- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Takaichi has called a snap election just three months into the job, taking a high-risk move. It is all about securing a public mandate for her policy.

Takaichi has called a snap election just three months into the job, taking a high-risk move. It is all about securing a public mandate for her policy.

She inherited a troubled party and a minority government in October after Ishiba Shigeru, who lost both parliamentary elections, was nearly forced to resign. The LDP lost public support with a cost-of-living crisis and several political funding scandals. Despite only narrowly becoming prime minister, her approval ratings during the first three months were surprisingly strong at around 70%. Now, she seeks to leverage her popularity to secure a sole majority for the LDP and thereby advance her policy agenda later with greater consistency. She supports former Prime Minister Shinzo Abe's policies, advocating pro-stimulus macro policies and a Japan-focused foreign policy. Opposition parties may not fully agree with her policy perspectives. Should the minority government situation persist, she will have to negotiate with other parties on each policy issue. However, if she wins this election, she will interpret it as Japanese voters' endorsement of her pledges and will push her policy agenda much more forcefully.

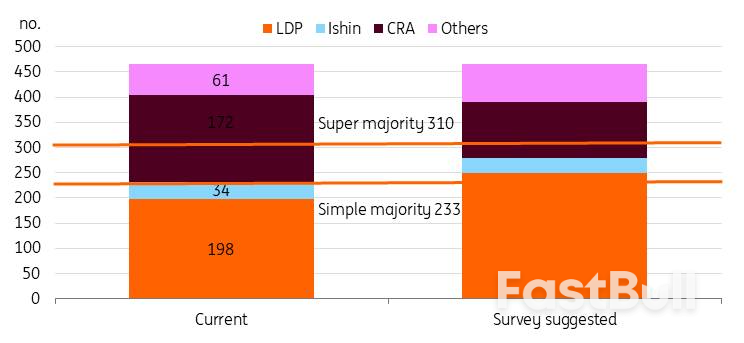

According to recent local polls, the LDP leads the campaign for sure. The LDP is expected to well exceed a simple majority of 233 seats (vs its current 198 seats) and the alliance may reach near 300. In contrast, the main opposition, the Centrist Reform Alliance, could lose almost half of its current seats. If the LDP coalition secures a super majority, the government would gain significantly more power. This would allow Takaichi to pass legislation even without having sufficient support in the Upper House.

Source: various news papers and ING estimates

Source: various news papers and ING estimatesAlthough the food consumption tax cut was a major topic before the campaign, its prominence diminished once the campaign began.

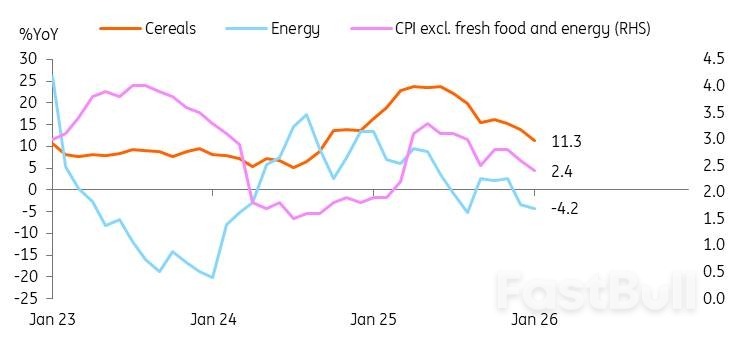

Japanese inflation has stayed above 2% since April 2022, but wages have lagged behind. The rise in living costs has increased public dissatisfaction. For instance, rice, the primary staple food, gained almost 100% year-on-year by mid-2025, although it came down to the 30% level recently. So, reducing inflation became a primary focus of the election campaign. Takaichi resumed energy subsidies last year via the supplementary budget. We see the impact of the subsidy from the recent sharp decline in inflation readings.

The focus has now turned to food prices. The food consumption tax rate of 8% is expected to reduce inflation by approximately one percentage point though at a cost of ¥5 trillion revenue loss (6% of total tax revenue). Although households may benefit from lower living costs, markets are worried about fiscal stability due to uncertain funding for the tax cuts.

