Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

The US dollar rose against its major trading partners early Tuesday, ahead of a light data release day.

Earlier Tuesday, the National Federation for Independent Business reported that small business sentiment improved modestly but that uncertainty remains. Taxes were cited as the largest problem by 18% of respondents, above labor quality and inflation for the first time since December 2020.

Weekly Redbook same-store sales are due to be released at 8:55 am ET.

Federal Reserve officials are in their 'quiet period' ahead of the next Federal Open Market Committee meeting on June 17-18.

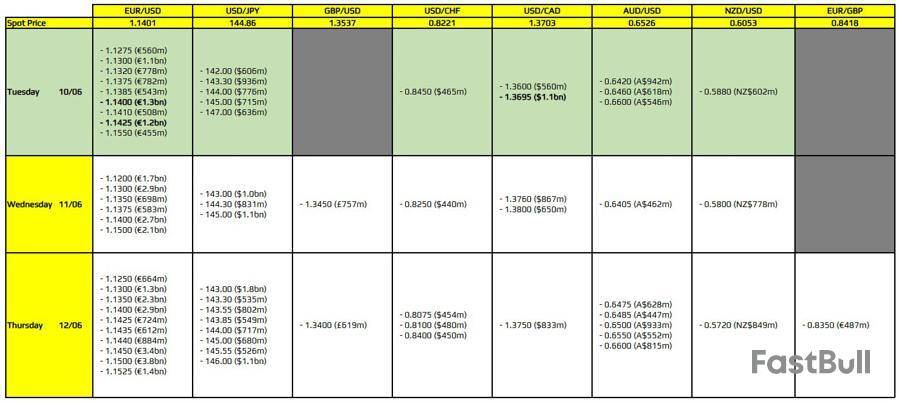

A quick summary of foreign exchange activity heading into Tuesday:

fell to 1.1424 from 1.1425 at the Monday US close but was above a level of 1.1420 at the same time Monday morning. Eurozone investor confidence rose in June to indicate slightly more optimism than pessimism, according to data released earlier Tuesday. European Central Bank President Christine Lagarde is due to speak at 11:15 pm ET. The next European Central Bank meeting is scheduled for July 24.

fell to 1.3501 from 1.3559 at the Monday US close and 1.3560 at the same time Monday morning. UK employment and earnings growth slowed in April while the unemployment rate increased, according to data released overnight. The next Bank of England meeting is scheduled for June 19.

rose to 144.5864 from 144.5770 at the Monday US close and 144.1785 at the same time Monday morning. Japanese machine tool orders growth slowed in May while money stock growth accelerated according to data release overnight. The next Bank of Japan meeting is scheduled for June 16-17.

rose to 1.3698 from 1.3685 at the Monday US close and 1.3675 at the same time Monday morning. There are no Canadian data on Tuesday's schedule. The next Bank of Canada meeting is scheduled for July 30.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up