Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The US dollar trades at its weakest levels since late July ahead of Thursday’s CPI data. US treasury yields have already done some heavy lifting for USD bears, but apparently more needed to take the greenback to new cycle lows.

US dollar at the brink – but shouldn’t it already be lower still?The US dollar has weakened since last Thursday, with Friday’s weak August US jobs report sparking most of the move, as expectations for a 25-basis point cut at next week’s FOMC meeting firmed up and the odds of a 50-basis point cut, if still low, are rising. Thursday’s US August CPI print is the next event risk of note ahead of the FOMC meeting next Wednesday. The combination of lower treasury yields all along the US yield curve and at least stable risk sentiment should be the sweet spot for a weaker US dollar. But the recent focus on the very long end of global yield curves and whether further stress would prompt a policy response – seen needed first in Japan and the UK and even in France, has likely kept some residual safe haven bid in the US dollar that is offsetting much of the negative pressure on the currency. That’s a working theory, at least. For now, while the US bears are in control and the US dollar looks on the technical brink, visibility is poor unless we get a significant bid into global long bonds outside of the US – a bit more color on USDJPY in the look at the chart below.

The French Prime Minister Bayrou lost yesterday’s confidence vote in the National Assembly by a resounding margin, as widely expected, and President Macron looks set to appoint the fifth prime minister in two years, as he is seemingly running short of appropriate candidates for the unthankful position. Germany-France 10-year yield spreads have blown wider in early trading today to absorb the news, but are only a few basis points beyond the recent highs, currently at 82 basis points as of this writing, only about a single basis point higher than the highest daily close of the cycle from late August. France’s debt mountain remains a structural issue, but does it fade to a slow burn rather than sparking any imminent further uncertainty?

Chart: USDJPYTraditionally, the recent collapse in US 10-year yields would have driven a sharp sell-off in USDJPY, but the recent stress in bond yields at the longest end of the Japanese yield curve (the benchmark 30-year JGB hit all-time highs within the last week and is still only a few basis points below those highs, contrasting with the benchmark US 30-year yield, which has tumbled over 30 basis points from recent highs in the last few trading sessions). That tension of the divergence in well tamed US yields versus Japan’s long yields still suggesting uncomfortable pressure on the longest JGBs (in part also on political turmoil in Japan as the PM is resigning and the opposition is clamoring for more welfare spending) keeps the “normal” signals of lower US yields from driving the USD lower here. Technically, we are none the wiser here in either direction until we close south of perhaps 146.20 or above 149.15.

Source: Saxo

Source: SaxoLooking aheadAgain, we have the US August CPI data up tomorrow, with a benign figure likely to raise expectations for a 50-basis point rate cut next week from the FOMC. The technical situation for the US dollar looks pivotal here and possibly ready for a breakdown, with the only reservation that we have already seen so much that could have already driven the US dollar weaker still. AUDUSD is one of the closest USD pairs to a breakout – trading as high as 0.6615 today versus the high for the year at 0.6625 from back in July.