However, after experiencing recent market volatility, Takaichi has adopted a more cautious stance on food tax cuts. She has avoided directly addressing the proposal during the campaign, focusing instead on "responsible and proactive public finances". Now she remains vague on implementation timing and prefers to "accelerate the discussion" to keep the agenda neutral.

Source: CEIC

Source: CEICThe market seems to have a fear that Takaichi's big victory may hurt fiscal conditions quite badly. We don't fully agree with it. If the LDP secures a majority in the lower house, Takaichi could speed up tax cut talks. She will argue that she has the public mandate. But a consensus still needs to be reached by the national council. The same should apply in case there is a super majority. Other opposition parties now support more expansionary fiscal policies; for instance, the CRA favours abolishing the food tax permanently, while the LDP suggests two-year exemptions. The LDP victory could result in a more balanced spending plan. Under Prime Minister Abe, Japan raised its consumption tax twice to help finance social security programmes for an ageing society, as part of the "Abenomics" reforms. It is expected that Takaichi will similarly focus on securing revenue while also aiming for greater spending.

As previously stated, the LDP has not specified when the tax cut might take effect. Additionally, the party has made explicit commitments to lowering Japan's debt-to-GDP ratio and implementing fiscal reforms. Therefore, the LDP is anticipated to devise strategies that prevent a sharp increase in the fiscal deficit.

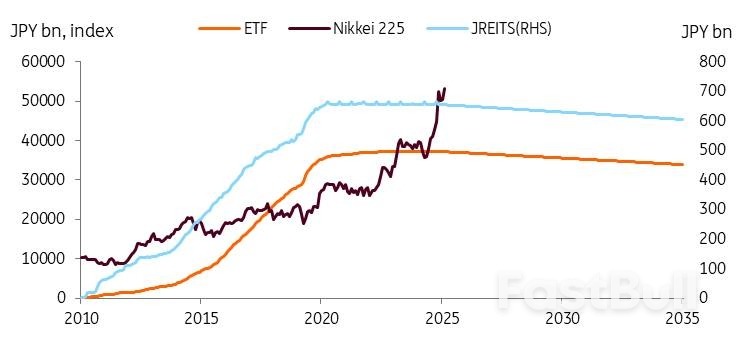

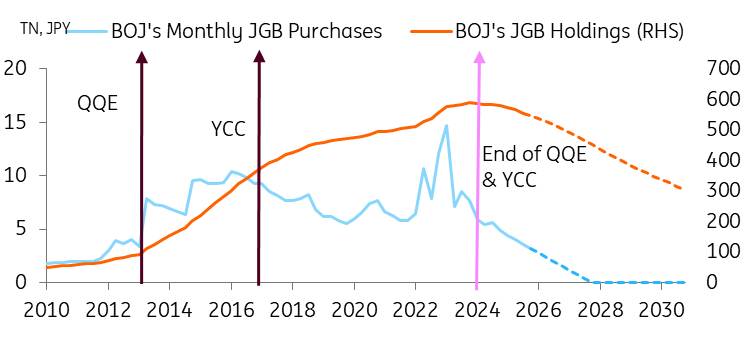

One potential funding approach involves seeking support from the BoJ. The BoJ commenced its initial asset sales in 2026, targeting an annual reduction of ¥330 billion in ETFs and ¥5 billion in JREITs. According to recent data, the BoJ's ETF and JREIT holdings declined by ¥5.3 billion and ¥0.1 billion respectively from December 2025 to January 2026. While this represents a modest decrease, the BoJ is expected to continue reducing its asset portfolio, a strategy anticipated to provide substantial returns over time. Since 2010, the Nikkei 225 has increased fivefold. With a simple calculation, the BoJ could earn about ¥1.7 trillion from selling an ETF book valued at ¥330 billion. If we suppose the Nikkei increases at the same rate as nominal GDP growth, this income stream has the potential to serve as a stable funding source.

Source: CEIC

Source: CEIC'Return to normal' implies higher inflation expectations, less central bank control over Japanese government bond (JGB) markets, increased volatility, and more yield adjustments.

We expect that the economy will return to a normal state after experiencing many years of deflation. While fiscal sustainability may contribute to higher yields, we think economic normalisation plays a stronger role in driving yields upward. These are reasons behind why we expect JGB yields to hit 3.0% by the end of 2027.

