Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Regional bank Westamerica Bancorporation reported revenue ahead of Wall Streets expectations in Q4 CY2025, but sales fell by 9.1% year on year to $63.55 million. Its non-GAAP profit of $1.12 per share was 5.2% above analysts’ consensus estimates.

Westamerica Bancorporation (WABC) Q4 CY2025 Highlights:

"Westamerica’s fourth quarter 2025 results benefited from the Company’s valuable low-cost deposit base, of which 46 percent was represented by non-interest bearing checking accounts during the quarter; the annualized cost of funding our loan and bond portfolios was 0.24 percent in the quarter. Operating expenses remained well controlled at 40 percent of total revenues. At December 31, 2025, nonperforming assets were stable at $1.8 million and the allowance for credit losses was $11.6 million” said Chairman, President and CEO David Payne.

Company Overview

Founded in 1884 and serving communities from Mendocino County in the north to Kern County in the south, Westamerica Bancorporation provides banking services to individuals and small businesses throughout Northern and Central California.

Sales Growth

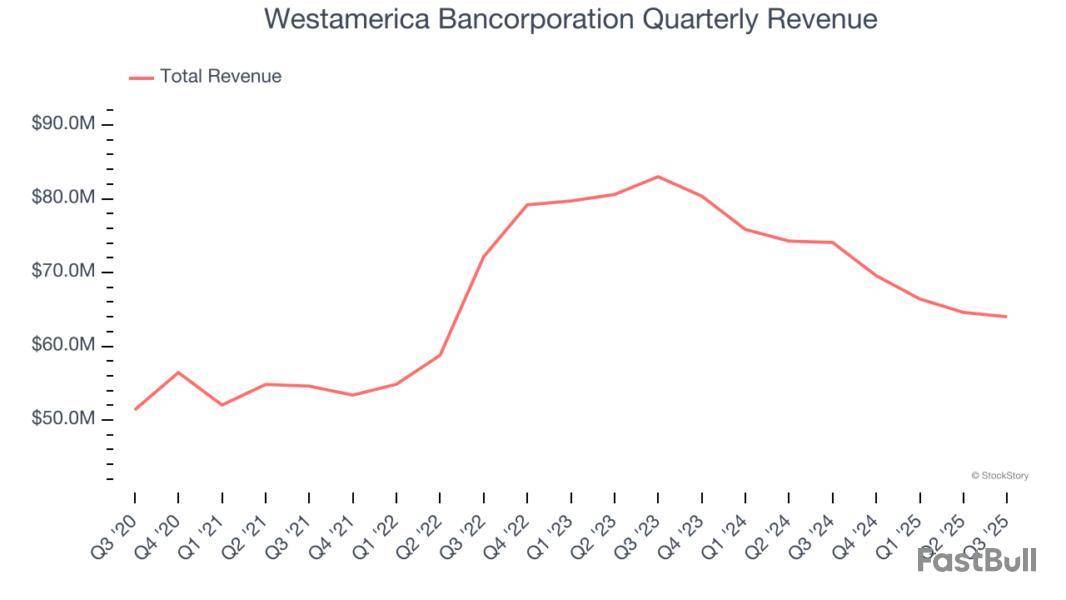

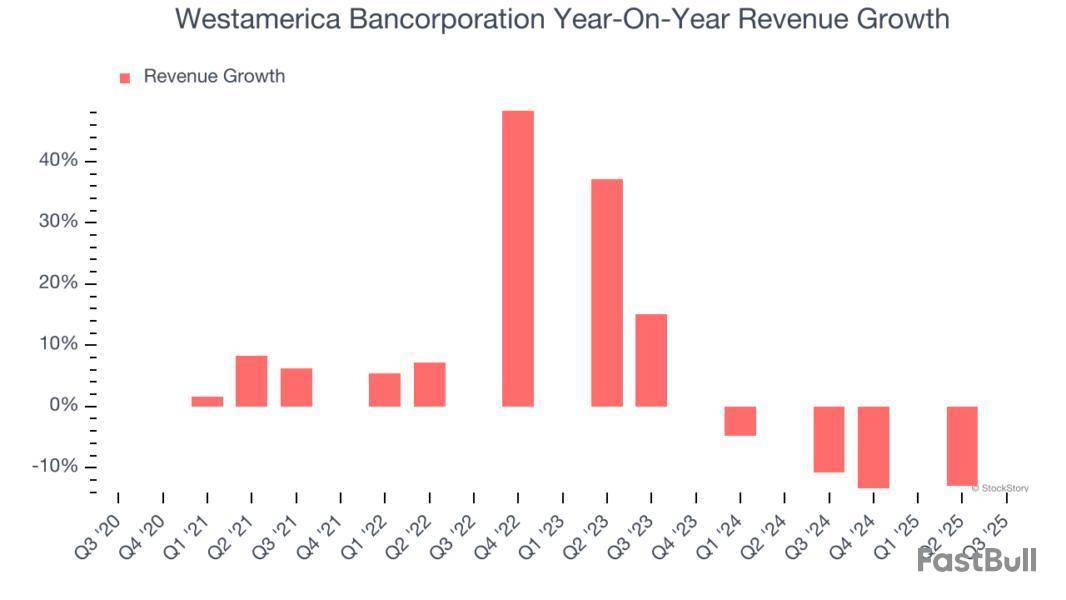

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Regrettably, Westamerica Bancorporation’s revenue grew at a sluggish 4% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Westamerica Bancorporation’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 10.7% annually.

This quarter, Westamerica Bancorporation’s revenue fell by 9.1% year on year to $63.55 million but beat Wall Street’s estimates by 2.7%.

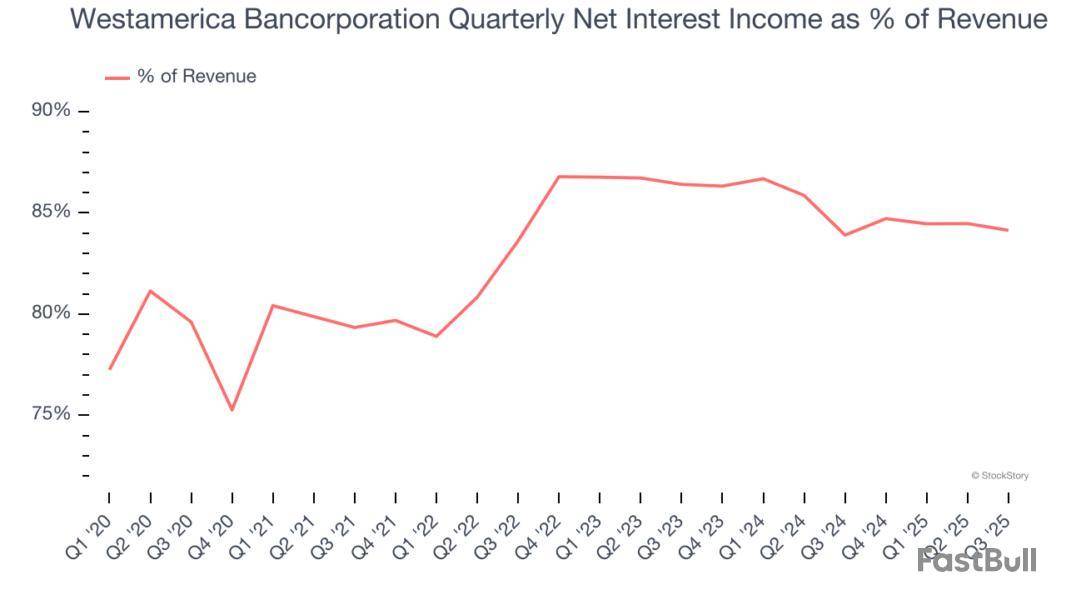

Net interest income made up 83.2% of the company’s total revenue during the last five years, meaning Westamerica Bancorporation barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Key Takeaways from Westamerica Bancorporation’s Q4 Results

We enjoyed seeing Westamerica Bancorporation beat analysts’ net interest income expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $50.92 immediately after reporting.

So do we think Westamerica Bancorporation is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up