Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The Aussie is flying high on the run-up in metals and now strong employment data, but the move may be overdone. Elsewhere, GBP remains in a world of hurt and USDJPY is dancing nervously around the 155.00 figure as market perhaps reluctant to challenge Japanese officialdom.

Chart focus: AUDNZDThe AUDNZD pair has been one of this year's great trenders, driven by the ever-wider divergence in yields at the front of the yield curve as Aussie rates have remained firmly anchored and even risen sharply from the October lows - especially overnight on the strong AU employment data - while NZ rates trended consistently lower from July through mid-October before stabilizing. Arguably the yield spread – currently at 107 basis points for 2-year swaps, a level last seen in when AUDNZD was trading 1.25+ justifies further upside to 1.2000 and beyond, but near term, have to wonder if this is as good as it gets. Note the beautiful Elliott Wave patterns from the lows to the latest surge higher looking like a "fifth wave of wave five". Yes, the saying goes that we should follow the trend until it bends, but this may be as good as it gets for a while. To prove the point, however, we would need a sharp rejection of this latest surge above 1.1600.

Source: Saxo

Source: SaxoThere is a lot going on in Washington and some interesting new policy impulses in the mix from Treasury Secretary Bessent. Will the market fret new fiscal excess as Trump goes hard populist to throw bread at the masses? The US dollar has been quiet, but needs to send a signal here soon and seems to be trying this morning. USDCAD and AUDUSD suggest USD is softening – as does EURUSD this morning above 1.1600 – today could prove pivotal if the latter sticks a strong close.

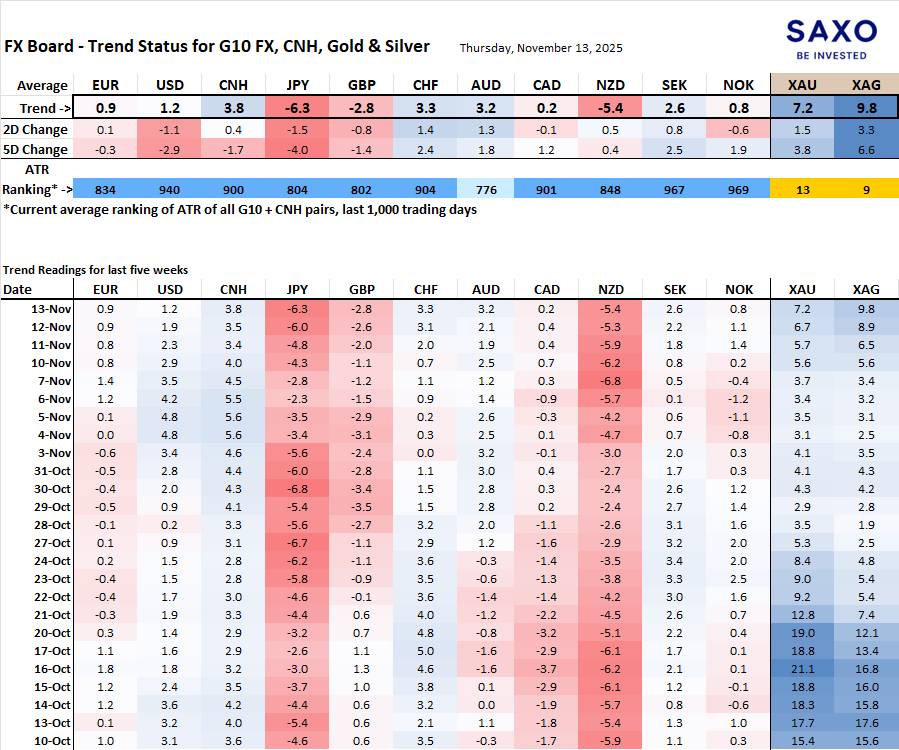

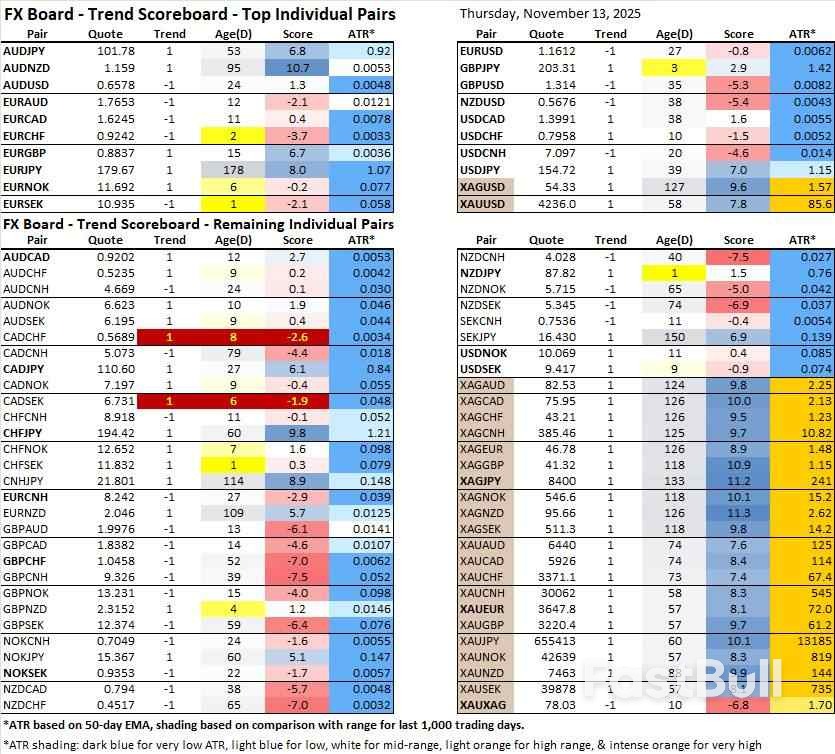

FX Board of G10 and CNH trend evolution and strength.Note: If unfamiliar with the FX board, please see a video tutorial for understanding and using the FX Board.

JPY weakness remains the strongest signal, together with NZD weakness – although the latter may be getting overdone as the NZD shorts may be overplayed here. CNH strength sticks out, especially on the move overnight versus the US dollar.

EURSEK has flipped back to negative and enjoys a seasonal tailwind to the downside through year-end. Elsewhere, the AUDUSD threatens an upside trend flip, while the USDCHF "uptrend" is likewise looking on tilt, as is EURUSD soon if it sticks a rally well above 1.1600 for two or three days.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up