Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Signal Accounts for Members

All Signal Accounts

All Contests

U.K. Trade Balance (Oct)

U.K. Trade Balance (Oct)A:--

F: --

P: --

U.K. Services Index MoMA:--

F: --

P: --

U.K. Construction Output MoM (SA) (Oct)A:--

F: --

P: --

U.K. Industrial Output YoY (Oct)A:--

F: --

P: --

U.K. Trade Balance (SA) (Oct)A:--

F: --

P: --

U.K. Trade Balance EU (SA) (Oct)A:--

F: --

P: --

U.K. Manufacturing Output YoY (Oct)A:--

F: --

P: --

U.K. GDP MoM (Oct)A:--

F: --

P: --

U.K. GDP YoY (SA) (Oct)A:--

F: --

P: --

U.K. Industrial Output MoM (Oct)A:--

F: --

P: --

U.K. Construction Output YoY (Oct)A:--

F: --

P: --

France HICP Final MoM (Nov)

France HICP Final MoM (Nov)A:--

F: --

P: --

China, Mainland Outstanding Loans Growth YoY (Nov)

China, Mainland Outstanding Loans Growth YoY (Nov)A:--

F: --

P: --

China, Mainland M2 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M0 Money Supply YoY (Nov)A:--

F: --

P: --

China, Mainland M1 Money Supply YoY (Nov)A:--

F: --

P: --

India CPI YoY (Nov)

India CPI YoY (Nov)A:--

F: --

P: --

India Deposit Gowth YoYA:--

F: --

P: --

Brazil Services Growth YoY (Oct)

Brazil Services Growth YoY (Oct)A:--

F: --

P: --

Mexico Industrial Output YoY (Oct)

Mexico Industrial Output YoY (Oct)A:--

F: --

P: --

Russia Trade Balance (Oct)

Russia Trade Balance (Oct)A:--

F: --

P: --

Philadelphia Fed President Henry Paulson delivers a speech

Philadelphia Fed President Henry Paulson delivers a speech Canada Building Permits MoM (SA) (Oct)

Canada Building Permits MoM (SA) (Oct)A:--

F: --

P: --

Canada Wholesale Sales YoY (Oct)A:--

F: --

P: --

Canada Wholesale Inventory MoM (Oct)A:--

F: --

P: --

Canada Wholesale Inventory YoY (Oct)A:--

F: --

P: --

Canada Wholesale Sales MoM (SA) (Oct)A:--

F: --

P: --

Germany Current Account (Not SA) (Oct)

Germany Current Account (Not SA) (Oct)A:--

F: --

P: --

U.S. Weekly Total Rig CountA:--

F: --

P: --

U.S. Weekly Total Oil Rig CountA:--

F: --

P: --

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)

Japan Tankan Large Non-Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Small Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Large Non-Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Large Manufacturing Outlook Index (Q4)--

F: --

P: --

Japan Tankan Small Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Large Manufacturing Diffusion Index (Q4)--

F: --

P: --

Japan Tankan Large-Enterprise Capital Expenditure YoY (Q4)--

F: --

P: --

U.K. Rightmove House Price Index YoY (Dec)--

F: --

P: --

China, Mainland Industrial Output YoY (YTD) (Nov)--

F: --

P: --

China, Mainland Urban Area Unemployment Rate (Nov)--

F: --

P: --

Saudi Arabia CPI YoY (Nov)

Saudi Arabia CPI YoY (Nov)--

F: --

P: --

Euro Zone Industrial Output YoY (Oct)

