of these people kind of commented. So there's a kind of like a big bit of back and forth in messaging that also helps in understanding how people are viewing it from outside as well. And also helps shape the story, shapes the thought and the thinking that goes into writing the story after the press conference.

Jones: So the group chat went crazy because I can imagine— looking at the first part of Tuesday's event, it's the written statement from the RBA and that was pretty short, pretty sort of formulaic. But then the real surprise sort of came at the press conference. Was it a surprise to the economists that you talked to? What did they have to say?

Pandey: Yes, it did come as a surprise to people that Michele Bullock was that clear in signaling that interest rate cuts were off the table and in fact preparing the groundwork for a hike. And in fact, one of the economists I spoke with during the press conference said that the governor was laying the markers for a full pivot towards a tightening bias. There is a kind of view that it's a conditional tightening bias right now. So what that means is if we have a bad inflation report in January and the RBA has to raise interest rates in February, nobody is going to say that, oh my gosh, this came as a shock, this came as a surprise, the RBA is not communicating, this just came out of nowhere. So that criticism is unlikely to happen because like the economist from Westpac, Pat Bustamante, that I spoke with, he said that the governor was laying the markers for a full pivot to a tightening bias, right? And that was the inference a lot of people in the market and economists drew as well from her remarks. So the onus, as Su-Lin Ong from RBC told me, is on data and if inflation continues to surprise on the upside, the RBA will not hesitate to raise interest rates from here.

Jones: I wanna pick up on something that you've just mentioned and that is inflation, because I think that's where the story gets messy. Swati, we've all noticed price pressures picking up over the last couple of months. When did things get so pricey? What is actually driving inflation?

Pandey: Yeah, so the past maybe three months of inflation reports have surprised on the upside. And in fact the very latest report had broad-based price pressures. So by that I mean everything from housing costs, clothing and footwear, education and culture, eating out, buying food and groceries—everything showed a big jump in price increases. And obviously the biggest driver has been housing costs, which includes the construction cost of a new property, new development. But it also includes things like electricity. As we know, Treasurer Chalmers this week announced the end of the electricity rebate that had helped to put some downward pressure on prices, and those rebates are now going away. So we are going to get a sticker shock in the fourth quarter inflation report and maybe in the first quarter inflation report as well. The good thing is that the RBA knew that would happen.

So when they released their forecasts in November, they had already priced that in. So the RBA is expecting inflationary pressures to remain high through at least the middle of next year. If inflation is higher than their already lofty expectations, that is when we see the risk of interest rate hikes happening. If inflation is tracking around their lofty expectations, the RBA will just probably want to keep interest rates on hold. So if there's an upside shock, that is when interest rate hikes become a real possibility.

Jones: And Swati, there's a view out there that the RBA is completely done easing. And of course by easing I mean cutting interest rates. There is also running along the same track another very live debate that suggests that if inflation stays sticky—that means keeps on going up, right?—Governor Bullock may in fact have to pivot and tighten, that is raise interest rates to try and bring inflation down. And then there is another track, which is people who believe that one or two cuts are still plausible in 2026. What does the data suggest is most likely at this point in time?

Pandey: That is a very complicated question only because the answer to that is not easy. So we are in an economy where productivity growth is very low and what that has done is it has brought down our potential rate of growth. So when during the mining boom Australia's economy, let's say, was growing at 4%, it was able to grow at that pace without really sparking inflationary pressures, right? Now, if the economy grows at let's say 2.5%, there is fear that it may spark inflationary pressures only because the potential for it to grow without sparking inflation has reduced because of lower productivity growth. And that is where this discrepancy arises between how economists are looking at this.

Some economists are saying that the supply constraints that we have seen in our economy—which have led to higher housing construction costs, for example, it's very hard to find tradies and likewise— I mean the economy has not been able to supply enough to meet the demand that there is. Some economists believe that this supply-demand conundrum will be resolved eventually or soon enough. Those who believe that feel that the RBA will not end up raising interest rates. Either the way it'll resolve is that demand will come down, the labour market would slow. We are already seeing signs of slowness in the labour market. We are hearing about companies laying off employees, unfortunately. We are seeing more increase in the unemployment rate. So some economists believe that that would be enough to cool demand.

Others believe that inflation will remain a concern—housing costs will be sticky or elevated and people will continue to spend on eating out, going to concerts and stuff like that. So these are the people who believe that the RBA may then have to increase interest rates next year. And then there are some people who feel that things are going to kind of wobble along, which would suggest that the current interest rate setting—where interest rate is at 3.6%—is fine. So you don't touch it, you don't do anything, just keep watching data.

Economists, the median in our Bloomberg survey, are expecting no change at all in fact. So they're expecting interest rates will remain at 3.6% through 2026. There are only a handful of economists who are predicting an interest rate hike and only a handful who are predicting a cut. So the majority is still sitting on no change.

Jones: It is such a complicated recipe to get right. And as you described, three very distinct schools of thought around what's going to happen next year. Swati, I want to talk to you a little bit now about a topic that makes Australians collectively inhale—you can guess—it's housing. Mortgage stress is rising, APRA is tightening lending standards and yet prices are still marching higher. We're sort of getting to the tail end of the so-called spring selling season right now. Swati, how big a risk is the housing market heading into next year?

