Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

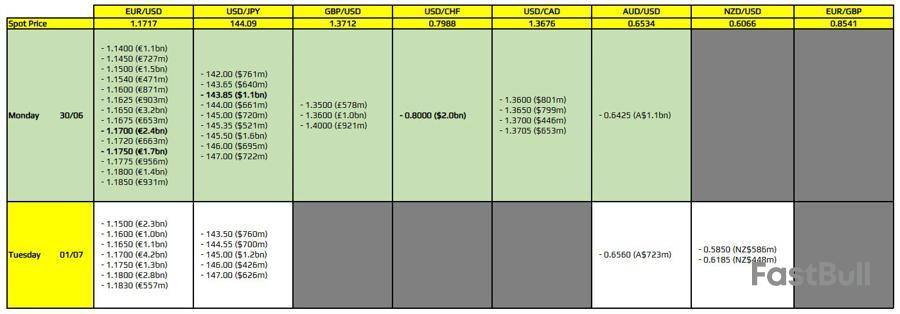

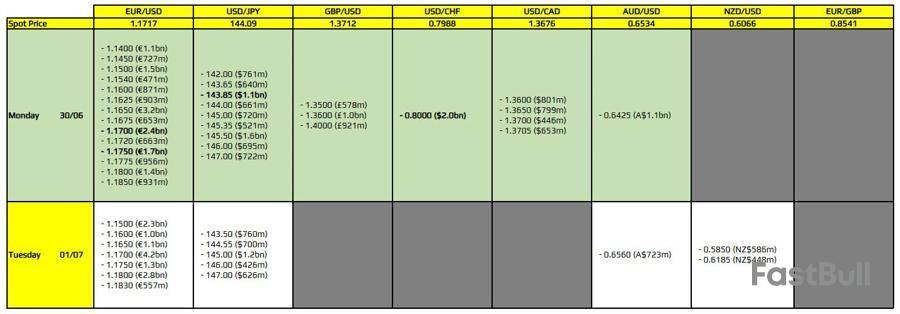

There are a couple to take note of on the day, as highlighted in bold.

The first ones being for EUR/USD at the 1.1700 and 1.1750 levels. The expiry levels don't tie in to any technical significance but they could very well play a role in terms of limiting price action as we look towards the month-end fix later in the day. Keep in mind that there are also large expiries sitting at the same levels tomorrow as well.

Then, there is one for USD/JPY at the 143.85 level. That doesn't really tie to anything either but sits near last week's low at least. That could limit downside but I wouldn't look to the expiries here to have too much impact. Dollar sentiment will remain the bigger driver, especially with month-end in consideration too.

And lastly, there is one for USD/CHF at the 0.8000 level. That is one that could act as a bit of a hold for price action but with the pair dribbling lower last week, the downside momentum remains more favourable. So, that will act as a counterweight to the expiries though we do have month-end to contend with as noted above.

In summary, the expiries could play a minor role in European morning trade but as month-end approaches, dollar sentiment and related flows will take on more importance on a day like this.

For more information on how to use this data, you may refer to this post here. This article was written by Justin Low at www.forexlive.com.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up