Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The U.S. Federal Reserve should not cut interest rates "for some time" as the impact of Trump administration tariffs begin passing through to consumer prices, with tight monetary policy needed to keep inflationary psychology in check, Federal Reserve governor Adriana Kugler said on Thursday.

The U.S. Federal Reserve should not cut interest rates "for some time" as the impact of Trump administration tariffs begin passing through to consumer prices, with tight monetary policy needed to keep inflationary psychology in check, Federal Reserve governor Adriana Kugler said on Thursday.

With unemployment stable and low, and inflation pressures building, "I find it appropriate to hold our policy rate at the current level for some time," Kugler said in remarks prepared for delivery at a housing forum in Washington D.C. "This still-restrictive policy stance is important to keep longer-run inflation expectations anchored."

Ongoing hiring and a 4.1% unemployment rate show the job market "stable and close to full employment," Kugler said. "Inflation, meanwhile, remains above the FOMC’s 2% goal and is facing upward pressure from implemented tariffs."

That pressure was apparent in this week's Consumer Price Index report that showed large price increases across an array of heavily imported goods, and Kugler said she felt there were many reasons to think price pressures would continue to build -- including the fact that the administration still seems to intend to impose higher levies on major trading partners in coming weeks.

"I see upward pressure on inflation from trade policies, and I expect additional price increases later in the year," she said. She estimated that coming data will show the Personal Consumption Expenditures price index, which the Fed uses to set its 2% inflation target, increased 2.5% in June, while the "core" measure outside of volatile food and energy items increased 2.8%, higher than in May.

"Both headline and core inflation have shown no progress in the last six months," Kugler said.

The Fed meets on July 29-30 and policymakers are expected to hold the benchmark interest rate steady in the current range of 4.25% to 4.5%. It will be the fifth consecutive meeting without a change since the Fed paused a series of rate cuts in December.

Since then, and to President Donald Trump's consternation, focus has turned to the impact Trump administration trade and other policies will have on inflation, jobs and economic growth. Fed policymakers say they are reluctant to resume rate reductions until they are more certain that tariffs will lead to only a one-time price adjustment, as administration officials contend, and not more persistent inflation.

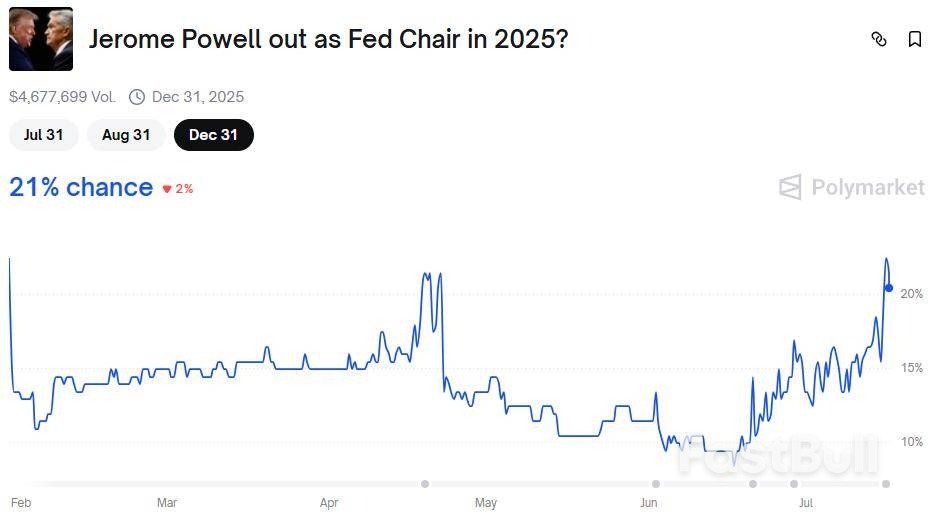

Appointed to the Fed by former President Joe Biden, Kugler's term at the central bank ends in January, creating a vacancy that the Trump administration may use to appoint a replacement for Fed chair Jerome Powell when his term as Fed chief ends in May.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up