Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.S. Personal Income MoM (Sept)

U.S. Personal Income MoM (Sept)A:--

F: --

P: --

U.S. PCE Price Index YoY (SA) (Sept)A:--

F: --

P: --

U.S. PCE Price Index MoM (Sept)A:--

F: --

P: --

U.S. Personal Outlays MoM (SA) (Sept)A:--

F: --

P: --

U.S. Core PCE Price Index MoM (Sept)A:--

F: --

P: --

U.S. Core PCE Price Index YoY (Sept)A:--

F: --

P: --

U.S. UMich 5-Year-Ahead Inflation Expectations Prelim YoY (Dec)A:--

F: --

P: --

U.S. Real Personal Consumption Expenditures MoM (Sept)A:--

F: --

P: --

U.S. UMich Current Economic Conditions Index Prelim (Dec)A:--

F: --

P: --

U.S. UMich Consumer Sentiment Index Prelim (Dec)A:--

F: --

P: --

U.S. UMich 1-Year-Ahead Inflation Expectations Prelim (Dec)A:--

F: --

P: --

U.S. UMich Consumer Expectations Index Prelim (Dec)A:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

U.S. Unit Labor Cost Prelim (SA) (Q3)--

F: --

P: --

U.S. Consumer Credit (SA) (Oct)A:--

F: --

P: --

China, Mainland Foreign Exchange Reserves (Nov)

China, Mainland Foreign Exchange Reserves (Nov)A:--

F: --

P: --

Japan Wages MoM (Oct)

Japan Wages MoM (Oct)A:--

F: --

P: --

Japan Trade Balance (Oct)A:--

F: --

P: --

Japan Nominal GDP Revised QoQ (Q3)A:--

F: --

P: --

Japan Trade Balance (Customs Data) (SA) (Oct)A:--

F: --

P: --

Japan GDP Annualized QoQ Revised (Q3)A:--

F: --

China, Mainland Exports YoY (CNH) (Nov)A:--

F: --

P: --

China, Mainland Trade Balance (USD) (Nov)A:--

F: --

P: --

China, Mainland Imports YoY (CNH) (Nov)A:--

F: --

P: --

China, Mainland Exports (Nov)A:--

F: --

P: --

China, Mainland Imports (CNH) (Nov)A:--

F: --

P: --

China, Mainland Trade Balance (CNH) (Nov)A:--

F: --

P: --

China, Mainland Imports YoY (USD) (Nov)A:--

F: --

P: --

China, Mainland Exports YoY (USD) (Nov)A:--

F: --

P: --

Germany Industrial Output MoM (SA) (Oct)

Germany Industrial Output MoM (SA) (Oct)--

F: --

P: --

Euro Zone Sentix Investor Confidence Index (Dec)

Euro Zone Sentix Investor Confidence Index (Dec)--

F: --

P: --

Canada Leading Index MoM (Nov)

Canada Leading Index MoM (Nov)--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

U.S. Dallas Fed PCE Price Index YoY (Sept)--

F: --

P: --

China, Mainland Trade Balance (USD) (Nov)--

F: --

P: --

U.S. 3-Year Note Auction Yield--

F: --

P: --

U.K. BRC Overall Retail Sales YoY (Nov)

U.K. BRC Overall Retail Sales YoY (Nov)--

F: --

P: --

U.K. BRC Like-For-Like Retail Sales YoY (Nov)--

F: --

P: --

Australia Overnight (Borrowing) Key Rate

Australia Overnight (Borrowing) Key Rate--

F: --

P: --

RBA Rate Statement RBA Press Conference Germany Exports MoM (SA) (Oct)--

F: --

P: --

U.S. NFIB Small Business Optimism Index (SA) (Nov)--

F: --

P: --

Mexico Core CPI YoY (Nov)

Mexico Core CPI YoY (Nov)--

F: --

P: --

Mexico 12-Month Inflation (CPI) (Nov)--

F: --

P: --

Mexico PPI YoY (Nov)--

F: --

P: --

Mexico CPI YoY (Nov)--

F: --

P: --

U.S. Weekly Redbook Index YoY--

F: --

P: --

U.S. JOLTS Job Openings (SA) (Oct)--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)--

F: --

P: --

U.S. EIA Short-Term Crude Production Forecast For The Next Year (Dec)--

F: --

P: --

U.S. EIA Short-Term Crude Production Forecast For The Year (Dec)--

F: --

P: --

U.S. EIA Natural Gas Production Forecast For The Next Year (Dec)--

F: --

P: --

EIA Monthly Short-Term Energy Outlook U.S. 10-Year Note Auction Avg. Yield--

F: --

P: --

U.S. API Weekly Cushing Crude Oil Stocks--

F: --

P: --

U.S. API Weekly Crude Oil Stocks--

F: --

P: --

U.S. API Weekly Refined Oil Stocks--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Within the global trend, the US 30 index has declined, leading to a shift towards a downward trajectory. The US 30 forecast for today is negative.