Euro Zone Industrial Output YoY (Oct)--

F: --

P: --

Euro Zone Industrial Output MoM (Oct)--

F: --

P: --

Canada Existing Home Sales MoM (Nov)--

F: --

P: --

Euro Zone Total Reserve Assets (Nov)--

F: --

P: --

U.K. Inflation Rate Expectations--

F: --

P: --

Canada National Economic Confidence Index--

F: --

P: --

Canada New Housing Starts (Nov)--

F: --

P: --

U.S. NY Fed Manufacturing Employment Index (Dec)--

F: --

P: --

U.S. NY Fed Manufacturing Index (Dec)--

F: --

P: --

Canada Core CPI YoY (Nov)--

F: --

P: --

Canada Manufacturing Unfilled Orders MoM (Oct)--

F: --

P: --

Canada Manufacturing New Orders MoM (Oct)--

F: --

P: --

Canada Core CPI MoM (Nov)--

F: --

P: --

Canada Manufacturing Inventory MoM (Oct)--

F: --

P: --

Canada CPI YoY (Nov)--

F: --

P: --

Canada CPI MoM (Nov)--

F: --

P: --

Canada CPI YoY (SA) (Nov)--

F: --

P: --

Canada Core CPI MoM (SA) (Nov)--

F: --

P: --

Canada CPI MoM (SA) (Nov)--

F: --

P: --

No matching data

Latest Views

Latest Views

Trending Topics

Top Columnists

Latest Update

White Label

Data API

Web Plug-ins

Affiliate Program

View All

No data

Despite OPEC+ announcing the largest output hikes in three years, actual global oil supply remains tighter than expected due to underperformance among producers, strong summer demand...

Key Points:

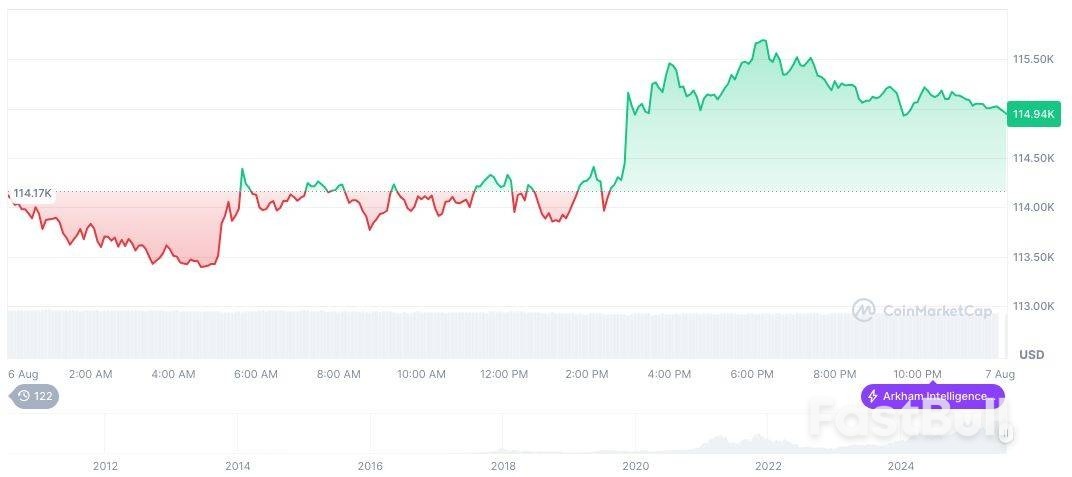

Bitcoin's approach to its 50-day moving average signals a market correction exacerbated by summer trading patterns and diminishing bullish sentiment, according to analysts' reports from August 7, 2025.

This correction underscores the cryptocurrency market's vulnerability to seasonal factors, highlighting traders' cautious stance amidst macroeconomic uncertainties and shifting sentiment in options markets.

The recent market correction, particularly impacting Bitcoin, aligns with summer seasonal weakness and macroeconomic factors. Analysts noted Bitcoin's frequent testing of the 50-day moving average, signaling "accumulation fatigue," as described by FxPro's Chief Market Analyst, Alex Kuptsikevich. The market has paused to lock in profits, while traders shift focus to smaller projects.

Market sentiment for Bitcoin’s long-term performance has shifted from a previously bullish outlook to neutrality. This change reflects the broader market's reassessment of future trends amid continued uncertainty. As Griffin Ardern of BloFin stated, "The bullish sentiment for Bitcoin's long-term options has dissipated, now firmly holding a neutral stance."

Analysts such as James Check describe the sell-off as "a traditional benign event," with active discussions on platforms like BlockBeats reflecting a cautious attitude toward potential future market weakness.

Did you know? Bitcoin has frequently tested its 50-day moving average, indicating market sentiment shifts over time.