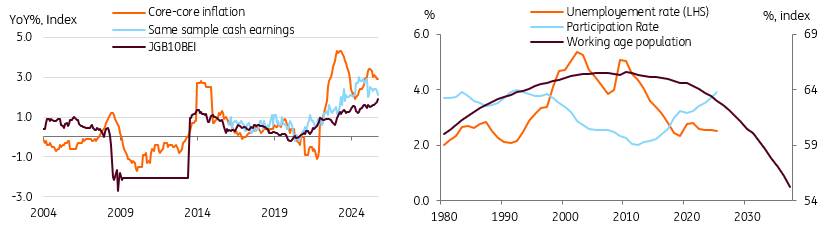

Returning to a normal state means achieving sustainable inflation growth of around 2%. Higher inflation expectations may explain the rise in JGB rates. The BEI index has been approaching 2%, and we expect inflation expectations to increase and stabilise near 2%, supported by structural labour shortages sustaining wage growth. Over the last three years, spring wage negotiations have resulted in wage growth exceeding 4-5%, and this year, an increase of over 5% is expected. Government subsidies, lowering energy and food prices, are expected to drive positive real wage growth this year, supporting demand-driven inflation and reinforcing progress toward a sustainable 2% target.

Source: CEIC, OECD, ING estimates

Source: CEIC, OECD, ING estimatesReturning to a normal state means that we expect the BoJ's slow and steady monetary policy normalisation via 1) policy rate hikes, a total of 75bp by the end of 2027 and 2) the BoJ's unwinding of unconventional monetary policy measures. As the BoJ buys less, the supply and demand balance shifts, creating upward pressure on JGB yields. While the BoJ will slow its reduction pace in April 2026, we expect the yield curve to steepen further during rate hikes, keeping spreads between the policy rate and 10Y JGBs at 150-175bp (currently 150bp). We believe that history doesn't necessarily predict well the future for JGBs, since past yield spreads happened during the deep disinflation. As quantitative tightening (QT) continues and bonds mature, the BoJ's control over the JGB market will diminish more, leading to more volatile, market-driven bond markets.

While sudden market movements may cause concern among market participants, they should be seen as part of the economy's return to normal. The BoJ and government must strike a careful balance; if a major sell-off occurs that is not driven by fundamentals, they can adjust the QT pace and bond issuances accordingly.

At the recent Bank of Japan meetings, following the JGB sell-off, Governor Ueda emphasised the bank's nimble approach to bond operations, which provides the BoJ significant flexibility. Nevertheless, his comments appear that the BoJ doesn't intend to change the path of rising yields; rather, just to smooth market volatility and prefers a more gradual progression. We believe that the BoJ will allow a gradual yield rise.

Lastly, we anticipate that government spending will rise further to address issues related to an ageing population and increased welfare needs. We expect investment in automation and digital technology to lead to higher expenditures as well. Due to Takaichi's significant spending plan, the goal of achieving a primary budget surplus by fiscal year 2025/2026 was not met and has been postponed. We do not expect an abrupt rise in debt issuance under the Takaichi administration, but we still believe her policy stance should keep pressure on JGB yields.

Source: Bank of Japan, CEIC, ING estimates

Source: Bank of Japan, CEIC, ING estimatesIt has been a volatile start to the year for USD/JPY, and it looks set to continue. The prevailing investment thesis has been that a negative real policy rate in Japan, burgeoning fiscal challenges and global investors favouring pro-cyclical currencies are all weighing on the yen. What seemed to be Japanese FX intervention near 160 and then reports of a Fed rate check late on Friday, 23 January have been the sole positives for the yen. Yet some official denials of US involvement and subsequent Japanese data question whether intervention took place at all. On the subject of intervention, we wonder whether strategic investment decisions from some of the government-influenced pension funds may be playing a role here – as is also the case in Korea when USD/KRW approaches 1500.

A positive election result for the LDP that would pump more air into the 'Takaichi trade' is a USD/JPY positive. USD/JPY could even approach 160/162 levels again on the back of this. Officials in Tokyo have made it clear they are uncomfortable with those kinds of levels, which, while good for exporters, also stand to increase import prices at a time when the government is trying to ameliorate the cost-of-living crisis. Therefore, FX intervention near 160/162 looks likely.