Pandey: One of the biggest problems with Australia's housing market is the lack of supply and we are not seeing that being resolved very quickly. In fact, it takes forever to build a house in Australia and you would know that when you're trying to get renovations done—it's very hard to find tradies and then even when you find them, it's very hard for them to stick with their timelines. Either it's difficult to get the right supply, it's difficult to get the right people, but whatever it is, it takes longer and that is what the country is facing in general. We are much behind our timelines to build enough housing to meet the growing demand of our people.

As long as that remains the case, housing prices are going to be elevated or rise. In fact, in some markets like Sydney, for example, affordability constraints mean that house price growth is not as rapid as it is in some other places like Adelaide or Brisbane or even Perth. Perth in fact is seeing a big boom in housing prices and there's big demand as well in Western Australia. So yes, it is a concern for people who want to buy a house, but it is also a concern for the Reserve Bank because housing costs are a big part of the inflation basket. If we are not able to bring that cost down, it would keep inflation sticky, which means elevated.

Jones: Let's zoom out a little bit now. The Federal Reserve in the US cut rates this week and that was widely expected. Swati, how does Australia's trajectory compare with the US right now?

Pandey: So in the past, Australia and most countries used to follow what the Fed would do, but that's not the case anymore. For example, the RBA started cutting rates much later than the Fed in this current cycle. Australia has only cut by 75 basis points. The Fed has cut by more. The RBA left interest rates unchanged this week for the third straight meeting and the Fed has cut for the third straight time. So they are completely diverging. The Fed is still cutting and the RBA is on hold but is signaling that the next move will not be a cut but a hike. They don't want to act too quick, too fast, which is why the bar to raise interest rates next year is very high as well. A key thing to watch out for is the inflation report for the December quarter, which will come out at the end of January. That is actually going to be really critical in deciding what the RBA does in February and the year ahead.

Jones: So there might be a few economists recalled back a little early from their summer holidays here in Australia. So Swati, let me get this straight. We've got inflation that won't go quietly, an RBA that may not be finished moving, a housing market that is continuing to defy both gravity and policy, plus a Fed that's cutting where we stay put. It's a really complex picture, isn't it? But very fascinating as we head towards 2026. I want to finally ask you about something completely different and that is AI and how that relates to Australia's economic prosperity. There is a view that 2026 could be the year that AI starts to show up in the real economy—in earnings, in efficiencies, in growth. We saw just last week how heavily the government is supporting the OpenAI–NextDC link-up. Is AI genuinely a bright spot for Australia or is the hype still running ahead of reality?

Pandey: Look, Michele Bullock was asked this question at the press conference on Tuesday and her response was that the data centres are being fitted—they're not being constructed here. So you are importing the required machinery from overseas and then you're getting them fitted here. You obviously need people to set them up, but then how many people would you employ in data centres, right? Is it a very labour-intensive industry? Maybe not. So for now, with the investments that we are seeing, it is a good thing and AI investments are expected to lead to greater productivity benefits as well. So from that point, it's good too.

One thing that Governor Bullock did not address, and I think it's something to watch out for, is the renewable energy transition, which may happen finally for Australia as a result of this, because data centres are extremely energy intensive and they are very water intensive as well. Australia has been trying forever to do this transition from basically coal to renewable—so whether it's solar or wind. If we start seeing these data centre investments spur huge demand for energy, then that will probably lead to that renewable transition that we have all been waiting for and that is going to have a huge impact for the economy and even in terms of productivity. So that is something that I would say we should watch out for and something to end the podcast on a positive note as well.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

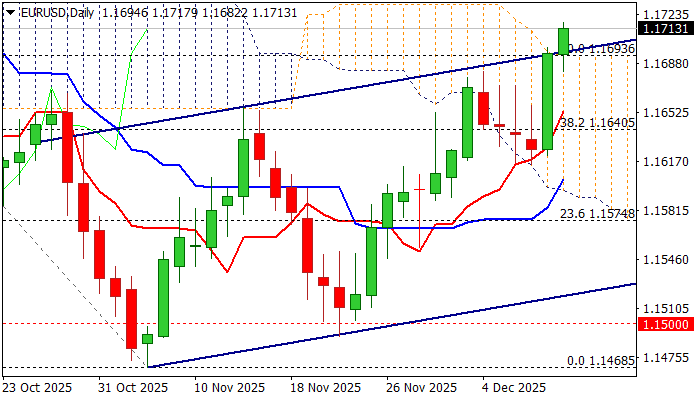

Fig. 1: Percentage of Nasdaq 100 component stocks trading above 20-day & 50-day moving averages as of 10 Dec 2025

Fig. 1: Percentage of Nasdaq 100 component stocks trading above 20-day & 50-day moving averages as of 10 Dec 2025 Fig. 2: US Nasdaq 100 CFD Index medium-term trend as of 11 Dec 2025

Fig. 2: US Nasdaq 100 CFD Index medium-term trend as of 11 Dec 2025