Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

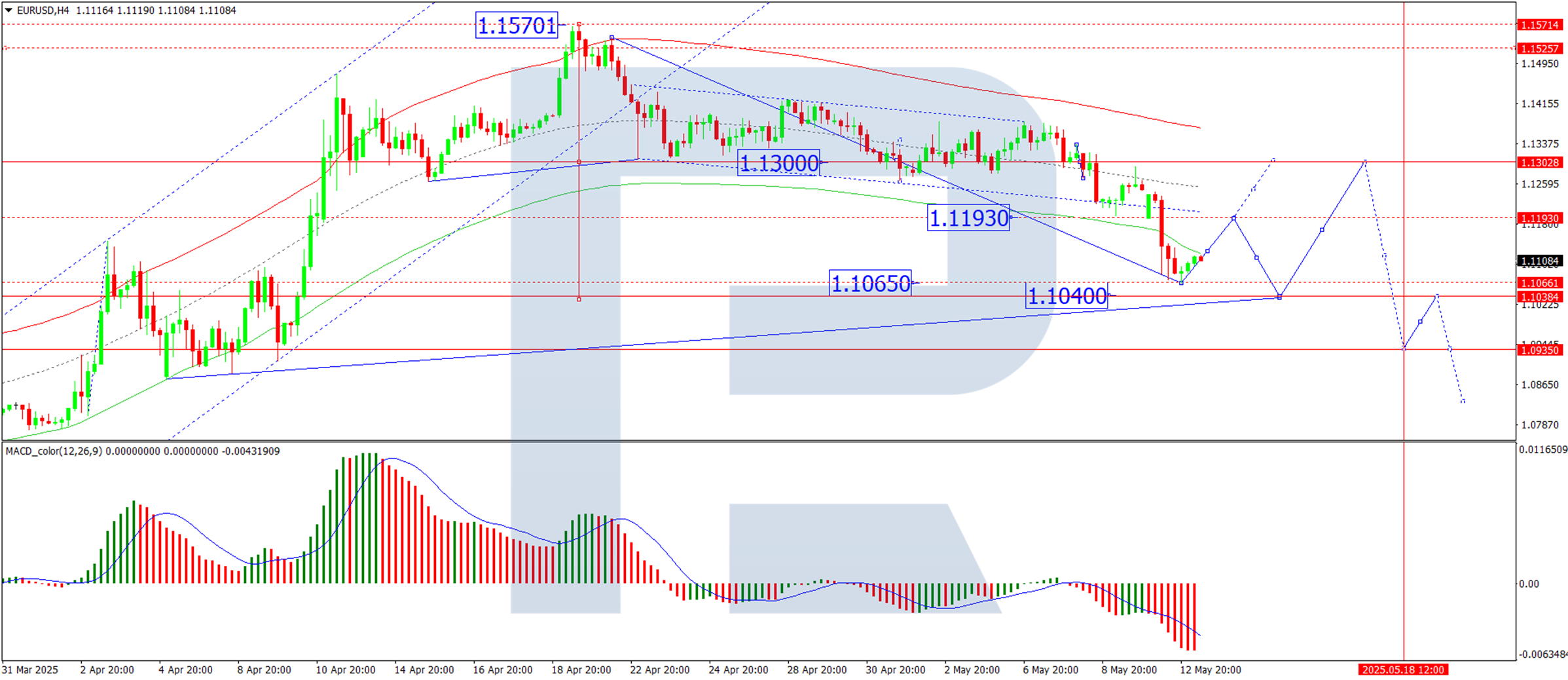

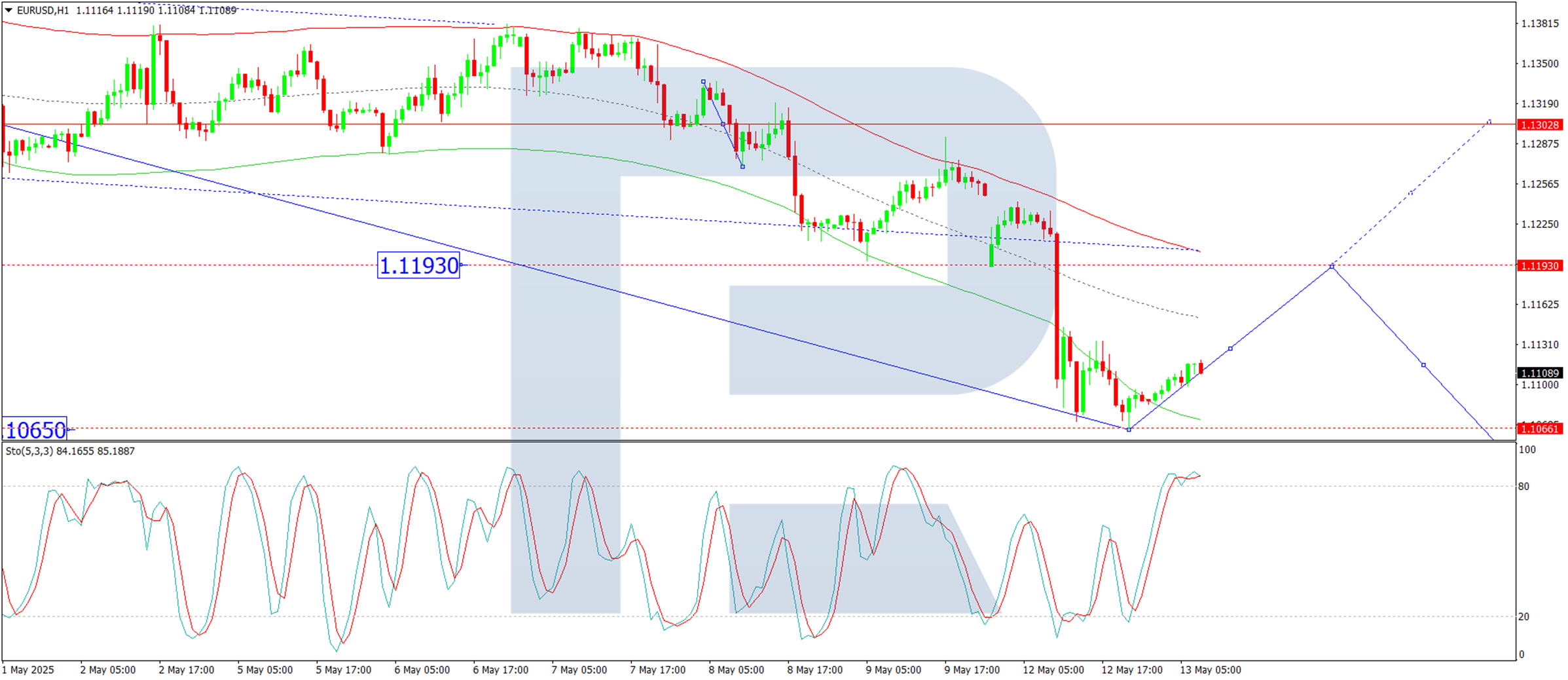

Headline CPI rose 2.3% YoY last month, cooler than consensus expectations for an unchanged 2.4% YoY, while core prices rose by 2.8% on an annual basis. So-called ‘supercore' prices, meanwhile, aka core services inflation less housing, rose 2.7% YoY in April, a fresh low since early-2021, and a notable decline from the prior 2.9% annual rate.

Headline CPI rose 2.3% YoY last month, cooler than consensus expectations for an unchanged 2.4% YoY, while core prices rose by 2.8% on an annual basis. So-called ‘supercore' prices, meanwhile, aka core services inflation less housing, rose 2.7% YoY in April, a fresh low since early-2021, and a notable decline from the prior 2.9% annual rate.

On an MoM basis, meanwhile, price pressures firmed compared to the previous couple of months, largely a result of tariffs beginning to boost prices across the economy, the impacts of which will continue to show up over the next quarter or two, even though the most drastic trade levies have been dramatically pared back since ‘Liberation Day'. Headline CPI rose 0.2% MoM in April, cooler than expected but still the firmest print since January, while prices excluding food and energy also rose 0.2% MoM over the same period.

Annualising this monthly data helps to provide a better idea of the inflationary backdrop, and underlying price trends:

Digging a little deeper into the data, the April CPI report pointed to a continuation of recent trends, with goods price pressures continuing to firm, as core goods deflation came to an end for the first time since the start of 2024, even as core services prices continued to ebb.

In the aftermath of the data, money markets underwent a modest dovish repricing, though little moves of any significance, with the USD OIS curve continuing to discount two 25bp Fed cuts by year-end, in September and December.