Will intervention be effective? Effective intervention requires heavy one-way market positioning and a turn in the fundamentals. Intervention proved effective in July 2024 when the speculative market was extremely short yen and the Fed was about to embark on an easing cycle – which the Fed did with a 50bp cut in September that year. USD/JPY fell from 160 to 140 over that two-month period.

Today, speculative positions are nowhere near as short yen as they were in 2024. And with the Fed funds rate now much closer to neutral at 3.75%, the prospect of lower short-dated US rates is far less compelling than it was two years ago. In short, the conditions are not in place today for a large correction lower in USD/JPY.

Instead, it looks like an LDP-inspired push higher in USD/JPY (assuming polls prove correct) will spark a sustained intervention campaign that could potentially last for the remainder of this year. For reference, the BoJ sold $100bn over four separate days between May and July in 2024. And in addition to the yen negatives discussed above, there is also the uncertainty about the timing of Japan's commitment to invest $550bn into the US – and whether that gets funded with dollar instruments (probably) or whether any FX flows are involved.

In all, we forecast USD/JPY to bounce around in a 155-160 range through the first half of the year and then 50bp of Fed rate cuts to drag it closer to 150 by year-end. But upside risks prevail for the rest of this quarter.

This USD/JPY narrative adds weight to our preference to receive Tonar and pay SOFR on the cross-currency swap. This is the 'negative carry play', which benefits from fixing USD/JPY at today's rate, and then buying back dollars in a year or two's time at that same rate. It is especially suitable for shorter tenors, ideally 1–2 years. Leave the positive carry play for longer tenors. Or, wait for a better entry point; a lower USD/JPY, with the bliss entry point at 140. See more on that here.

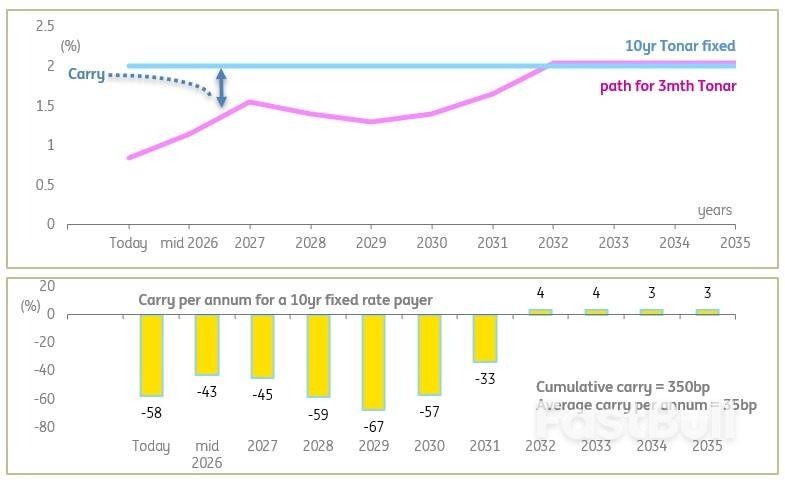

For corporates looking at the relationship between floating rate exposure and fixed rate exposure post the elections, there are two key observations. First, floating rate Tonar rates are on a long winding path higher, eventually to 2%, although more likely to see a peak at around 1.5% in this current cycle. Still, floating-rate exposures remain the cheaper funding option for the coming few years, when compared with say 10yr Tonar (now at 2%).

That being said, 10yr Tonar is likely to remain under upward pressure (in line with JGBs), which means that fixed rate payers set today would prove a positive mark-to-market outcome in the intermediate period. Also, we doubt there will be a fall to materially lower-rate lock-in opportunities, so the rate seen on screens today is about as good as it gets (give or take c.20bp, and barring the unexpected). The alternative is to look at lower lock-in levels in shorter tenors, say the 1.5% attainable in the 4yr tenor. We calculate that the average carry cost there per annum is about 20bp, compared with 35bp for the 10yr lock-in.

For those looking to swap to floating, there is positive impact carry and positive cumulative carry, but it tapers, and is not dramatically high (350bp in the 10yr). The chart below illustrates the profile in the coming 10yrs, and the carry outcome for a 10yr fixed rate payer set today (reverse the signs for the fixed rate receiver).

The long end is already at 2%, while the BoJ is on a slow path towards it, getting there eventually

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up