Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Markets continue to print record highs, and with them, investor uncertainty.Some worry that valuations have run too far. Others fear missing out on the next leg higher. And somewhere in between are those asking, “Should I wait for a correction before putting money to work?”It’s a fair question, but history suggests it’s the wrong one.

Key points:

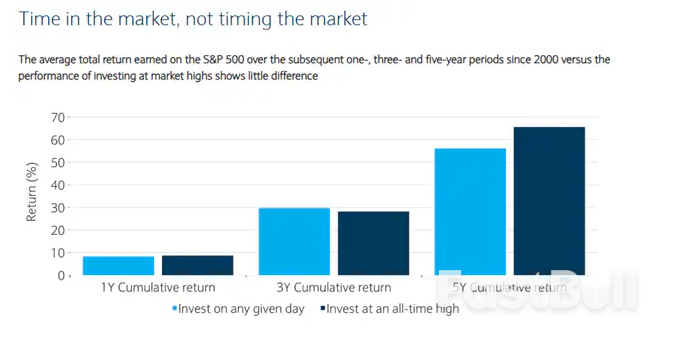

The myth of waiting for the perfect entryIn theory, “buy low, sell high” sounds perfect. In practice, most investors struggle to do either.In fact, if you only invested on days when the S&P 500 hit an all-time high, your long-term returns would often be higher than if you invested on any random day.

That’s because record highs typically happen during bull markets, and bull markets tend to last longer than expected.The real challenge isn’t timing the market. It’s having a strategy that works when prices feel high, and sticking to it.

What to do instead: smart moves at market highs

Even when the overall market is rising, individual stocks and sectors often face short-term dips. Those can be opportunities.

What you can do:

While technology and AI stocks have led the charge, many parts of the market have lagged, and may offer better value and catch-up potential if the rally broadens out.

What to consider:

Market leadership today is shaped less by geography or sector, and more by macro forces like interest rates, trade policies, and geopolitical risk. Traditional diversification alone may not be enough. It’s time to think about how different parts of your portfolio respond to shifting policy and economic drivers.

How to position:

Even if some of these areas have gained attention recently, their relevance over the long term means they may still be underrepresented in many portfolios.

Waiting for the “perfect moment” to invest often leads to missed opportunities. Even when markets dip, fear and uncertainty can prevent action, leaving cash on the sidelines and long-term goals unmet.

What works better:

Buying at market highs can feel uncomfortable, but history shows that long-term investors are often rewarded for staying the course.If you diversify smartly, lean into underappreciated areas, and stay consistent with your investing plan, you won’t need to worry about whether you’re “too late.”Because long-term wealth isn’t built by picking the perfect moment.It’s built by showing up, again and again.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

BTC and ETH had a drawdown mostly driven by long liquidations, ahead of the monthly options expiry. | Source: CoingGlass.

BTC and ETH had a drawdown mostly driven by long liquidations, ahead of the monthly options expiry. | Source: CoingGlass.