On the whole, the April inflation figures won't be a game-changer, or anything of the sort, for the FOMC and the near-term policy outlook. Powell & Co. remain firmly in ‘wait and see' mode for the time being, seeking to sit on the sidelines amid a ‘well positioned' policy stance, assessing both incoming economic data, as well as changes in trade policy, and digesting how these shifts may alter the balance of risks facing each side of the dual mandate.

Primarily, though, the Committee's focus remains on ensuring that inflation expectations remain well-anchored as, even in light of the recent reduction in US tariffs on Chinese goods, the substantial rise in the overall average effective tariff rate is near-certain to result in CPI continuing to head higher through the summer.

With these upside inflation risks in mind, as well as the considerable degree of uncertainty that continues to cloud the economic outlook, and the labour market remaining in rude health, the bar to Fed action in the short-term remains a very high one indeed. While the direction of travel for rates remains lower, any cuts before the end of the third quarter seem a very long shot indeed, barring a significant deterioration in labour market conditions and policymakers obtaining sufficient confidence in price pressures remaining contained in the meantime.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

Above: "78% of European investors expect US growth to slow over the coming months, down from 89% last month, while 16% expect growth to flatline, up from 7% last month" - Bank of America.

Above: "78% of European investors expect US growth to slow over the coming months, down from 89% last month, while 16% expect growth to flatline, up from 7% last month" - Bank of America.