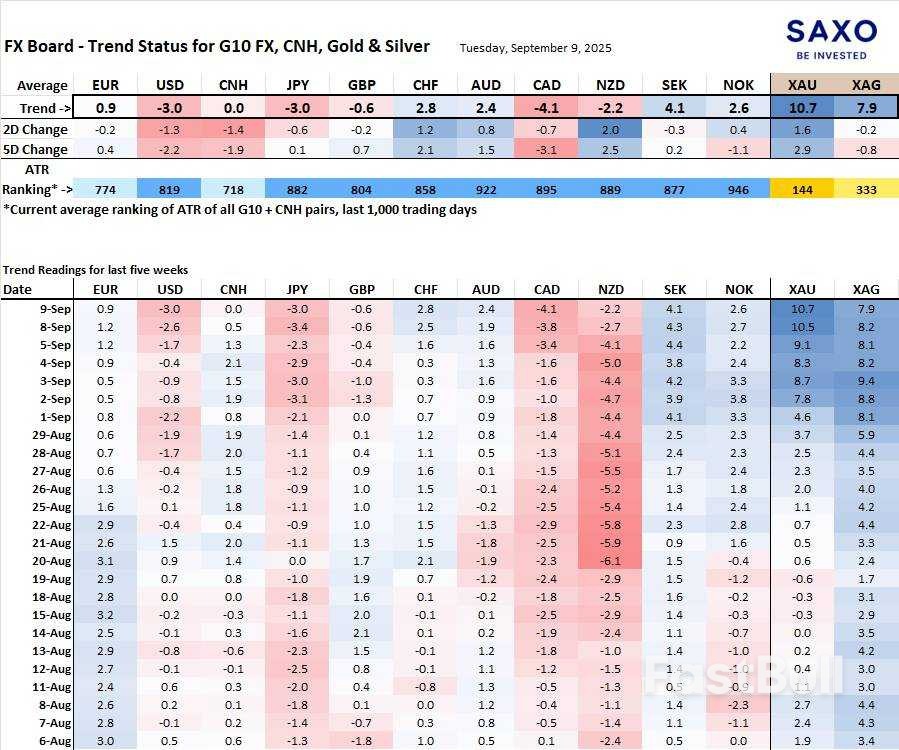

FX Board of G10 and CNH trend evolution and strength.Note: If unfamiliar with the FX board, please see a video tutorial for understanding and using the FX Board.

Both the US dollar and Japanese yen are weak if for different reasons – the US on collapsing yieds and anticipation of Fed cutting, the yen on concern that the bond market is destabilizing and political uncertainty. CAD is in a world of hurt as it follows the US dollar lower on an economy nosediving, in part on tariff-driven woes. On the positive side, the Swedish krona sticks out, possibly on its pristine balance sheet, something that the Swiss can also relate to, while gold and silver are blistering hot with incredibly strong bull trend readings.

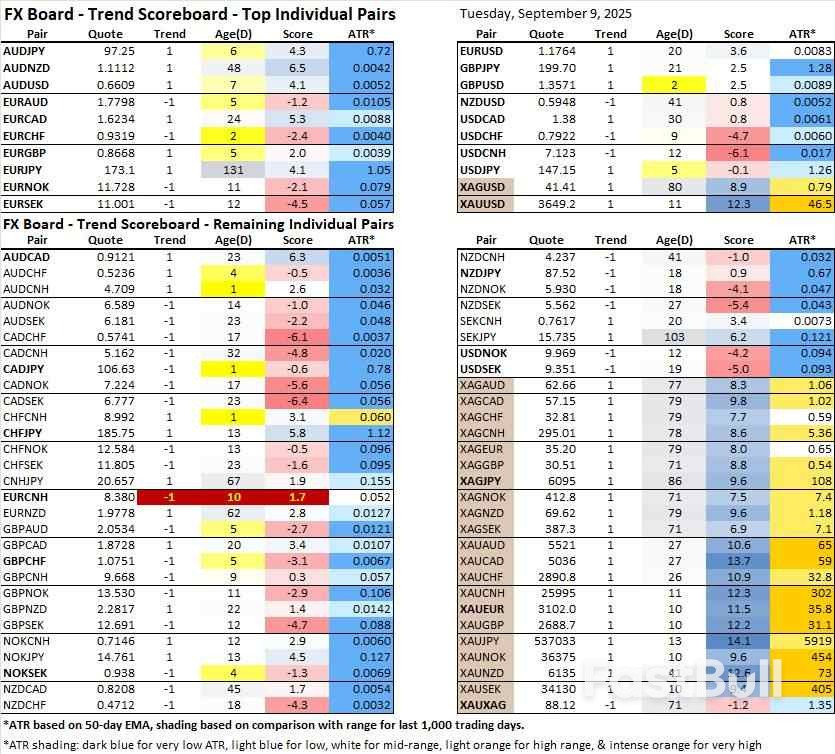

Table: NEW FX Board Trend Scoreboard for individual pairs.Fresh USD bearish trend signals in recent days in GBPUSD and humorously enough in USDJPY (the trend signal is useless when currency pairs are caught in a trading range as the moving averages meander back in forth within the range). Note the French concerns have also weighed on the euro in some crosses like EURAUD and EURGBP of late.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up