Within the global trend, the US 30 index has declined, leading to a shift towards a downward trajectory. The US 30 forecast for today is negative.

US 30 forecast: key trading points

Speaking at the National Association for Business Economics conference in Philadelphia, Federal Reserve Chairman Jerome Powell discussed in detail the current stage of quantitative tightening. Although he did not specify when the program might end, Powell noted that there are signs the Fed is nearing its target level of adequate reserves available to banks. While balance sheet management may appear to be a technical issue, it plays an important role for financial markets.

When financial conditions tighten, the Fed aims to maintain ample reserves so that banks can access liquidity and support the economy. As conditions evolve, the central bank targets a sufficient – rather than excessive – level of reserves to prevent surplus capital in the system. During the COVID-19 pandemic, the Federal Reserve significantly expanded its balance sheet through large-scale purchases of US Treasury and mortgage-backed securities, pushing it close to 9 trillion USD.

The US 30 index continues to fall within a downtrend. The resistance level has formed at 46,880.0, while support lies at 45,450.0. At this stage, it is difficult to assess how long the current trend might last. A breakout above the current resistance level would signal a potential resumption of upward movement.

The US 30 price forecast considers the following scenarios:

Jerome Powell noted signs of gradually tightening liquidity conditions, suggesting that further reserve reductions could hinder growth. The US 30 stock index has been in a downtrend since late last week. Only developments related to the US-China trade conflict are likely to reverse this trend, while economic data remains unavailable due to the government shutdown. The next downside target for the index could be 46,880.0.

When an incursion of Russian drones forced Warsaw airport to shut down last month, Poland immediately shot them down. When unidentified drones forced Munich airport to suspend operations this month, German authorities provided snacks for stranded passengers while police helicopters monitored the air space. As strange as it may sound, Germany’s military isn’t allowed to defend German airspace against anything short of a full-scale invasion. It’s just one roadblock of many in the way of making Germany fighting fit.

On paper, Berlin has a free pass to strengthen national defense. With military spending above 1% gross domestic product exempted from borrowing restrictions, there is effectively no limit on funding of the military, known as the Bundeswehr. But as the drone dilemma indicates, Germany faces more daunting obstacles to defending itself as the neighborhood gets increasingly dangerous.

For one, the constitution, written after World War II, strictly limits the military’s role inside the country, even banning it from shooting down flying objects such as drones anywhere in domestic airspace that isn’t above a military base. This rule was meant to prevent the kind of military overreach seen during authoritarian times, especially under the Nazi regime. Today, these restrictions make it hard to respond to modern threats.

Germany could of course change the legislation, but this is where its deeply fragmented political landscape comes into play. For the first time in post-war history, Germany’s moderate parties don’t command a two-thirds majority in parliament, which is necessary to change constitutionally enshrined rules like the one in question. The far-right AfD and the far-left Die Linke together take up over a third of the seats. The ruling conservatives have a party resolution in place not to negotiate with either.

Even if Chancellor Friedrich Merz talked to all political parties freely to find a two-thirds majority to change the rules, it’s unlikely that he’d find one. His coalition partners, the center-left Social Democrats (SPD), have a vocal pacifist wing and the Green Party has its roots in the peace movements of the 1970s and 1980s. When Merz’s Interior Minister Alexander Dobrindt recently suggested finding a way to use the Bundeswehr against drone attacks, representatives of both parties rejected the idea outright.

With the head of the foreign intelligence service, Martin Jaeger, warning this week that “a frosty peace” in Europe “could turn into hot confrontation here and there at any moment,” it seems impossible for Merz to find a political consensus to defend German airspace.But his problems run deeper than that. Many Germans themselves harbor a profound mistrust of state power and public institutions. The Bundeswehr itself has remained popular, with around three-quarters of people saying in polls that they trust it as an institution. But belief in the politicians that would direct its actions has reached a nadir, with one recent survey suggesting that only 17% trust their democratically elected government.

The far-right AfD, now neck-and-neck with the ruling conservatives in the polls, embodies this dilemma. On the one hand, the party program demands more funding for the Bundeswehr and a reintroduction of a compulsory military service to “secure Germany’s defense capability.” On the other, many of its politicians, especially in the former East Germany, openly question if a boosted Bundeswehr would be used “in the German interest,” as the AfD leader in the state of Brandenburg, Christoph Berndt, told the media recently.

