Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q2. Today, we are looking at it distribution & solutions stocks, starting with ePlus .

IT Distribution & Solutions will be buoyed by the increasing complexity of IT ecosystems, rising cloud adoption, and demand for cybersecurity solutions. Enterprises are less likely than ever to embark on these complicated journeys solo, and companies in the sector boast expertise and scale in these areas. However, cloud migration also means less need for hardware, which could dent demand for large portions of the product portfolio and hurt margins. Additionally, planning for potentially supply chain disruptions is ongoing, as the COVID-19 pandemic showed how damaging a pause in global trade could be in areas like semiconductor procurement.

The 7 it distribution & solutions stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 6.2% while next quarter’s revenue guidance was 0.5% below.

In light of this news, share prices of the companies have held steady as they are up 4.5% on average since the latest earnings results.

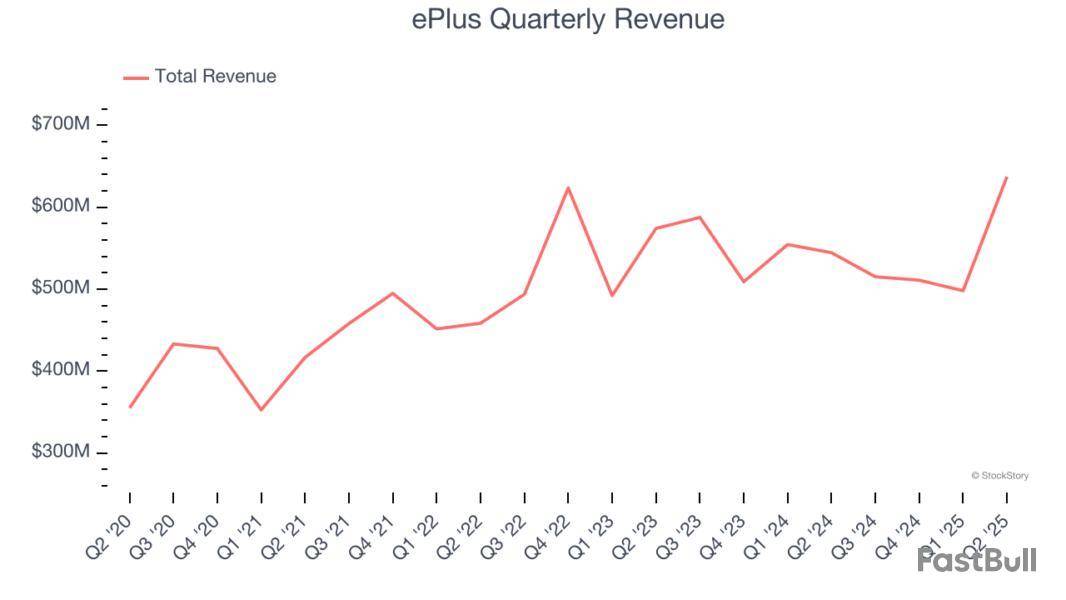

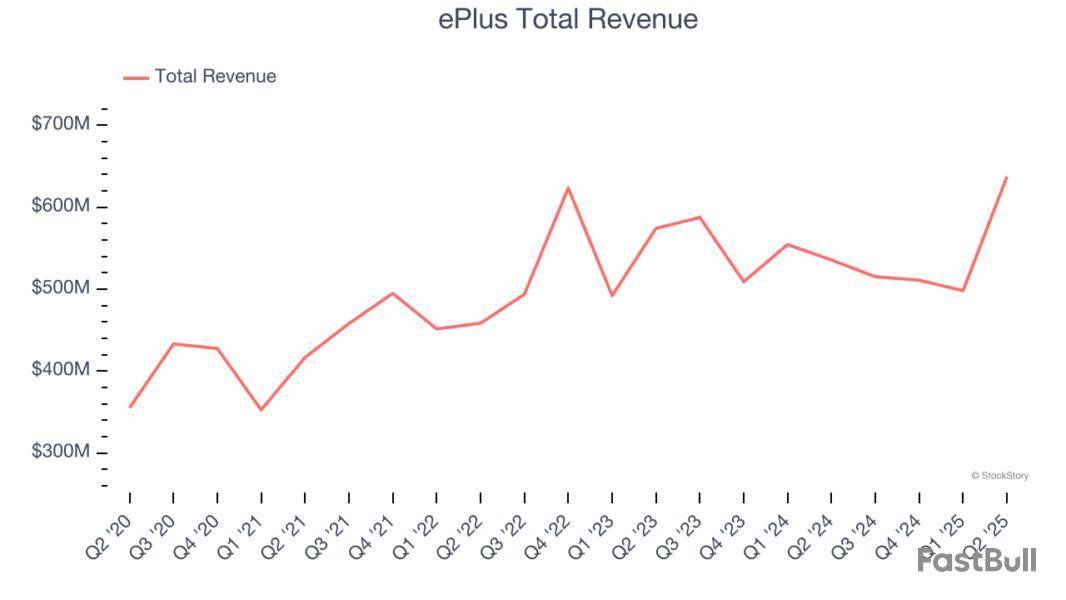

Starting as a financing company in 1990 before evolving into a full-service technology provider, ePlus provides comprehensive IT solutions, professional services, and financing options to help organizations optimize their technology infrastructure and supply chain processes.

