Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

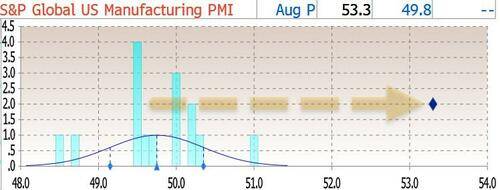

One month after unexpectedly sliding into contraction for the first time in 2025, moments ago the S&P Manufaturing PMI even more unexpectedly soared from 49.8 to 53.3, not only smashing expectations of another decline to 49.7 and printing well above the highest economist forecast and in fact printing 7-sigma above the median estimate...

One month after unexpectedly sliding into contraction for the first time in 2025, moments ago the S&P Manufaturing PMI even more unexpectedly soared from 49.8 to 53.3, not only smashing expectations of another decline to 49.7 and printing well above the highest economist forecast and in fact printing 7-sigma above the median estimate...

... but was the highest print since May 2022! According to S&P's PMI report, the surge signaled "a renewed improvement of factory business conditions after a brief deterioration in July."

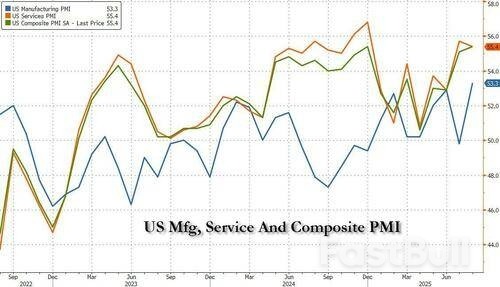

At the same time the S&P Services PMI declined from last month's red hot 55.7 to 55.4, but still beat estimates of 54.2. As a result, the composite PMI of US business activity grew at the fastest rate recorded so far this year in August, rising to 55.4 from 55.1, matching the previous post-covid high from Dec 2024 and adding to signs of a strong third quarter. Output has now grown continually for 31 months, with the latest two months seeing the strongest back-to-back expansions since the spring of 2022.

According to the report, growth was seen across both manufacturing and service sectors of the economy. Hiring also picked up. Most notably, job creation reached one of the highest rates seen over the past three years as companies reported the largest build-up in uncompleted work since May 2022.

There was more good news when it comes to jobs: employment rose for a sixth successive month, with the pace of job creation hitting the highest since January (and one of the strongest rates seen for over three years). Service providers took on staff at the fastest pace for seven months while factory job gains reached the highest since March 2022. Companies largely took on additional staff in response to rising backlogs of work. Uncompleted orders rose for a fifth consecutive month, rising in August at a pace unsurpassed since May 2022 reflecting stronger demand and near-term capacity constraints at some companies.

There were some concerns on the price side, with tariffs reported as the key driver of further cost increases in August. Companies across both manufacturing and service sectors collectively reported the steepest rise in input prices since May and the second-largest increase since January 2023. Rates of increase accelerated in both sectors. While the manufacturing cost rise was especially large, being the second-steepest since August 2022, the service sector increase was the second-highest since June 2023. Average prices charged for goods and services rose at the sharpest rate since August 2022 as firms passed higher costs on to customers. Although goods price inflation cooled slightly for a second month in a row, it remained among the highest seen over the past three years. Service sector price inflation meanwhile was the sharpest since August 2022.

Business confidence in the outlook also improved but remained much weaker than seen at the start of the year as companies reported ongoing concerns over the impact of government policies, especially in relation to tariffs. Tariffs were again widely cited as the principal cause of sharply higher costs, which in turn fed through to the steepest rise in average selling prices recorded over the past three years.

Commenting on the report, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said that the "strong flash PMI reading for August adds to signs that US businesses have enjoyed a strong third quarter so far. The data are consistent with the economy expanding at a 2.5% annualized rate, up from the average 1.3% expansion seen over the first two quarters of the year."

“Companies across both manufacturing and services are reporting stronger demand conditions, but are struggling to meet sales growth, causing backlogs of work to rise at a pace not seen since the pandemic-related capacity constraints recorded in early 2022. Stock building of finished goods has also risen at a survey record pace, linked in part to worries over future supply conditions."

“While this upturn in demand has fueled a surge in hiring, it has also bolstered firms’ pricing power. Companies have consequently passed tariff-related cost increases through to customers in increasing numbers, indicating that inflation pressures are now at their highest for three years."

As a result, the economist concludes that the "rise in selling prices for goods and services suggests that consumer price inflation will rise further above the Fed’s 2% target in the coming months. Indeed, combined with the upturn in business activity and hiring, the rise in prices signaled by the survey puts the PMI data more into rate hiking, rather than cutting, territory according to the historical relationship between these economic indicators and FOMC policy changes.”

In other words, the report coming unexpectedly strong, may be just an attempt by the traditionally anti-Trumpian S&P to pressure the Fed into maintaining a hawkish bias even as the labor market - at least as measured by most other 3rd parties - continues to deteriorate.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up