Surprisingly for a party that claims to have the national interest at heart, some AfD representatives wouldn’t even be willing to fight for their country in case of an outright attack. A young regional MP, Felix Teichner, told a German journalist last year: “One thing is clear: if this country is attacked, no matter by whom, I will grab my children and go as far away as possible.”He is not alone with this view. A recent survey found that only 16% of Germans would “definitely” defend the country with arms. That’s despite the fact that over a quarter of people thought it likely that Germany would be attacked militarily within the next five years. It’s hardly surprising that the political class can’t find a consensus when society shares their deeply entrenched reluctance to build German defense readiness.

Germany’s grappling with the question of how to defend its airspace from drone incursions is the tip of a giant iceberg of problems when it comes to rearmament and defense readiness. A deeply divided country with increasingly messy politics, it is far from mounting the kind of collective resolve necessary to build an effective military ethos. It’s a conundrum that afflicts much of the West to varying degrees. But Germany’s exceptional fiscal power, combined with its particular past and present, creates a unique paradox: Germany is an economic giant that is astonishingly hard to defend.

New York state factory activity unexpectedly expanded and the outlook climbed to the highest since the start of the year despite lingering price pressures.

The Federal Reserve Bank of New York’s October general business conditions index increased 19.4 points to 10.7 as orders and shipments picked up, figures issued Wednesday showed. Readings above zero indicate expansion.

The figure, which is prone to wide swings on a monthly basis, exceeded all estimates in a Bloomberg survey of economists.

A gauge of the outlook over the next six months more than doubled to 30.3, reflecting greater optimism about orders and shipments. Some producers stand to benefit from more favorable tax policy and business investment such as artificial intelligence.

Manufacturing across a variety of sectors has struggled to build momentum as higher US import duties raise costs of materials and introduce supply-chain challenges. The Fed’s report showed a gauge of prices paid for materials rose, while a measure of prices received by state manufacturers increased to a six-month high.

The state’s producers expect more inflation in coming months. The outlook for prices paid climbed to one of the highest readings since 2022.

Economists and policymakers will be relying more on reports such as those from the regional Fed banks for clues on the economy in the absence of official data because of the US government shutdown. The Fed announced last week that it has delayed the September industrial production report.

In addition to growth in orders and shipments, a gauge of factory employment showed the fastest expansion in three months.

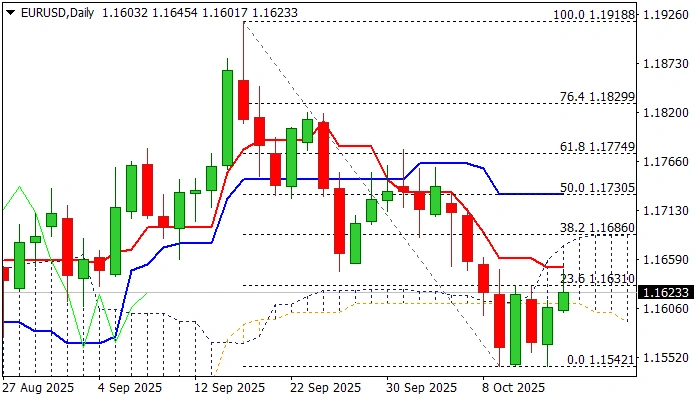

The Euro edged higher on Wednesday morning, underpinned by weaker dollar on the latest remarks from Fed chief Powell which markets saw as more dovish and contributing to strong expectations for two rate cuts by the end of the year.

Fresh gains penetrated daily cloud (spanned between 1.1610 and 1.1686) and attempt to break above recent congestion (top lays at 1.1650 and is reinforced by daily Tenkan-sen), which acts as solid resistance and caps recovery so far.

Break of 1.1650 is seen as minimum requirement to keep recovery in play, with lift above daily cloud top (1.1680. also Fibo 38.2% of 1.1918/1.1542) to confirm signal and open way for further gains towards 1.1730 (daily Kijun-sen / 50% retracement) and 1.1774 (Fibo 61.8% / Oct 1 lower top) in extension.

However, predominantly bearish structure of daily technical studies warns of potential recovery stall, with slight bullish bias expected while the price stays above cloud base, but fresh negative signal to be expected in case on repeated daily close below daily cloud.

Res: 1.1650; 1.1686; 1.1700; 1.1730.

Sup: 1.1610; 1.1596; 1.1574; 1.1542.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up