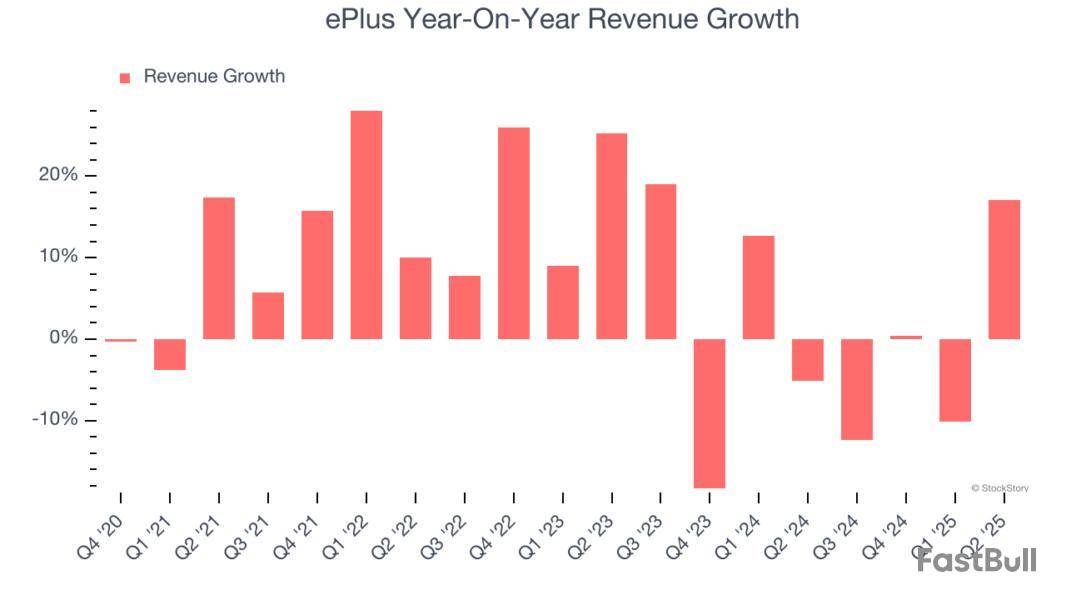

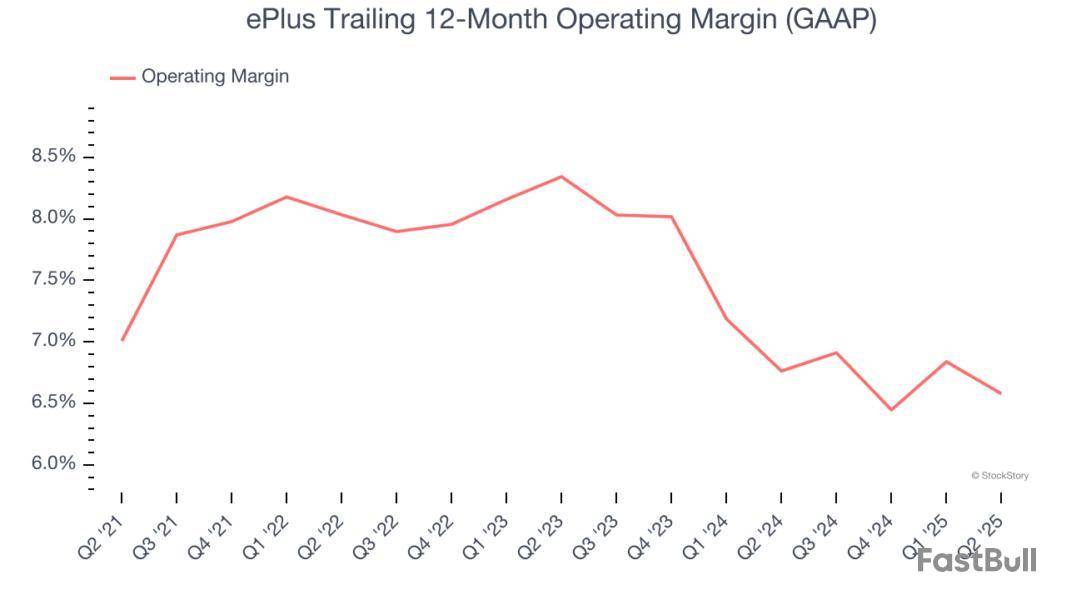

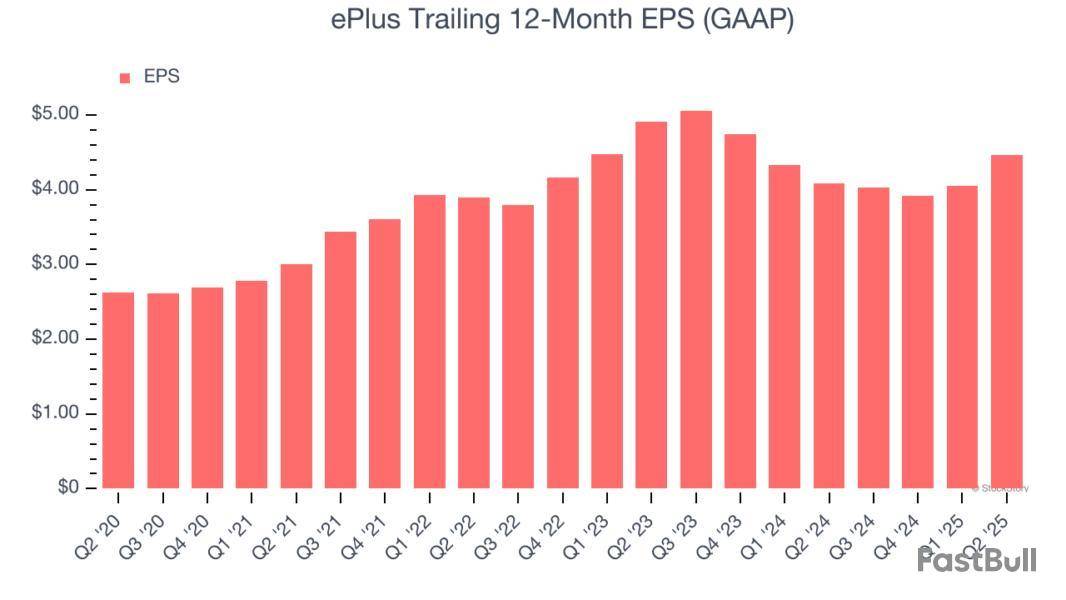

ePlus reported revenues of $637.3 million, up 19% year on year. This print exceeded analysts’ expectations by 23.3%. Overall, it was an incredible quarter for the company with a beat of analysts’ EPS estimates.

"Fiscal 2026 is off to a strong start both financially and strategically. We reported double digit growth across key financial metrics, including revenue, gross profit, and earnings per share. Our services business continues to be a standout, increasing nearly 50% in the quarter," commented Mark Marron, president and CEO of ePlus.

ePlus achieved the biggest analyst estimates beat and fastest revenue growth of the whole group. Unsurprisingly, the stock is up 16.1% since reporting and currently trades at $73.68.

Is now the time to buy ePlus? Access our full analysis of the earnings results here, it’s free.

