- GBPUSD

- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

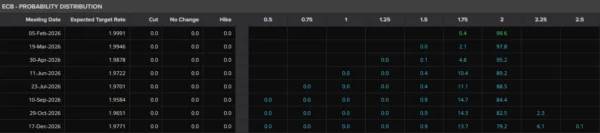

The European Central Bank (ECB) is widely expected to hold key interest rates steady.

As the European Central Bank (ECB) prepares for its first major meeting of 2026 on February 5, the Governing Council finds itself in a delicate balancing act. After a series of rate cuts in late 2024 and 2025 that brought the deposit facility rate down to 2.00%, the central bank now faces a "neutral" landscape where the next move is far from certain.

Market consensus is overwhelmingly in favor of a hold. The ECB is expected to maintain its key interest rates, the Deposit Facility at 2.00%, the Main Refinancing Operations at 2.15%, and the Marginal Lending Facility at 2.40%.

This "wait-and-see" approach is bolstered by January's inflation data, which landed right on the ECB's 2% target. While some economists suggest that headline inflation could actually dip as low as 1.7% in the coming weeks, the Governing Council appears content to let the current restrictive-to-neutral policy simmer. Following the "plateau" narrative that emerged in late 2025, the February meeting is less about the immediate decision and more about the "policy signals" for the rest of the year.

The euro enters February 2026 in a position of renewed strength but this has introduced a new layer of complexity to the ECB's deliberations. In early 2026, the euro broke above the 1.19 mark against the US dollar, briefly testing the psychological resistance level of 1.20.

However, this Euro strength is a double-edged sword for Frankfurt.

The Deflationary Hedge: A stronger euro helps suppress imported inflation—particularly energy and raw materials priced in dollars. This gives President Christine Lagarde more breathing room to keep rates steady even if global commodity prices fluctuate.

The Growth Drag: The "global euro moment" also brings risks. A potent currency threatens the competitiveness of Eurozone exports, particularly for the German industrial sector, which is already struggling with a modest 2026 growth forecast of 0.8% to 1.2%. If the euro's appreciation becomes too aggressive, it could "import deflation" to the point of undershooting the 2% target, potentially forcing the ECB to resume rate cuts earlier than the "hold through 2026" crowd expects.

Market participants are looking past the February announcement to the ECB's Survey of Professional Forecasters (SPF) and the subsequent March projections. Currently, swap markets are pricing in very little movement for the remainder of 2026, signaling that the "rate cut cycle" that defined 2025 has likely reached its conclusion.

However, the tone of the press conference will be vital. Any emphasis on "downside risks to growth" or concerns regarding the "undershooting of inflation" will be interpreted as a dovish tilt. Conversely, if Lagarde maintains that service-sector inflation remains sticky, the Euro could see further gains as traders price out any remaining hopes for a mid-year cut.

President Lagarde's press conference will be closely watched for clues on balancing inflation, growth, and market risks.

For the Euro, the February meeting is likely to consolidate its recent gains unless the ECB explicitly expresses discomfort with the currency's level. With the US Federal Reserve also reaching a potential pause in its own cycle, the EUR/USD pair is finding a new equilibrium.

The primary takeaway for February 2026 is that the ECB has successfully navigated the "soft landing." The focus has shifted from "how high" or "how low" to "how long", how long will rates stay at 2% before the next economic shift dictates a new direction.

For now, stability is the name of the game in Frankfurt.

From a technical standpoint, EUR/USD has seen a significant pullback since the January 27 high at 1.2082.

The pullback is just over 50% of the initial upside move which started at the 1.1572 handle on January 19.

Heading into the meeting, EUR/USD rests at a key area of support which was the swing high in December 2025 around the 1.1794.

If this level holds, then a run back toward the psychological 1.2000 handle may be on the cards.

The period 14-RSI bodes well, having bounced off the neutral 50 level which hints at bullish momentum remaining in play.

A break lower from here may bring the 100-day MA back into focus around the 1.1678 handle.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up