Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

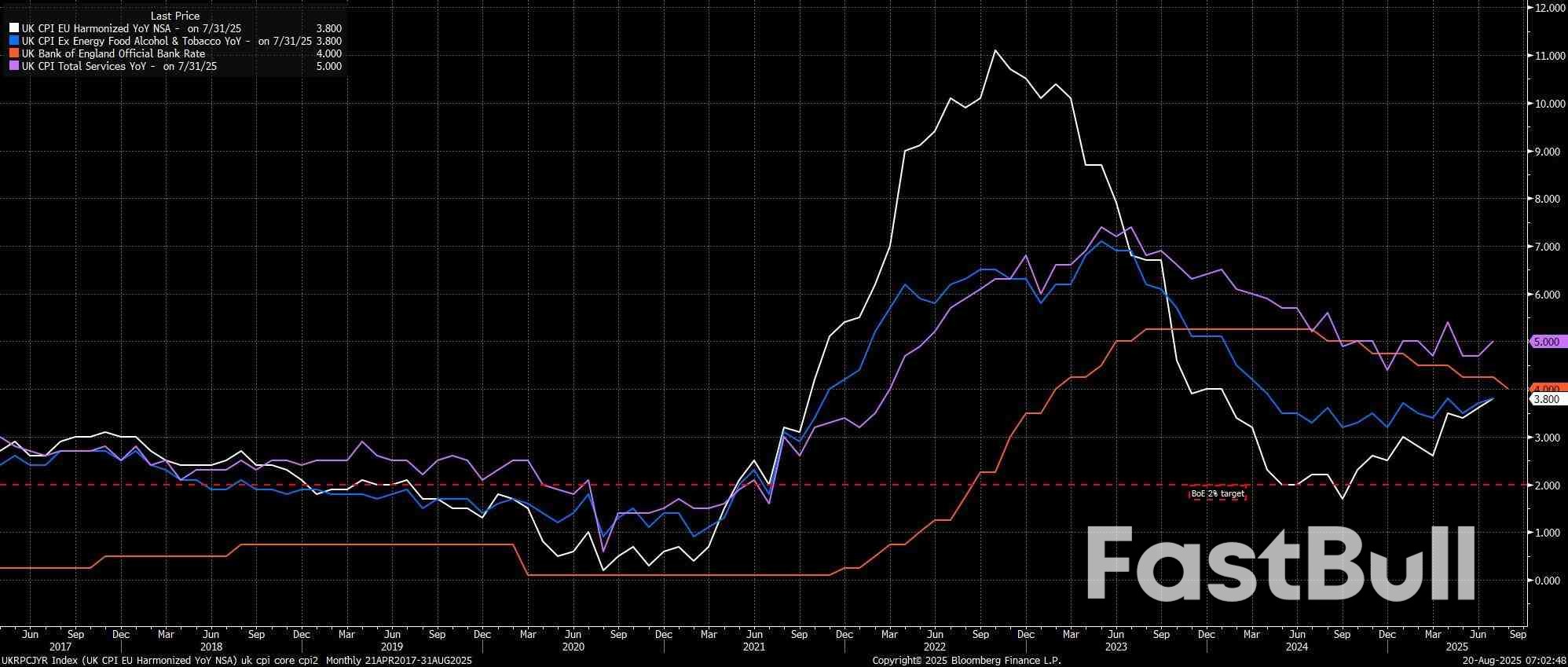

Headline CPI rose 3.8% YoY in July, the fastest pace since January last year, albeit in line with the Bank of England's latest forecasts. Those same BoE forecasts, however, foresee a further rise in inflation in the months ahead, with CPI set to peak at 4.0% YoY in September, double the MPC's target.

Headline CPI rose 3.8% YoY in July, the fastest pace since January last year, albeit in line with the Bank of England's latest forecasts. Those same BoE forecasts, however, foresee a further rise in inflation in the months ahead, with CPI set to peak at 4.0% YoY in September, double the MPC's target.

Measures of underlying inflation also pointed to price pressures having remained intense, and incompatible with the Bank's 2% inflation aim. Core CPI, excluding food and energy, rose 3.8% YoY last month, the fastest pace since April, while the closely-watched services CPI metric rose 5.0% on an annual basis, also the highest level since April, and above the Bank's 4.9% YoY forecast.

Overall, the rise in headline prices came largely as a result of yet another chunky rise in food prices, but also by virtue of an upward impulse from consumer energy costs, with the Ofgem price cap this year seeing a much smaller drop than in July 2024, and as a result of the largest July increase in airfares since the start of the millennium. However, these one-off factors do little to allay concerns over those aforementioned underlying metrics remaining at elevated levels, though there may be some upwards skew in certain sections of the services metric, in particular, owing to the sampling having fallen in the middle of a number of major concert tours this summer.

Frankly, though, none of this is likely to move the needle especially much for the Bank of England, with the MPC having voted in favour of a 25bp Bank Rate cut a fortnight ago, by the narrowest possible 5-4 majority.

Today's figures are unlikely enough to persuade those 4 'hawks' that the risks of price pressures becoming embedded within the economy are subsiding in material fashion, though the next 'live' MPC meeting is now not until November, with the September meeting set to see Bank Rate held steady.

With the MPC having retained their guidance around a 'gradual and careful' pace of easing, my base case remains that a cut will be delivered at that November confab, given the continued preference for a regular, quarterly pace of cuts if possible. That said, the bar for further policy easing is clearly now considerably higher than it was mere weeks ago, while there also remains a long way to run until that November decision, especially with the autumn Budget, and likely sizeable fiscal tightening, in the mix during this period as well.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up