Bitcoin (BTC) is priced at $114,333, with a market cap of $2.28 trillion, commanding a 60.84% dominance in the crypto landscape. Over the past 90 days, BTC has demonstrated an 11.23% increase in price, as reported by CoinMarketCap.

Source: CoinMarketCap

Source: CoinMarketCapAccording to the Coincu research team, the observed neutral market sentiment and past trends suggest Bitcoin’s price could stabilize or decline further if broader economic uncertainties persist. Predictions rely on past performance and current on-chain indicators.

Traders should monitor fresh macro data out of Australia and China early in the session, stay vigilant for new tariff headlines or trade policy updates from the U.S., and pay particular attention to risk sentiment shifts as global data and central bank communications filter through. Market volatility is expected to remain elevated amid ongoing uncertainty surrounding U.S. trade policies and global monetary policy direction.

The U.S. Dollar is on the defensive today, pressured by expectations of Fed rate cuts, lingering concern about the economic fallout from new tariffs, and heightened political risk. Market volatility remains elevated, with traders focused on both economic data and headline risk from Washington. The dollar index (DXY), which measures the USD against a basket of major peers, fell about 0.61% in late New York trading, reflecting a broad-based decline. Recent sessions saw the dollar retreat from a short-term high reached earlier in the week, as optimism about new U.S. trade deals faded and investors reassessed risks from upcoming tariffs.Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

Gold remains in a holding pattern as traders weigh the likelihood of imminent Fed rate cuts against the strength of the US dollar and ongoing tariff/trade uncertainty. Asian and global investors should watch for Fed commentary, US macro data, and any unexpected geopolitical headlines for signs of a breakout from the current price range. Gold is holding firm near recent highs. Leading into August 7, gold traded in a $3,370–$3,379 per ounce range following a multi-session rally and brief consolidation.Next 24 Hours Bias

Medium Bullish

The Australian Dollar is regaining ground amid improved global risk sentiment and hopes for trade stability. However, the currency’s direction will remain highly sensitive to central bank messaging (particularly the RBA), evolving U.S. interest rate expectations, and Australia’s external trade data. Immediate attention will focus on macro reports and RBA commentary slated for the rest of the session.

Central Bank Notes:

Weak Bearish

The NZD is steady but fragile following weak labor data, rising inflation expectations, and heightened U.S. trade barriers. Market sentiment will pivot on future RBNZ signals and further developments in global trade or commodity prices. The Reserve Bank of New Zealand’s (RBNZ) quarterly survey showed business inflation expectations holding at 2.29% for Q3 2025, matching the previous quarter and remaining at the highest level in a year. This read is especially significant as it comes ahead of the RBNZ’s next policy meeting, informing interest rate trajectory decisions. The central bank uses these figures to assess whether current policy is anchoring inflation in the target band.

Central Bank Notes:

Next 24 Hours Bias

Weak Bearish

The yen is likely to remain under pressure amid BOJ caution, soft economic momentum, and persistent trade risks. Japanese government bond auctions and domestic demand indicators are critical for the near-term yen direction. Any new headlines regarding US tariffs or BOJ policy may trigger further volatility for JPY and related assets.The Japanese yen (JPY) continued to weaken, trading around 147.3–147.7 per US dollar as of August 6, down approximately 0.17% from the previous session. Over the past month, the yen has been on a downtrend, losing close to 1% against the dollar amid lingering economic and trade uncertainties. Market forecasts suggest further potential yen weakness, with models pointing to USD/JPY levels above 149 later in the quarter.

Central Bank Notes:

Next 24 Hours BiasStrong Bullish

Oil prices are near multi-week lows after OPEC+ output hikes and amid cautious global sentiment. U.S. demand offers support, but mixed signals from China and worries about oversupply weigh on prices. Key risks include escalating U.S. tariffs, potential sanctions on Russian oil, and the pace at which OPEC+ restores previously cut supply. These developments suggest heightened volatility and a complex interplay of supply increases, global economic and policy risks, and evolving demand, shaping oil market sentiment today.Next 24 Hours Bias

Weak Bearish

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

White Label

Data API

Web Plug-ins

Poster Maker

Affiliate Program

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up