Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

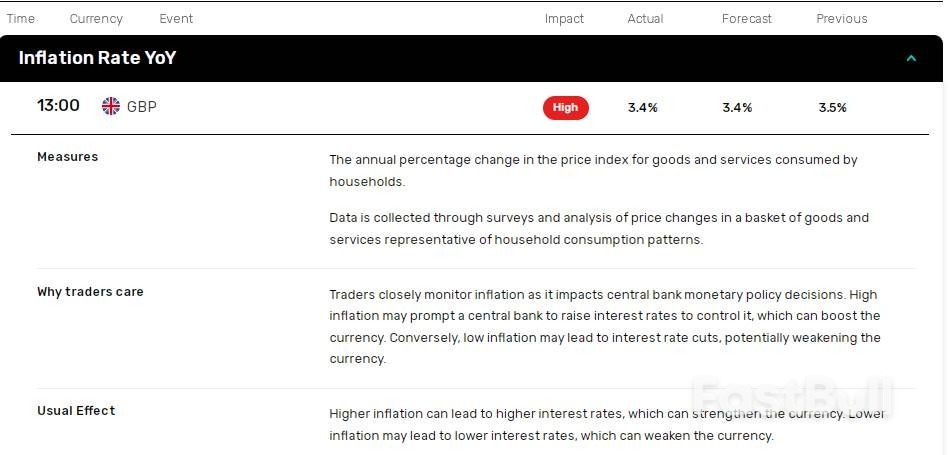

UK inflation cooled to 3.4% in May, fueling speculation about BoE rate cut bets amid slowing economic momentum. Core inflation dropped to 3.5%, below forecasts, supporting expectations of easing monetary policy. Sticky services inflation may delay BoE cuts despite weakening GDP and retail demand concerns.

Softer-than-expected UK inflation data fueled speculation about Bank of England rate cut bets on Wednesday, June 18.

The UK’s annual inflation rate (headline) cooled from 3.5% in April to 3.4% in May, aligned with a consensus of 3.4%. Core inflation dropped from 3.8% to 3.5% in May, below a consensus of 3.6%.

Key price trends from the Office for National Statistics included:

Despite the softer inflation readings, a spike in WTI crude oil prices in response to the Iran-Israel conflict may cloud the inflation outlook. Uncertainty about CPI trends may leave the BoE in a policy-holding pattern despite a faltering UK economy.

Economists expect the BoE to keep interest rates at 4.25% on Thursday, June 19, despite the UK economy losing momentum in April. The UK GDP fell 0.3% month-on-month as services output dropped for the first time since October 2024.

However, sticky inflation and potentially higher oil prices could raise stagflation risks. Monetary policy uncertainty and a worsening economic outlook may pressure GBP/USD.

Ahead of May’s inflation report, ING Economics commented on the BoE’s potential rate path, stating:

“We expect the Bank of England to keep rates at 4.25% on 19 June, but some disappointing job numbers, lower wage growth, and a more optimistic outlook for services inflation mean we expect cuts in August and November.”

May’s services inflation numbers supported ING Economics’ outlook. However, the Iran-Israel conflict remains a curveball for economists and central bankers.

Friday’s upcoming retail sales figures could give a better gauge of momentum in the UK economy and the BoE’s path forward.

Ahead of the inflation report, the GBP/USD dipped to a low of $1.34145 before climbing to a high of $1.34489. Following the report, the pair fell to a low of $1.34403 before surging to a high of $1.34621.

On Wednesday, June 18, the GBP/USD was up 0.19% to $1.34530. The upswing likely signaled the potential impact of sticky inflation on the BoE’s policy outlook.

GBPUSD – 3 Minute Chart – 180625

GBPUSD – 3 Minute Chart – 180625Traders must now turn to the BoE’s interest rate decision on June 19 and Friday’s UK retail sales. Consumer spending data may offer further insights into consumer sentiment and potential GDP and inflation trends.

A drop in retail sales could signal further economic weakness and softer inflation, supporting multiple BoE rate cuts. However, strong retail sales could dampen BoE rate cut bets, sending GBP/USD higher.

In parallel, trade developments and the Iran-Israel conflict will remain key drivers of risk sentiment and GBP/USD price action.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up