Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The U.S. dollar steadied Friday, but was on course for a third consecutive weekly fall after the Federal Reserve cut interest rates earlier this week, bringing borrowing costs to a nea...

The U.S. dollar steadied Friday, but was on course for a third consecutive weekly fall after the Federal Reserve cut interest rates earlier this week, bringing borrowing costs to a near three-year low.

At 04:00 ET (09:00 GMT), the Dollar Index, which tracks the greenback against a basket of six other currencies, traded largely unchanged at 97.995, but was set for a weekly drop of 0.7%.

The index is down more than 9% this year, on pace for its steepest annual drop since 2017.

The U.S. central bank lowered rates by 25 basis points this week, as expected, but remarks from Chair Jerome Powell at his post-meeting press conference were more balanced and less hawkish than many had anticipated.

The Fed policymakers also forecast another rate cut next year, even with members of the central bank showing divisions over December's move.

"The bearish wind is coming not only from interest rates but also from end-of-year seasonality," said analysts at ING, in a note. "Dollar rates saw another calibration of Fed expectations lower, with the 2y falling to 3.50% and the market pricing in 3.05% as the Fed terminal rate at the end of next year, keeping pressure on the U.S. dollar."

The focus going forward will hinge on economic data that is still lagging from the impact of the 43-day federal government shutdown in October and November, as well as the identity of the next Fed chair.

In Europe, GBP/USD dropped 0.1% to 1.3383, falling back from its highest level since October after data showed that the U.K. economy unexpectedly contracted in October, with uncertainty ahead of the Autumn budget by Chancellor Rachel Reeves likely curtailing growth.

Data released earlier Friday by the Office for National Statistics showed that U.K. gross domestic product fell by 0.1% on a monthly basis in October, matching the drop seen during the prior month and below the 0.1% growth expected.

The Bank of England holds its final policy-setting meeting of the year next week, and is widely expected to cut interest rates by a quarter point to 3.75% as recent data has shown inflation drifting lower.

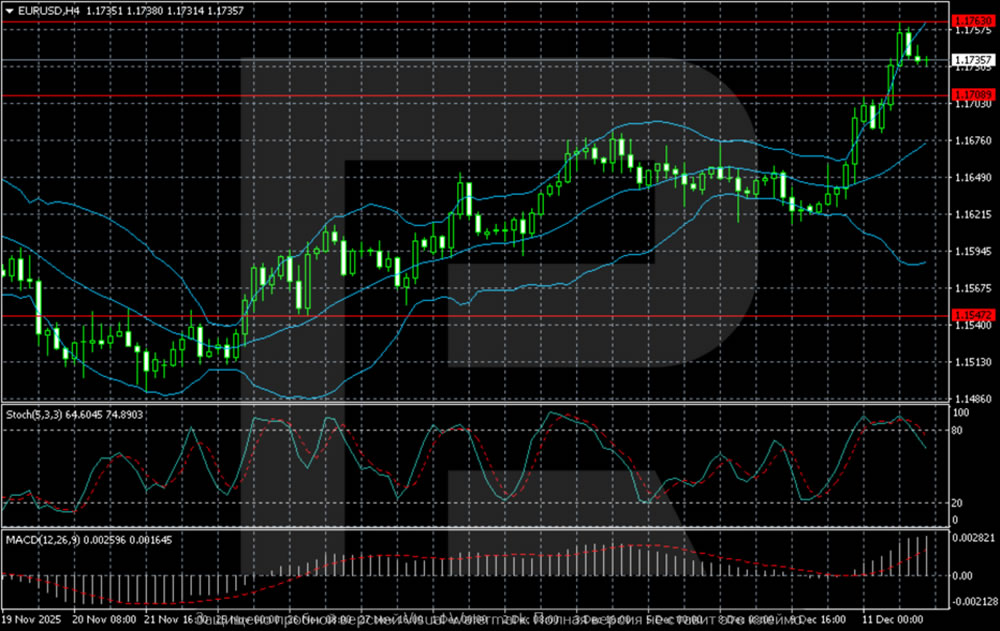

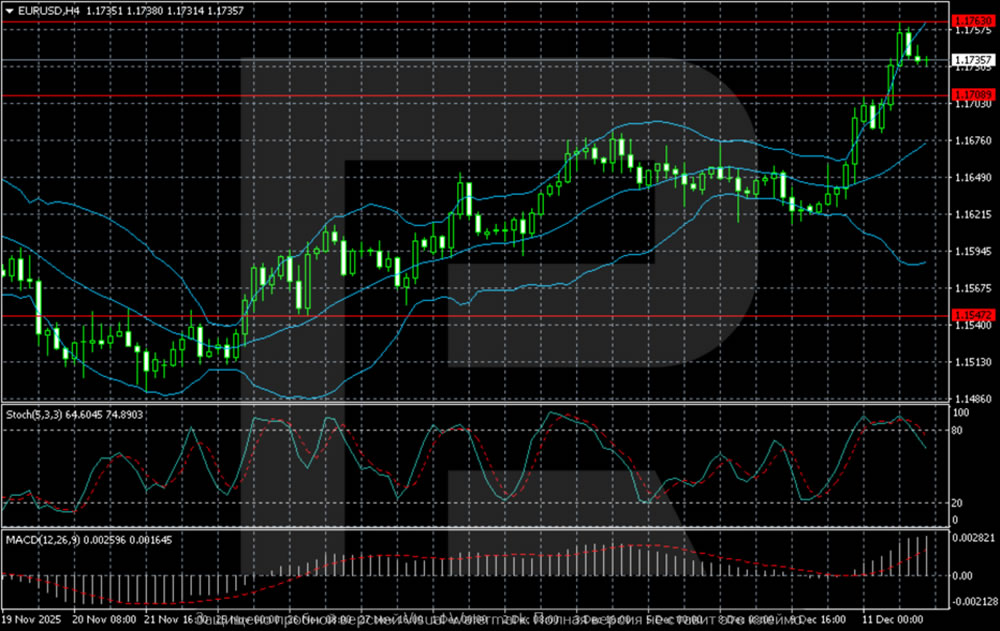

EUR/USD edged lower to 1.1736, but the single currency was poised to register weekly gains of 0.8%, on course for a third weekly gain.

German inflation rose to 2.6% in November, confirming preliminary data, while consumer prices harmonised to compare with other European Union countries, stood at 2.3% year-on-year in October.

"Following the Fed meeting this week, the market's attention will shift to the ECB meeting next Thursday. President Christine Lagarde will present a new forecast, which should be the first test of the current pricing of no further rate cuts, in line with our view," ING added.

In Asia, USD/JPY gained 0.1% to 155.73, with the yen slightly lower ahead of next week's Bank of Japan meeting where the broad expectation is for a rate hike.

The market focus is on comments from the policymakers on how the Japanese rate path will look in 2026.

USD/CNY traded 0.1% lower to 7.0556, while AUD/USD gained 0.1% to 0.6673, set for a weekly gain of 0.5% as persistent inflationary pressures suggests the Reserve Bank of Australia could hike rates in the near-term.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up