- USDX

- XAUUSD

- XAGUSD

- WTI

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

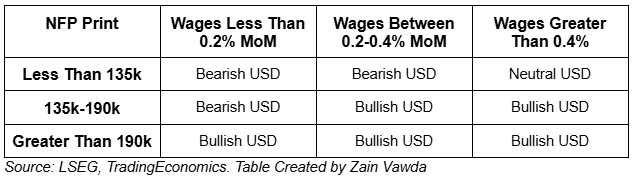

Consensus forecasts predict an increase of 169,000 jobs, with the unemployment rate expected to remain at 4.1%. Strong numbers (over 190,000 jobs) could strengthen the dollar, while weak numbers (less than 135,000 jobs) could weaken it. (DXY) currently has support levels around 107.00, 106.13, and 105.76, and resistance levels at 108.00, 108.49, and 109.52.

Consensus forecasts predict an increase of 169,000 jobs, with the unemployment rate expected to remain at 4.1%.

Strong numbers (over 190,000 jobs) could strengthen the dollar, while weak numbers (less than 135,000 jobs) could weaken it.

(DXY) currently has support levels around 107.00, 106.13, and 105.76, and resistance levels at 108.00, 108.49, and 109.52.

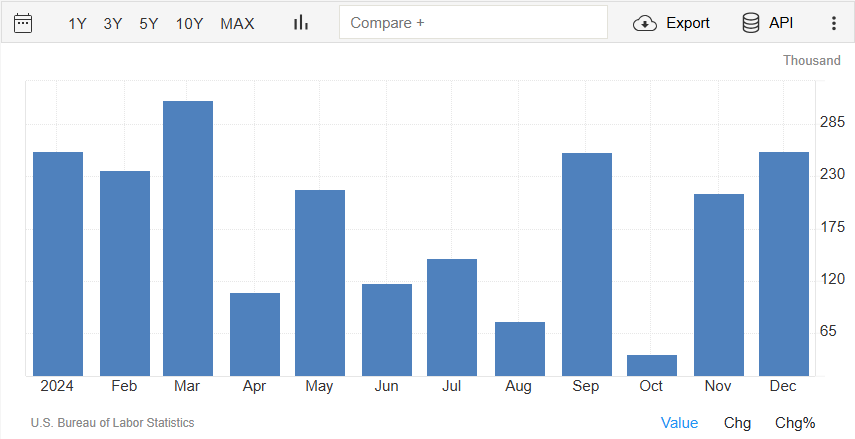

The US Bureau of Labor Statistics is set to release the non-farm payroll and jobs data for January 2025 on Friday, February 7th, 2025.

NFP Report Expectations

The consensus forecast for January’s non-farm payroll is an increase of 169,000 jobs, following a robust gain of 256,000 jobs in December 2024. Recent jobs data has been strong, with the US economy adding an average of 186,000 jobs per month in 2024. This suggests that the labor market remains healthy heading into 2025.

Source: TradingEconomics

The unemployment rate is expected to stay at 4.1%, and wages are predicted to grow by 0.3% this month (3.8% over the past year). However, job growth could be higher than expected, with estimates ranging from 175,000 to 225,000 new jobs.

As always the average hourly earnings measure will play a key role. Any significant deviation away from the 3.8-4% range here could see an uptick in inflation expectations. This would then have a knock on effect on Fed policy regarding rate cuts which could see the US Dollar experience some volatility.

There are challenges ahead with concerns that tariff uncertainty and growth worries may lead to a cautious approach toward hiring in the first part of 2025. It will be interesting to see if these concerns come to fruition and we see any cooling of the labor market and a drop in hiring.

The Current State of the US Labor Market

The US labor market is slowing down gradually. A December report showed over 500,000 fewer job openings, bringing the total to 7.6 million. Professional services and healthcare saw the biggest drops, while leisure and hospitality stayed strong.

Hiring has been slower, and layoffs are balancing out new hires in some industries. However, wages have stayed steady, with average pay growth at 3.9-4.0% over the past five months, showing that demand for workers is still solid.

There have been some mixed signs in recent data releases however, with metrics like the manufacturing and services PMI employment components, pointing to sustained hiring momentum. The ISM Manufacturing Employment Index recently climbed to 50.3, signaling expansion, while the ADP private payrolls report showed 183,000 jobs added in January.

Given the above and with the geopolitical and trade developments one may understand why tomorrow’s report is so crucial.

Potential Impact and Scenarios

The NFP report plays a big role in shaping the US Dollar Index (DXY) and overall market mood. If the report shows strong numbers, especially over 190,000 new jobs, the US dollar could strengthen, especially since it’s close to support levels around 107.50. But if the report is weak, with less than 135,000 jobs added or wage growth under 0.2%, markets may expect the Fed to cut rates more aggressively, which could weaken the dollar.

For stocks, strong job numbers might raise concerns about stubborn inflation moving forward, which could slow down market gains. On the other hand, weak job data could signal easier monetary policies ahead and more rate cuts thus stoking market optimism. .

Potential Impact on the US Dollar Based on the Data Released

Technical Analysis – US Dollar Index (DXY)

Looking at the US Dollar Index and bulls have failed to kick on this week as price action has now printed a lower high but no lower low has materialized yet. Will the jobs data help the DXY continue its recent malaise or will it give bulls renewed impetus to push on?

Immediate support rests at 107.00 before the 106.13 and 105.76 handles come into focus.

A move higher from here will need to break above the 108.00 handle before resistance at 108.49 and 109.52 come into focus.

US Dollar Index (DXY) Daily Chart, February 6, 2025

Source: TradingView (click to enlarge)

Support

107.00

106.13

105.76 (100-day MA)

Resistance

108.00

108.49

109.52

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up