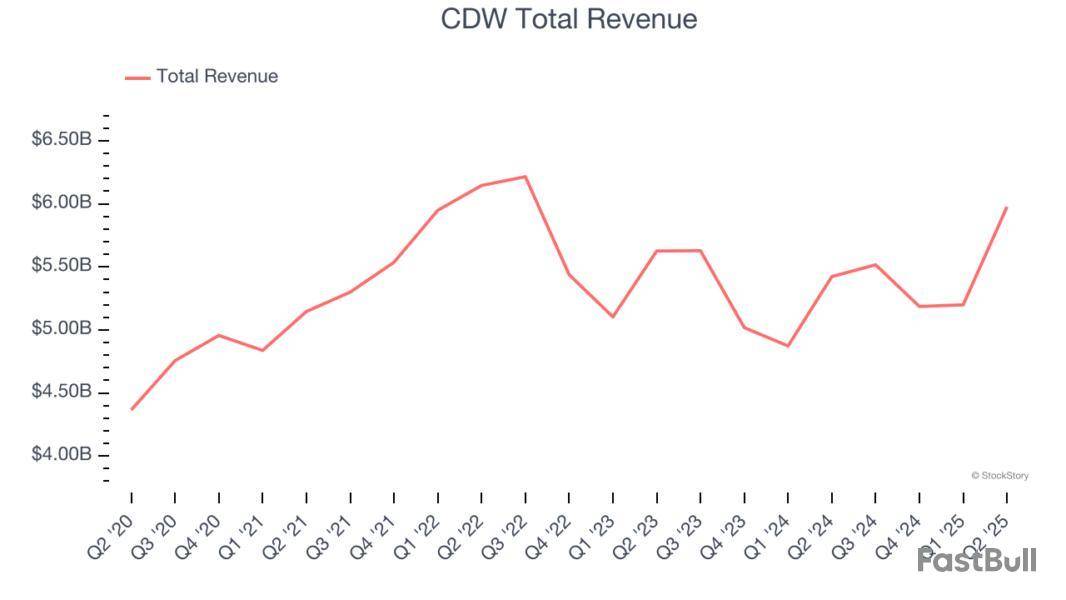

Serving as a crucial bridge between technology manufacturers and end users since 1984, CDW is a multi-brand provider of information technology solutions that helps businesses and public sector organizations select, implement, and manage hardware, software, and IT services.

CDW reported revenues of $5.98 billion, up 10.2% year on year, outperforming analysts’ expectations by 7.8%. The business had a very strong quarter with a beat of analysts’ EPS estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $164.45.

Is now the time to buy CDW? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Insight Enterprises

With over 35 years of IT expertise and partnerships with more than 8,000 technology providers, Insight Enterprises provides end-to-end digital transformation solutions that help businesses modernize their IT infrastructure and maximize the value of technology.

Insight Enterprises reported revenues of $2.09 billion, down 3.2% year on year, falling short of analysts’ expectations by 2.4%. It was a slower quarter as it posted a miss of analysts’ EPS estimates.

Insight Enterprises delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 8.4% since the results and currently trades at $132.64.

Read our full analysis of Insight Enterprises’s results here.

Operating as the crucial link in the global technology supply chain with a presence in 57 countries, Ingram Micro is a global technology distributor that connects manufacturers with resellers, providing hardware, software, cloud services, and logistics expertise.

Ingram Micro reported revenues of $12.79 billion, up 10.9% year on year. This result beat analysts’ expectations by 6.4%. Taking a step back, it was a slower quarter as it recorded a significant miss of analysts’ EPS estimates and revenue guidance for next quarter slightly missing analysts’ expectations.

The stock is up 3.5% since reporting and currently trades at $19.49.

Read our full, actionable report on Ingram Micro here, it’s free.

With a century-long history of adapting to technological evolution, Avnet is a global electronic components distributor that connects manufacturers of semiconductors and other electronic parts with businesses that need these components.

Avnet reported revenues of $5.62 billion, flat year on year. This print topped analysts’ expectations by 4.5%. More broadly, it was a satisfactory quarter as it also logged a beat of analysts’ EPS estimates but a significant miss of analysts’ EPS guidance for next quarter estimates.

The stock is up 4.3% since reporting and currently trades at $54.11.

Read our full, actionable report on Avnet here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up